The Affordable Care Act: Small Business Forum Mitchell Stein Health

30 Slides165.29 KB

The Affordable Care Act: Small Business Forum Mitchell Stein Health Policy Consulting

Part 1

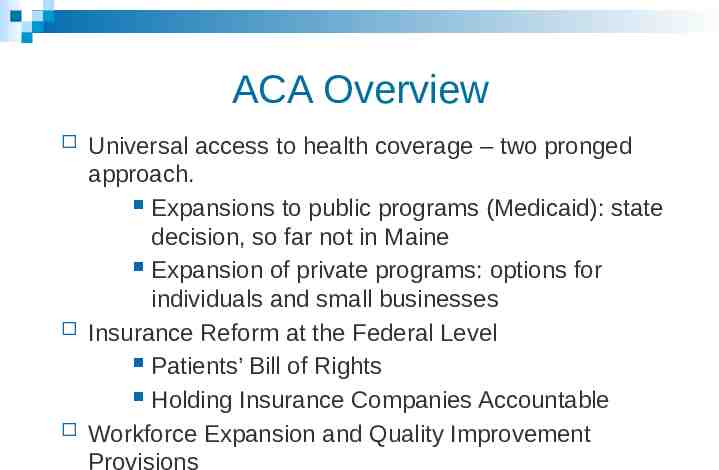

ACA Overview Universal access to health coverage – two pronged approach. Expansions to public programs (Medicaid): state decision, so far not in Maine Expansion of private programs: options for individuals and small businesses Insurance Reform at the Federal Level Patients’ Bill of Rights Holding Insurance Companies Accountable Workforce Expansion and Quality Improvement Provisions

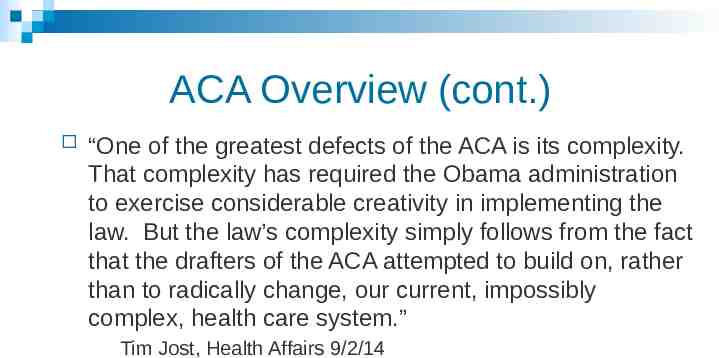

ACA Overview (cont.) “One of the greatest defects of the ACA is its complexity. That complexity has required the Obama administration to exercise considerable creativity in implementing the law. But the law’s complexity simply follows from the fact that the drafters of the ACA attempted to build on, rather than to radically change, our current, impossibly complex, health care system.” Tim Jost, Health Affairs 9/2/14

What’s Happening Now Effective now Minimum Credible Coverage Requirement: Mandate for Individuals to Have Health Coverage Marketplace Coverage and Subsidies Plan reforms including Essential Health Benefits and no cost sharing preventative services Risk Adjustment Programs

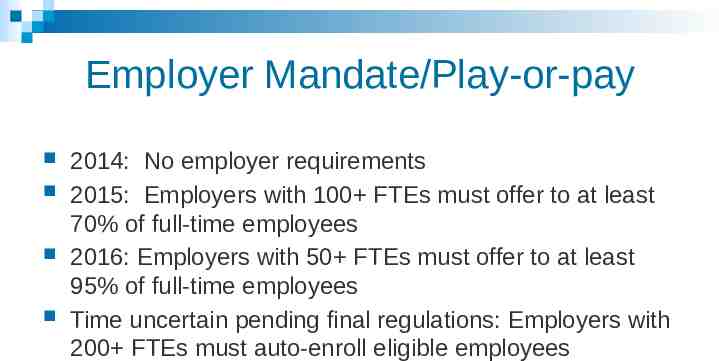

Employer Mandate/Play-or-pay 2014: No employer requirements 2015: Employers with 100 FTEs must offer to at least 70% of full-time employees 2016: Employers with 50 FTEs must offer to at least 95% of full-time employees Time uncertain pending final regulations: Employers with 200 FTEs must auto-enroll eligible employees

