What To Expect When Applying For a SBA Loan- Tips To Know Before You

31 Slides7.15 MB

What To Expect When Applying For a SBA Loan- Tips To Know Before You Apply. Presented by: Iman Cotton Loan Officer CDC Small Business Finance/Momentus Capital

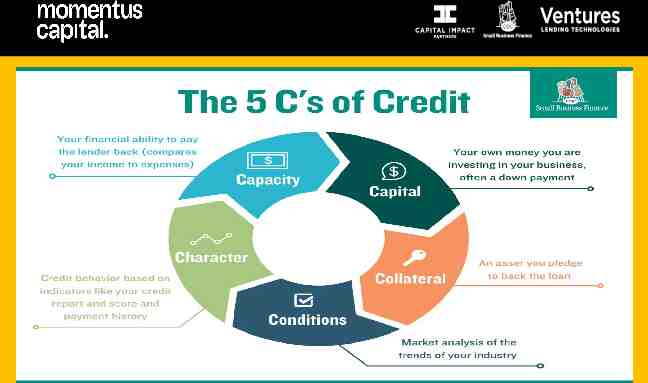

Today’s Topics I. Introduction II. Types of Loans III. The 5 C’s of Credit IV. CDC Loan Products V. Success Stories

Today’s Topics Introduction Types of Loans The 5 C’s of Credit Success Stories 3

What is a CDC? CDC Certified Development Company CDCs are certified by the SBA (Small Business Administration) to administer SBA 504 loans. CDCs are private, non-profit entities with a mission to provide business financing to those who aren’t quite strong enough for bank financing. 260 CDC’s in the country 4

What is a CDFI? CDFI Community Development Financial Institution CDFIs help promote access to capital and local economic growth in urban and rural low-income communities across the nation through monetary awards and the allocation of tax credits. Financial institutions certified by the CDFI Fund are eligible to apply for monetary support and training to build organization capacity. CDFIs are specialized financial institutions that provide financial products and services to populations and businesses located in underserved markets. These institutions have community development missions and a reputation for lending responsibly in low-income communities. CDFIs include banks and bank holding companies, as well as credit unions, loan funds, and venture capital funds. More than 1300 CDFIs 5

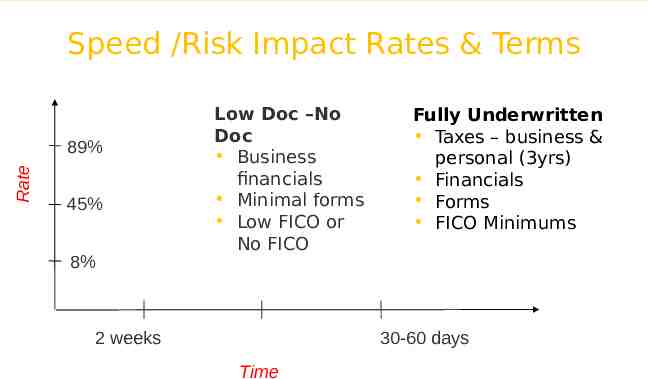

Speed /Risk Impact Rates & Terms Rate 89% 45% 8% Low Doc –No Doc Business financials Minimal forms Low FICO or No FICO 2 weeks Fully Underwritten Taxes – business & personal (3yrs) Financials Forms FICO Minimums 30-60 days Time 6

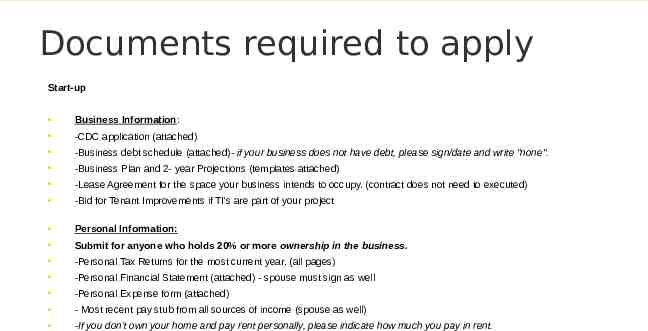

Documents required to apply Start-up Business Information: -CDC application (attached) -Business debt schedule (attached)- if your business does not have debt, please sign/date and write "none". -Business Plan and 2- year Projections (templates attached) -Lease Agreement for the space your business intends to occupy. (contract does not need to executed) -Bid for Tenant Improvements if TI's are part of your project Personal Information: Submit for anyone who holds 20% or more ownership in the business. -Personal Tax Returns for the most current year. (all pages) -Personal Financial Statement (attached) - spouse must sign as well -Personal Expense form (attached) - Most recent pay stub from all sources of income (spouse as well) -If you don’t own your home and pay rent personally, please indicate how much you pay in rent. 7

