Tim Stepp, Internal Audit INSPIRE | EQUIP | CONNECT |

16 Slides2.74 MB

Tim Stepp, Internal Audit INSPIRE EQUIP CONNECT

Agenda Review of Financial Guide Fraud Update What questions/concerns do you have?

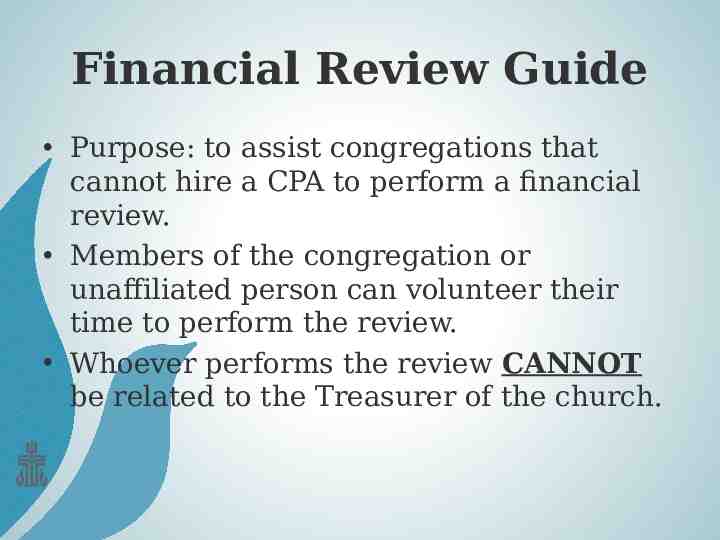

Financial Review Guide Purpose: to assist congregations that cannot hire a CPA to perform a financial review. Members of the congregation or unaffiliated person can volunteer their time to perform the review. Whoever performs the review CANNOT be related to the Treasurer of the church.

Bank/Investment Accounts After the books are closed: Bank Reconciliations are performed. Request from each bank/investment account the account balance, and the authorized signers on the account. Verify Safety Deposit Box access

Income Offering counted by two unrelated persons. Review deposit slips for timeliness and compare to secretary/treasurer records. Test a sample of counter’s documentation vs. deposit slips and bank statements for accurate postings of offerings and correct designations. Review the original books of entry for other income and that it is appropriately accounted for. On a test basis conduct donation confirmations.

Disbursements Invoices are properly approved. Verify that the cancelled check matches the invoice information. All checks are accounted for. Accounts that are charged are noted on invoice. Invoices greater than 30 days are accrued for. Per capita/mission apportionments are paid accordingly. Procedures in place to account for restricted gifts.

Reports Approved budget is included. Controls for over budget expenditures are in place. Policy for restricted funds reviewed. Reports are provided in timely fashion. Report distribution is appropriate. Balance Sheet and Statement of Income/Expense prepared.

General Ledger Restricted funds are separated appropriately. Internal controls for receipts and disbursements are reviewed. Verify fund balance from prior year and correct balance is carried forward.

Administrative EIN, tax filings, deed to church property, mortgage, and insurance policies are safeguarded. Adequate insurance coverage. Church has separate bond for people handling money. Where and how documents are safeguarded noted, and who has access.

Payroll/Tax Records Personnel files are kept confidential and secure. Tax forms are issued timely to all personnel. Payroll tax deposits and timely remittances to government occur. Proper 1099 filing and approvals for persons paid over 600 (contracts/honorariums). Test that the appropriate amount of tax is withheld. Vouch payroll and tax records coincide with actual disbursements made.

Organizational Fraud Update

Fraud Statistics 2016 Total Loss - 6.3 Billion (2,410 cases studied in 114 Countries) Median Loss - 150,000 (same for small and large organizations) Average Time to Detect – 18 Months Most Common Method to Detect - Tips (39%)

Top 3 Control Weaknesses that contributed to Fraud 29% - Lack of Internal Controls 20% - Override of Controls by Management 19% - Lack of Management Review

Behavioral Red Flags of Fraud 45% - Living Beyond Means 30% - Financial Difficulties 20% - Close Relationship with Vendors/Customers 15% - Wheeler Dealer Attitude 15% - Family Problems 8% - Refusal to take Vacation

QUESTIONS? Joined by: Denise Hampton, CPA – Presbyterian Mission Agency Toni Carver-Smith – Presbyterian Mission Agency