WHO PAYS THE PRICE? OVERDRAFT FEE CEILINGS AND THE UNBANKED

30 Slides618.78 KB

WHO PAYS THE PRICE? OVERDRAFT FEE CEILINGS AND THE UNBANKED Jennifer Dlugosz, Federal Reserve Board Brian Melzer, Dartmouth Donald Morgan, Federal Reserve Bank of New York CFPB Research Conference May 7, 2021 Disclaimer: The views expressed in this presentation are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of New York or the Federal Reserve System

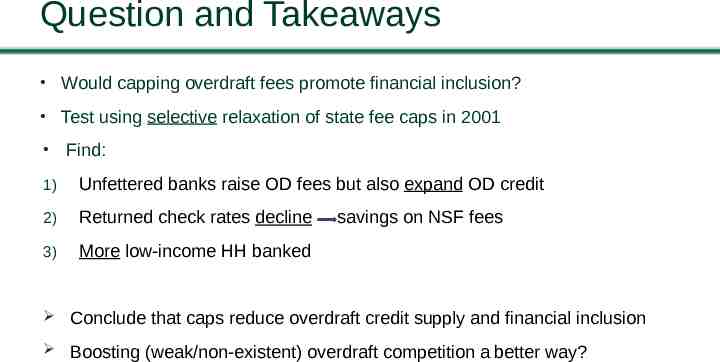

Question and Takeaways Would capping overdraft fees promote financial inclusion? Test using selective relaxation of state fee caps in 2001 Find: 1) Unfettered banks raise OD fees but also expand OD credit 2) Returned check rates decline 3) More low-income HH banked savings on NSF fees Conclude that caps reduce overdraft credit supply and financial inclusion Boosting (weak/non-existent) overdraft competition a better way?

Plan 1. Background 2. Study Design/Findings 3. Conclusion

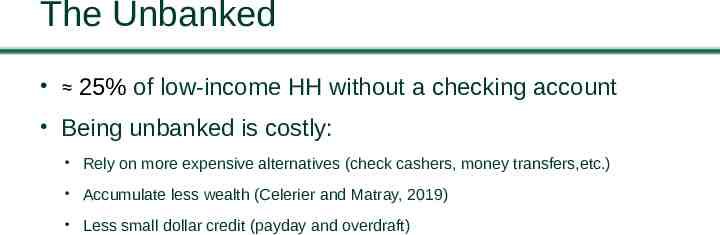

The Unbanked 25% of low-income HH without a checking account Being unbanked is costly: Rely on more expensive alternatives (check cashers, money transfers,etc.) Accumulate less wealth (Celerier and Matray, 2019) Less small dollar credit (payday and overdraft)

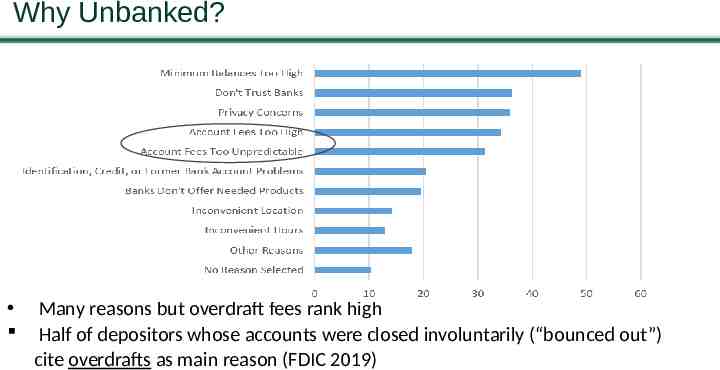

Why Unbanked? % FDIC (2019) Many reasons but overdraft fees rank high Half of depositors whose accounts were closed involuntarily (“bounced out”) cite overdrafts as main reason (FDIC 2019)

Background: Overdraft Credit Demand Demand essentially bi-modal - Most depositors rarely/never overdraw; small proportion overdraw almost monthly (CFPB 2013) Depositors must opt-in for overdraft coverage via debit and ATM - Opt-in higher (45%) for heavy uses of OD (CFPB 2013) Depositors that don’t repay credit/fees “bounce out” - Bank closes account and reports to debit bureaus (e.g. Chex systems) - 6.5M accounts closed in 2005 (Campbell et al 2012)