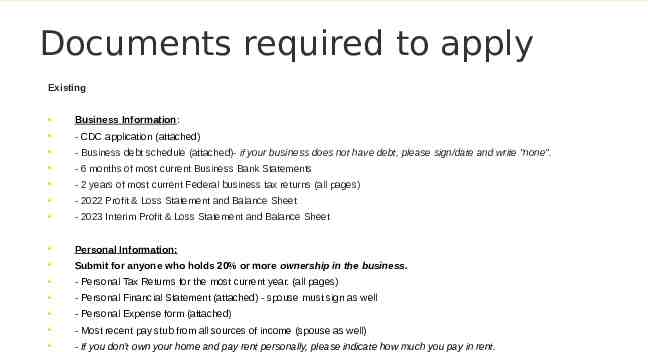

Documents required to apply Existing Business Information: - CDC application (attached) - Business debt schedule (attached)- if your business does not have debt, please sign/date and write "none". - 6 months of most current Business Bank Statements - 2 years of most current Federal business tax returns (all pages) - 2022 Profit & Loss Statement and Balance Sheet - 2023 Interim Profit & Loss Statement and Balance Sheet Personal Information: Submit for anyone who holds 20% or more ownership in the business. - Personal Tax Returns for the most current year. (all pages) - Personal Financial Statement (attached) - spouse must sign as well - Personal Expense form (attached) - Most recent pay stub from all sources of income (spouse as well) - If you don’t own your home and pay rent personally, please indicate how much you pay in rent. 8

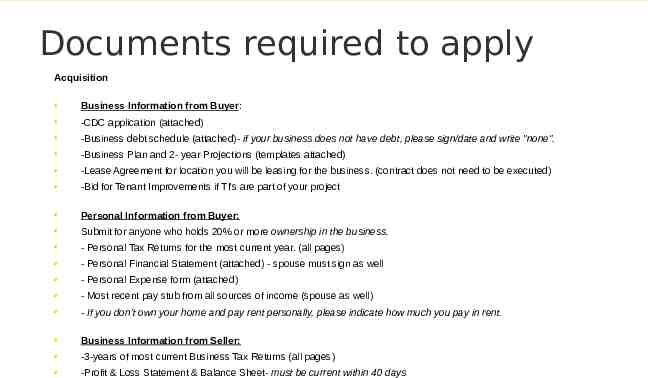

Documents required to apply Acquisition Business Information from Buyer: -CDC application (attached) -Business debt schedule (attached)- if your business does not have debt, please sign/date and write "none". -Business Plan and 2- year Projections (templates attached) -Lease Agreement for location you will be leasing for the business. (contract does not need to be executed) -Bid for Tenant Improvements if TI's are part of your project Personal Information from Buyer: Submit for anyone who holds 20% or more ownership in the business. - Personal Tax Returns for the most current year. (all pages) - Personal Financial Statement (attached) - spouse must sign as well - Personal Expense form (attached) - Most recent pay stub from all sources of income (spouse as well) - If you don’t own your home and pay rent personally, please indicate how much you pay in rent. Business Information from Seller: -3-years of most current Business Tax Returns (all pages) -Profit & Loss Statement & Balance Sheet- must be current within 40 days 9

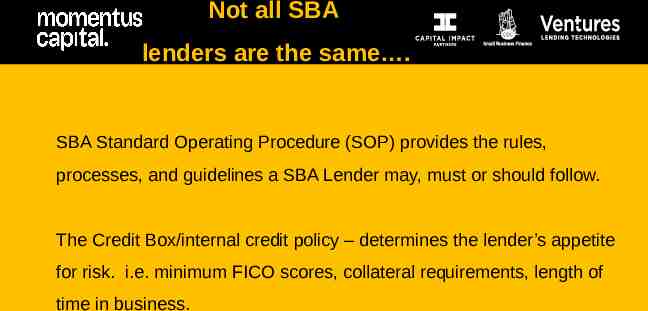

Not all SBA lenders are the same . SBA Standard Operating Procedure (SOP) provides the rules, processes, and guidelines a SBA Lender may, must or should follow. The Credit Box/internal credit policy – determines the lender’s appetite for risk. i.e. minimum FICO scores, collateral requirements, length of time in business.