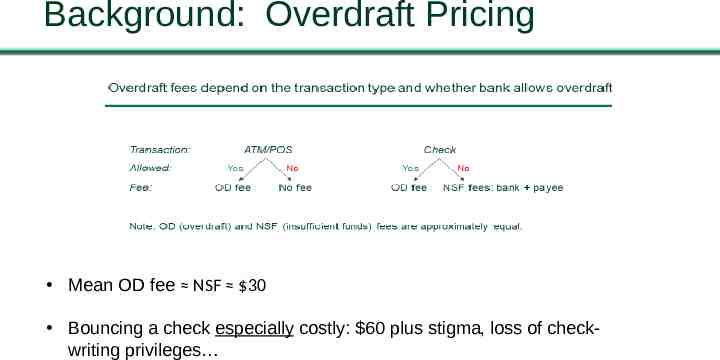

Background: Overdraft Pricing Mean OD fee NSF 30 Bouncing a check especially costly: 60 plus stigma, loss of checkwriting privileges

Question: Would Fees Caps Promote Inclusion? Many consumer advocacy groups (Pew, CRL) recommend caps Federal cap proposed in 2019 (“Stop Overdraft Profiteering Act”) “overdraft fees push low-income consumers away from banking products altogether” (Sen. Cory A. Booker, 2018) Price theory predicts unintended effects: - Overdraft credit is credit per fee - Fee cap credit rationing

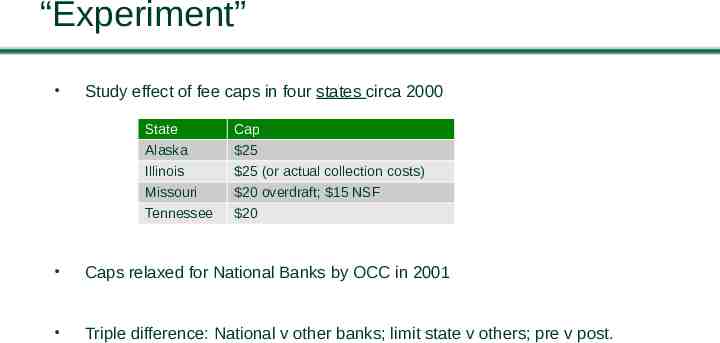

“Experiment” Study effect of fee caps in four states circa 2000 State Cap Alaska 25 Illinois 25 (or actual collection costs) Missouri 20 overdraft; 15 NSF Tennessee 20 Caps relaxed for National Banks by OCC in 2001 Triple difference: National v other banks; limit state v others; pre v post.

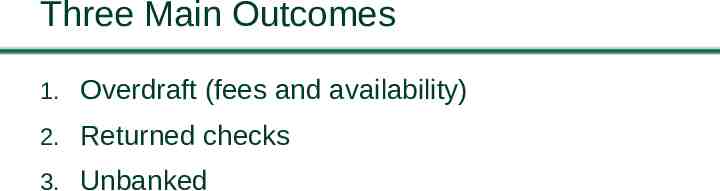

Three Main Outcomes 1. Overdraft (fees and availability) 2. Returned checks 3. Unbanked

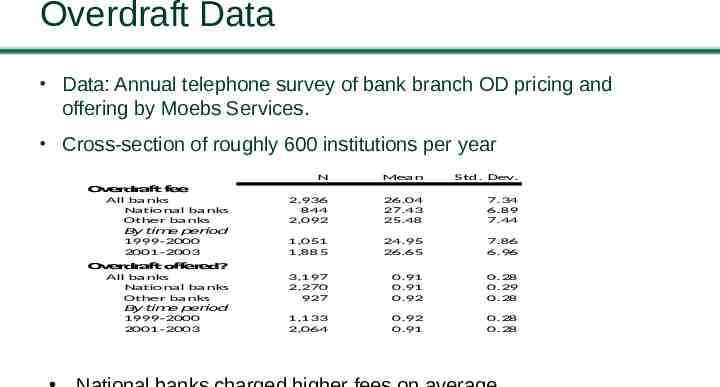

Overdraft Data Data: Annual telephone survey of bank branch OD pricing and offering by Moebs Services. Cross-section of roughly 600 institutions per year Overdraft fee All banks National banks Other banks By time period 1999-2000 2001-2003 Overdraft offered? All banks National banks Other banks By time period 1999-2000 2001-2003 N Mean Std. Dev. 2,936 844 2,092 26.04 27.43 25.48 7.34 6.89 7.44 1,051 1,885 24.95 26.65 7.86 6.96 3,197 2,270 927 0.91 0.91 0.92 0.28 0.29 0.28 1,133 2,064 0.92 0.91 0.28 0.28

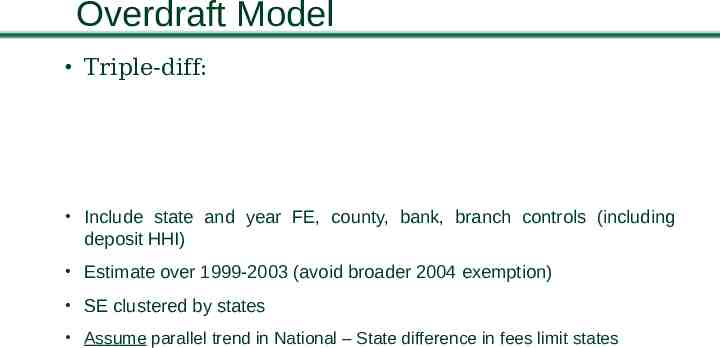

Overdraft Model Triple-diff: Include state and year FE, county, bank, branch controls (including deposit HHI) Estimate over 1999-2003 (avoid broader 2004 exemption) SE clustered by states Assume parallel trend in National – State difference in fees limit states

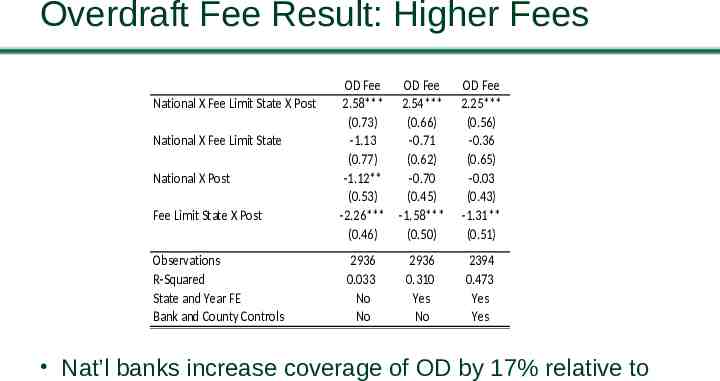

Overdraft Fee Result: Higher Fees National X Fee Limit State X Post National X Fee Limit State National X Post Fee Limit State X Post Observations R-Squared State and Year FE Bank and County Controls OD Fee 2.58*** (0.73) -1.13 (0.77) -1.12** (0.53) -2.26*** (0.46) OD Fee 2.54*** (0.66) -0.71 (0.62) -0.70 (0.45) -1.58*** (0.50) OD Fee 2.25*** (0.56) -0.36 (0.65) -0.03 (0.43) -1.31** (0.51) 2936 0.033 No No 2936 0.310 Yes No 2394 0.473 Yes Yes Nat’l banks increase coverage of OD by 17% relative to

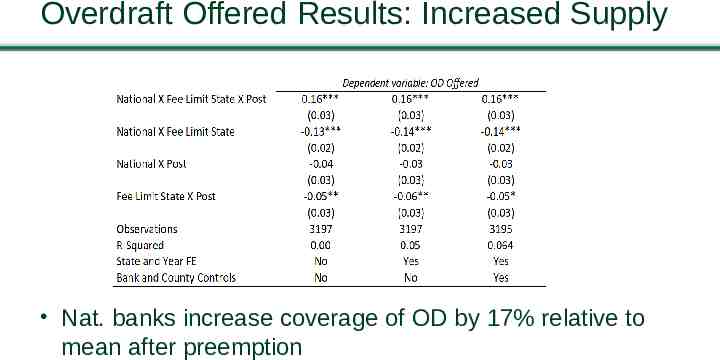

Overdraft Offered Results: Increased Supply Nat. banks increase coverage of OD by 17% relative to mean after preemption