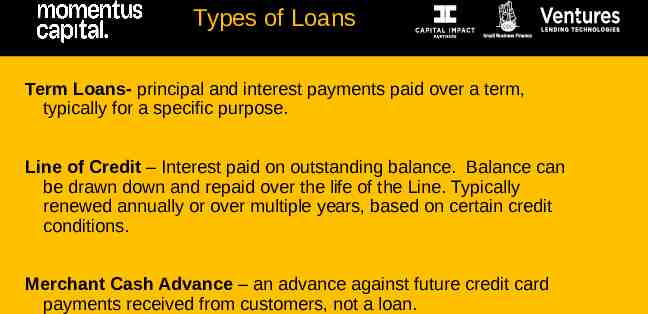

Types of Loans Term Loans- principal and interest payments paid over a term, typically for a specific purpose. Line of Credit – Interest paid on outstanding balance. Balance can be drawn down and repaid over the life of the Line. Typically renewed annually or over multiple years, based on certain credit conditions. Merchant Cash Advance – an advance against future credit card payments received from customers, not a loan.

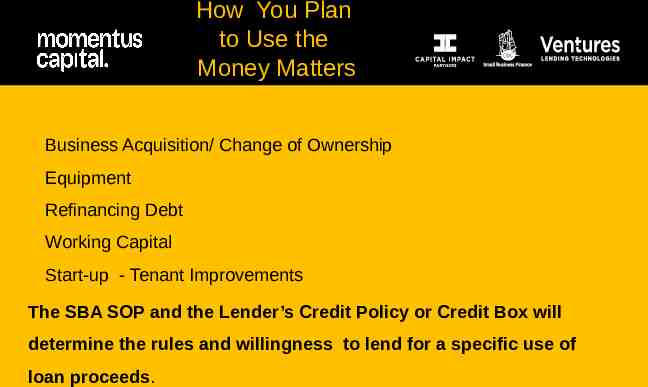

How You Plan to Use the Money Matters Business Acquisition/ Change of Ownership Equipment Refinancing Debt Working Capital Start-up - Tenant Improvements The SBA SOP and the Lender’s Credit Policy or Credit Box will determine the rules and willingness to lend for a specific use of loan proceeds.

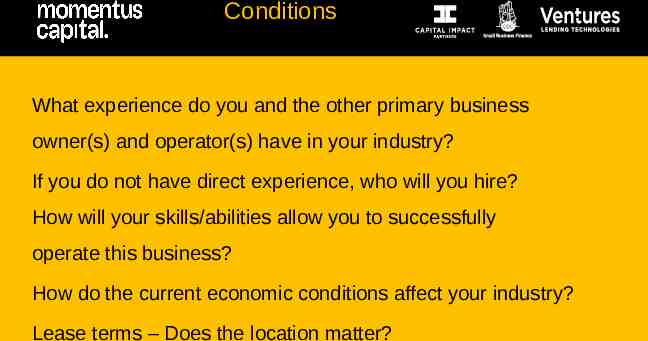

Conditions What experience do you and the other primary business owner(s) and operator(s) have in your industry? If you do not have direct experience, who will you hire? How will your skills/abilities allow you to successfully operate this business? How do the current economic conditions affect your industry? Lease terms – Does the location matter?

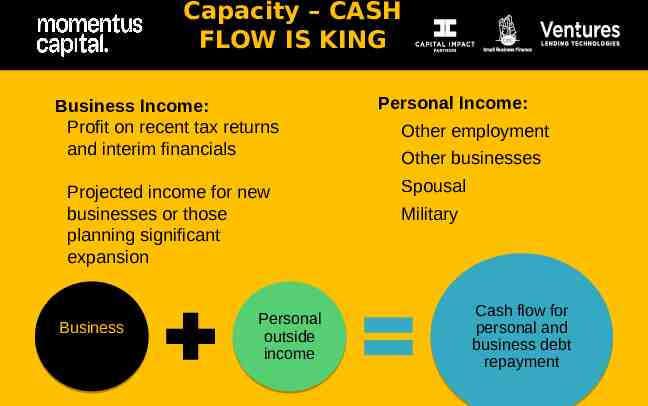

Capacity – CASH FLOW IS KING Business Income: Profit on recent tax returns and interim financials Projected income for new businesses or those planning significant expansion Business profits Personal outside income Personal Income: Other employment Other businesses Spousal Military Cash flow for personal and business debt repayment