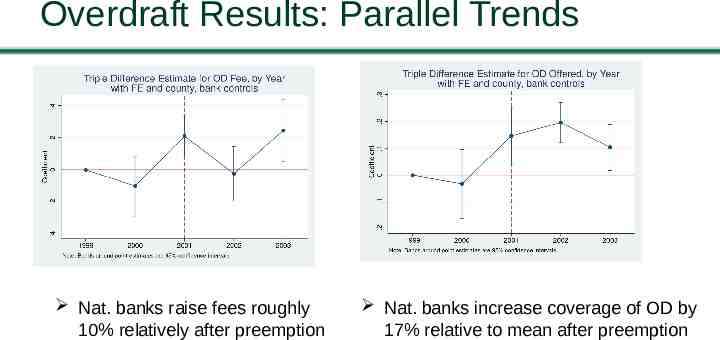

Overdraft Results: Parallel Trends Nat. banks raise fees roughly 10% relatively after preemption Nat. banks increase coverage of OD by 17% relative to mean after preemption

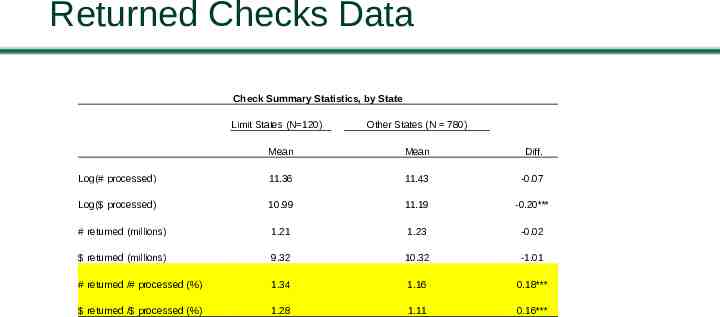

Returned Checks Data Data from Fed check processing centers (CPC): Checks processed and returned (“bounced”) per quarter Estimate diff-in-diff at CPC level. 46 CPC one per state; 6 in limit states

Returned Checks Data Check Summary Statistics, by State Limit States (N 120) Other States (N 780) Mean Mean Diff. Log(# processed) 11.36 11.43 -0.07 Log( processed) 10.99 11.19 -0.20*** # returned (millions) 1.21 1.23 -0.02 returned (millions) 9.32 10.32 -1.01 # returned /# processed (%) 1.34 1.16 0.18*** returned / processed (%) 1.28 1.11 0.16***

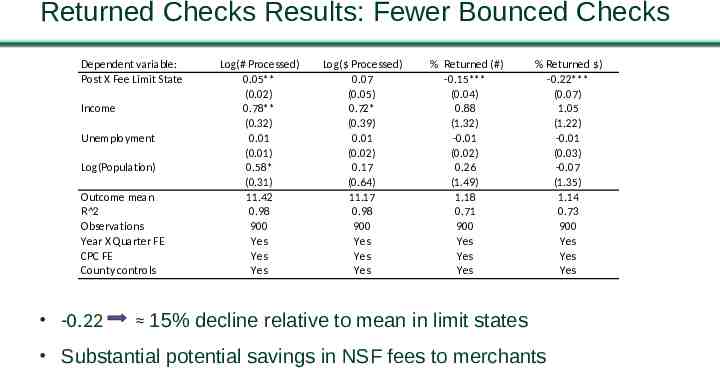

Returned Checks Results: Fewer Bounced Checks Dependent variable: Post X Fee Limit State Income Unemployment Log(Population) Outcome mean R 2 Observations Year X Quarter FE CPC FE County controls -0.22 Log(# Processed) 0.05** (0.02) 0.78** (0.32) 0.01 (0.01) 0.58* (0.31) 11.42 0.98 900 Yes Yes Yes Log( Processed) 0.07 (0.05) 0.72* (0.39) 0.01 (0.02) 0.17 (0.64) 11.17 0.98 900 Yes Yes Yes % Returned (#) -0.15*** (0.04) 0.88 (1.32) -0.01 (0.02) 0.26 (1.49) 1.18 0.71 900 Yes Yes Yes % Returned ) -0.22*** (0.07) 1.05 (1.22) -0.01 (0.03) -0.07 (1.35) 1.14 0.73 900 Yes Yes Yes 15% decline relative to mean in limit states Substantial potential savings in NSF fees to merchants

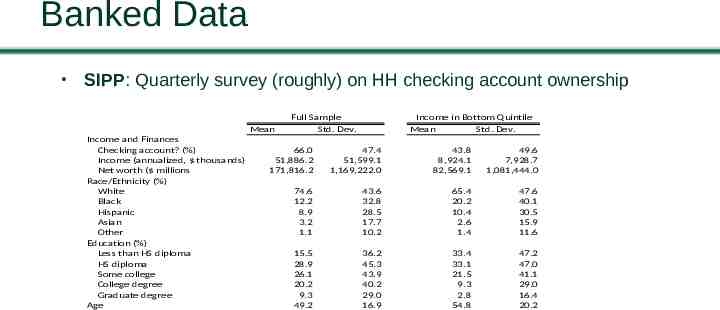

Banked Data SIPP: Quarterly survey (roughly) on HH checking account ownership Mean Income and Finances Checking account? (%) Income (annualized, thousands) Net worth ( millions Race/Ethnicity (%) White Black Hispanic Asian Other Education (%) Less than HS diploma HS diploma Some college College degree Graduate degree Age Full Sample Std. Dev. Income in Bottom Quintile Mean Std. Dev. 66.0 51,886.2 171,816.2 47.4 51,599.1 1,169,222.0 43.8 8,924.1 82,569.1 49.6 7,928.7 1,081,444.0 74.6 12.2 8.9 3.2 1.1 43.6 32.8 28.5 17.7 10.2 65.4 20.2 10.4 2.6 1.4 47.6 40.1 30.5 15.9 11.6 15.5 28.9 26.1 20.2 9.3 49.2 36.2 45.3 43.9 40.2 29.0 16.9 33.4 33.1 21.5 9.3 2.8 54.8 47.2 47.0 41.1 29.0 16.4 20.2

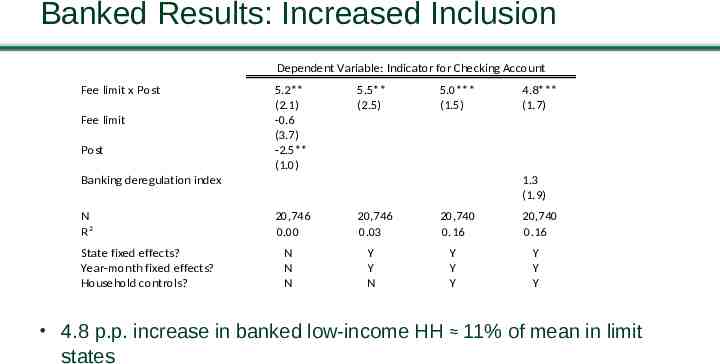

Banked Results: Increased Inclusion Dependent Variable: Indicator for Checking Account Fee limit x Post Fee limit Post 5.2** (2.1) -0.6 (3.7) -2.5** (1.0) 5.5** (2.5) 5.0*** (1.5) Banking deregulation index N R2 State fixed effects? Year-month fixed effects? Household controls? 4.8*** (1.7) 1.3 (1.9) 20,746 0.00 N N N 20,746 0.03 Y Y N 20,740 0.16 Y Y Y 20,740 0.16 Y Y Y 4.8 p.p. increase in banked low-income HH 11% of mean in limit states

Banked: Behavioral Concerns Newly banked not necessarily better off if fees “shrouded” (Gabaix and Laibson 2006) “Naïve” depositors open/re-open account but later have it closed after a rash of overdrafts/returned checks Lower returned check rates suggest otherwise Also find lower account turnover and enduring relationships

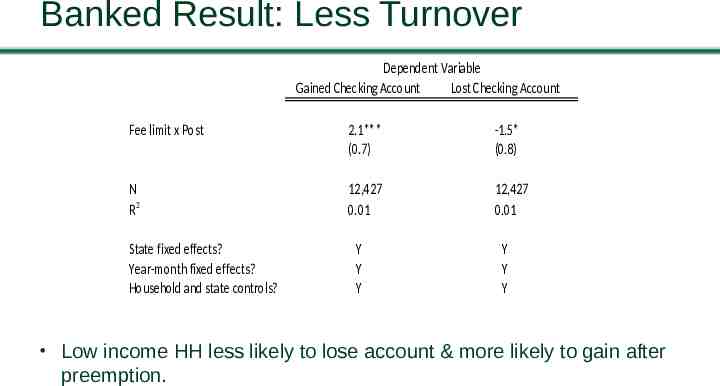

Banked Result: Less Turnover Dependent Variable Gained Checking Account Lost Checking Account Fee limit x Post 2.1*** (0.7) -1.5* (0.8) N R2 12,427 0.01 12,427 0.01 State fixed effects? Year-month fixed effects? Household and state controls? Y Y Y Y Y Y Low income HH less likely to lose account & more likely to gain after preemption.