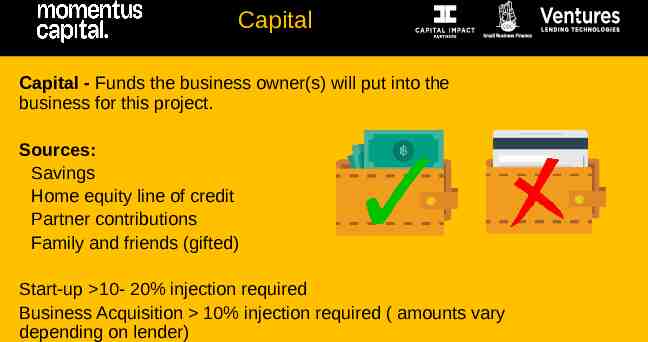

Capital Capital - Funds the business owner(s) will put into the business for this project. Sources: Savings Home equity line of credit Partner contributions Family and friends (gifted) Start-up 10- 20% injection required Business Acquisition 10% injection required ( amounts vary depending on lender)

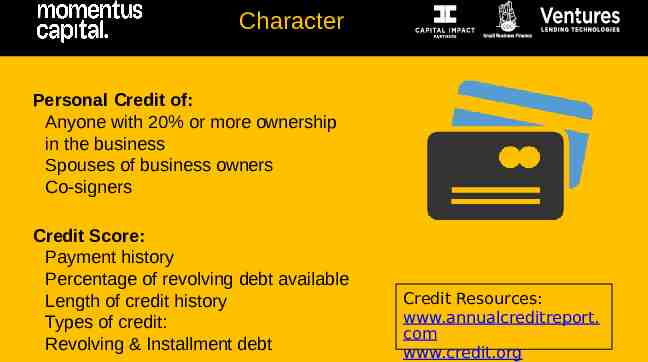

Character Personal Credit of: Anyone with 20% or more ownership in the business Spouses of business owners Co-signers Credit Score: Payment history Percentage of revolving debt available Length of credit history Types of credit: Revolving & Installment debt Credit Resources: www.annualcreditreport. com www.credit.org

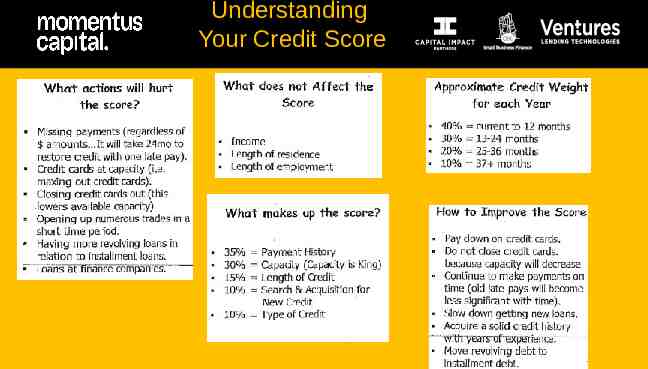

Understanding Your Credit Score

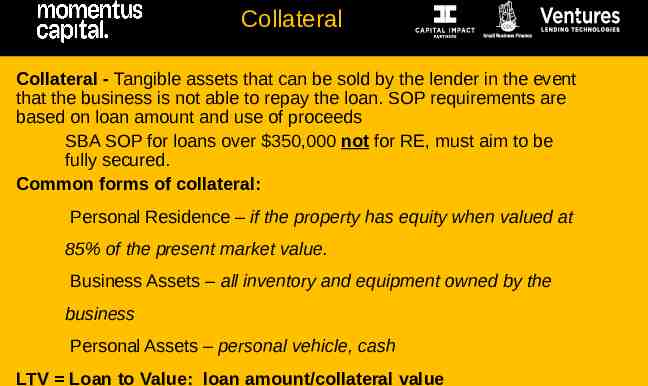

Collateral Collateral - Tangible assets that can be sold by the lender in the event that the business is not able to repay the loan. SOP requirements are based on loan amount and use of proceeds SBA SOP for loans over 350,000 not for RE, must aim to be fully secured. Common forms of collateral: Personal Residence – if the property has equity when valued at 85% of the present market value. Business Assets – all inventory and equipment owned by the business Personal Assets – personal vehicle, cash LTV Loan to Value: loan amount/collateral value

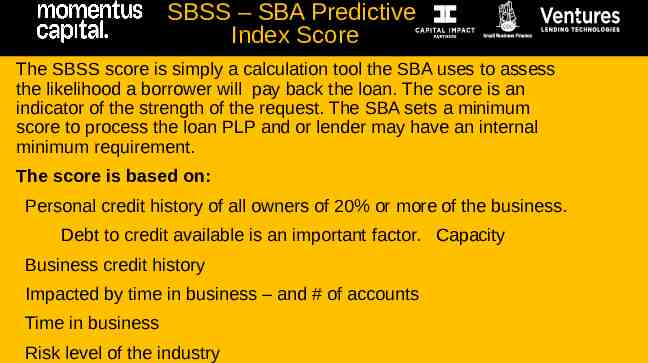

SBSS – SBA Predictive Index Score The SBSS score is simply a calculation tool the SBA uses to assess the likelihood a borrower will pay back the loan. The score is an indicator of the strength of the request. The SBA sets a minimum score to process the loan PLP and or lender may have an internal minimum requirement. The score is based on: Personal credit history of all owners of 20% or more of the business. Debt to credit available is an important factor. Capacity Business credit history Impacted by time in business – and # of accounts Time in business Risk level of the industry

SBA 504- 90 % Fixed rate With an SBA 504 loan, money can be used to buy a building, finance ground-up construction or building improvements, purchase heavy machinery and equipment, or refinance debt 125,000- 20 Million Fixed 10 yrs – equipment 20-25 yrs real estate Down Payment – Minimum 10%

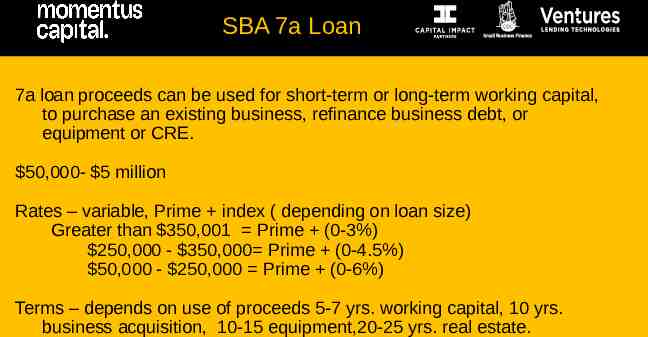

SBA 7a Loan 7a loan proceeds can be used for short-term or long-term working capital, to purchase an existing business, refinance business debt, or equipment or CRE. 50,000- 5 million Rates – variable, Prime index ( depending on loan size) Greater than 350,001 Prime (0-3%) 250,000 - 350,000 Prime (0-4.5%) 50,000 - 250,000 Prime (0-6%) Terms – depends on use of proceeds 5-7 yrs. working capital, 10 yrs. business acquisition, 10-15 equipment,20-25 yrs. real estate.

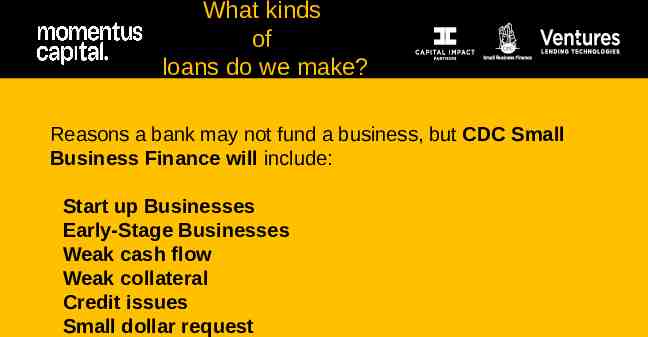

What kinds of loans do we make? Reasons a bank may not fund a business, but CDC Small Business Finance will include: Start up Businesses Early-Stage Businesses Weak cash flow Weak collateral Credit issues Small dollar request

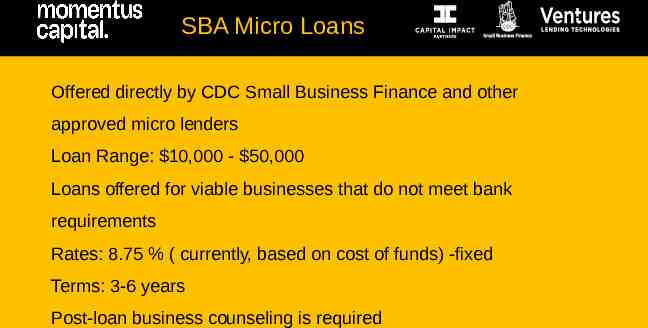

SBA Micro Loans Offered directly by CDC Small Business Finance and other approved micro lenders Loan Range: 10,000 - 50,000 Loans offered for viable businesses that do not meet bank requirements Rates: 8.75 % ( currently, based on cost of funds) -fixed Terms: 3-6 years Post-loan business counseling is required