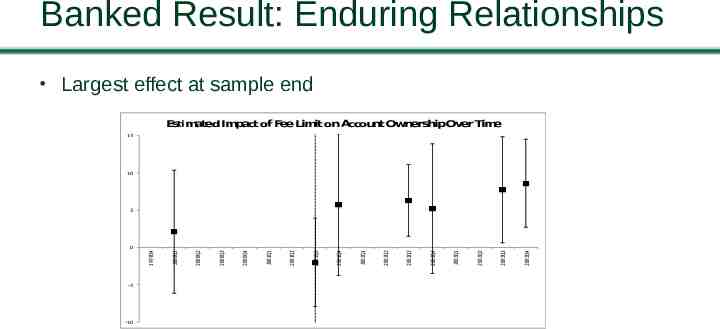

Banked Result: Enduring Relationships Largest effect at sample end Es matedImpact of FeeLimit onAccount OwnershipOver Time 15 10 -5 -10 2003Q4 2003Q3 2003Q2 2003Q1 2002Q4 2002Q3 2002Q2 2002Q1 2001Q4 2001Q3 2001Q2 2001Q1 2000Q4 2000Q3 2000Q2 1999Q4 0 2000Q1 5

Recap 1) Fee caps lower OD fees but less OD credit 2) Higher returned checks rates under caps credit (and in NSF) 3) Low income HH less likely banked with cap less OD

Conclusion Urge to curb high overdraft fees understandable but beware Ec:101: caps reduce overdraft credit, so more bounces checks and less financial exclusion Banked depositors pay in returned check fees that might have been covered absent cap Increasing competition may be better path to increased inclusion

Competition Instead of Caps? Overdraft very profitable to banks and credit unions ( 35 bn annually) Competition weak among depositories (no advertising!) But works across small dollar lenders (Melzer and Morgan 2004)

Reference Slides

Contribution Financial Inclusion. Campbell, Martinez-Jerez, Tufano (2012), Celerier and Matray (2019), Dupas, Karlan, Robinson, Ubfal (2018), Bord (2020). Behavioral economics/consumer financial regulation. Gabaix and Laibson (2006), Mullainathan, Barr, and Shafir (2009), Heidhues and Koszegi (2018), Alan, Cemalcilar, Karlan, Zinman (2018), Stango and Zinman (2011, 2014), Ru and Schoar (2019), Melzer and Morgan (2005) Price ceilings in banking. Agarwal, Chomsisengphet, Mahoney, Stroebel (2014), Nelson (2018), Kay, Manuszak, Vojtech (2017)); Knittel and Stango (2003), DeYoung and Phillips (2009), Melzer and Schroeder (2018).

OCC preemption OCC historically preempts state fee and usury limits for National banks Before 2001, OCC had granted only qualified exemption from state overdraft fee limits; evaluated case-by-case OCC removed qualification in July 2001 and categorically exempted national banks from state limits Natural experiment: only national banks exempted, only some states limited

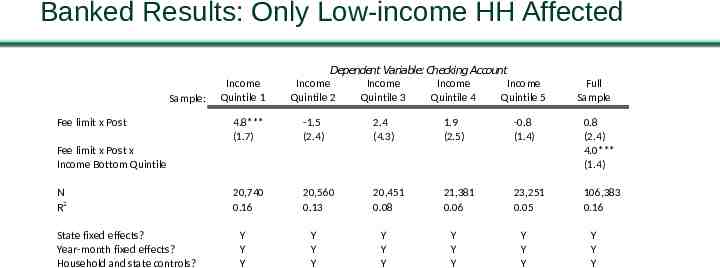

Banked Results: Only Low-income HH Affected Sample: Fee limit x Post Income Quintile 1 Dependent Variable: Checking Account Income Income Income Income Quintile 2 Quintile 3 Quintile 4 Quintile 5 4.8*** (1.7) -1.5 (2.4) 2.4 (4.3) 1.9 (2.5) -0.8 (1.4) 0.8 (2.4) 4.0*** (1.4) 20,740 0.16 20,560 0.13 20,451 0.08 21,381 0.06 23,251 0.05 106,383 0.16 Fee limit x Post x Income Bottom Quintile N R2 State fixed effects? Year-month fixed effects? Household and state controls? Full Sample Y Y Y Y Y Y Y Y Y Y Y Y Y Y Y Y Y Y