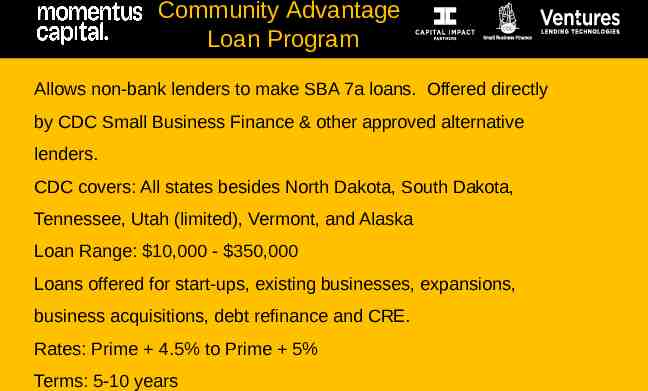

Community Advantage Loan Program Allows non-bank lenders to make SBA 7a loans. Offered directly by CDC Small Business Finance & other approved alternative lenders. CDC covers: All states besides North Dakota, South Dakota, Tennessee, Utah (limited), Vermont, and Alaska Loan Range: 10,000 - 350,000 Loans offered for start-ups, existing businesses, expansions, business acquisitions, debt refinance and CRE. Rates: Prime 4.5% to Prime 5% Terms: 5-10 years

Impact Loans Focused on serving African-American and Latino small business owners and businesses located in low- and moderate-income areas. ONLY California – State Guaranteed Loan Loan Range: 10,000 - 350,000 Loans offered for start-ups, existing businesses, expansions, business acquisitions, debt refinance and CRE. Rates: Prime 4.5% to Prime 5% Terms: 10-year amortization due in 5 years

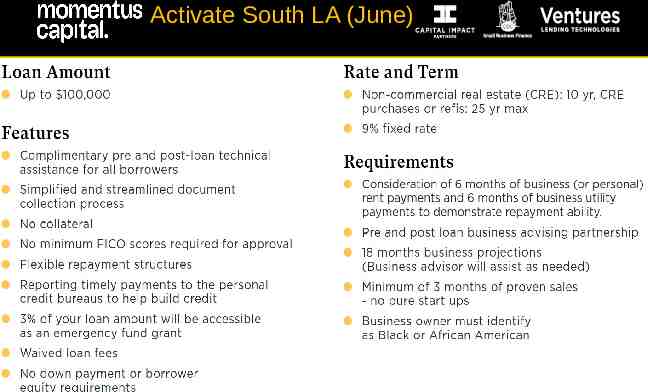

Activate South LA (June)

Success Stories

Start-up Project: Needed funds to create additional products, secure an employee, and pay off debt. Referral Source: LinkedIn Credit: Low 600 Collateral/ Guarantors: UCC 1 on business assets Cash Flow: (projections-based request plus one year of bus tax returns) Capital - 36,500 (gifted) – Plus has current w2 job. UOP –working capital, equipment, debt consolidation

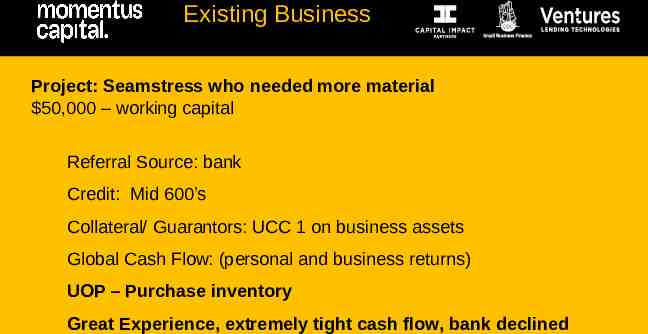

Existing Business Project: Seamstress who needed more material 50,000 – working capital Referral Source: bank Credit: Mid 600’s Collateral/ Guarantors: UCC 1 on business assets Global Cash Flow: (personal and business returns) UOP – Purchase inventory Great Experience, extremely tight cash flow, bank declined

THANK YOU.