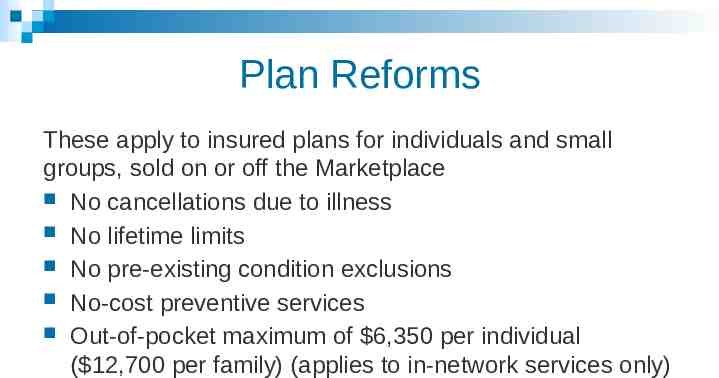

Plan Reforms These apply to insured plans for individuals and small groups, sold on or off the Marketplace No cancellations due to illness No lifetime limits No pre-existing condition exclusions No-cost preventive services Out-of-pocket maximum of 6,350 per individual ( 12,700 per family) (applies to in-network services only)

Marketplaces (Exchanges) An Exchange is a Marketplace that is an easier way to shop for health insurance (now referred to as the Marketplace): www.healthcare.gov Two Marketplaces: Individual and the Small Business Health Options Program (SHOP) The Marketplace provides a way to compare and review choices in a consumer-friendly “apples to apples” format Standardized plan levels Note sole-proprietors use the Individual Marketplace

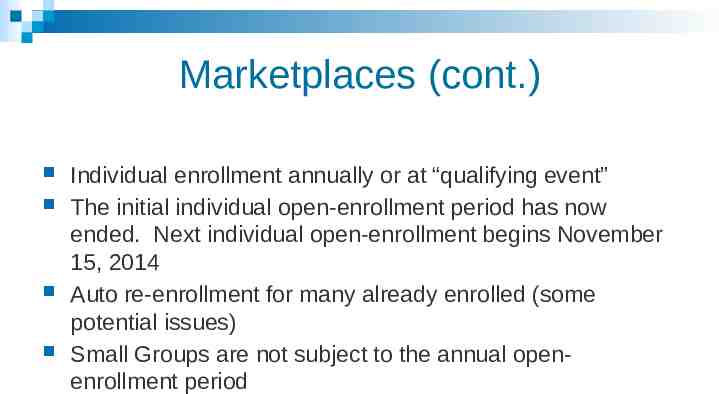

Marketplaces (cont.) Individual enrollment annually or at “qualifying event” The initial individual open-enrollment period has now ended. Next individual open-enrollment begins November 15, 2014 Auto re-enrollment for many already enrolled (some potential issues) Small Groups are not subject to the annual openenrollment period

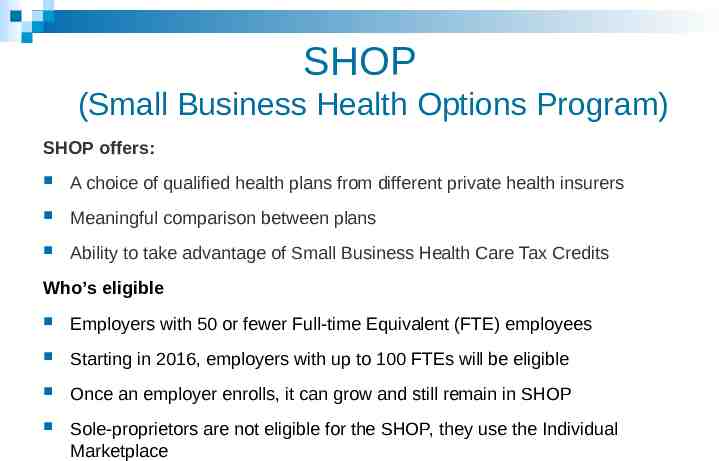

SHOP (Small Business Health Options Program) SHOP offers: A choice of qualified health plans from different private health insurers Meaningful comparison between plans Ability to take advantage of Small Business Health Care Tax Credits Who’s eligible Employers with 50 or fewer Full-time Equivalent (FTE) employees Starting in 2016, employers with up to 100 FTEs will be eligible Once an employer enrolls, it can grow and still remain in SHOP Sole-proprietors are not eligible for the SHOP, they use the Individual Marketplace

SHOP Employers are not subject to open-enrollment period, can start plans at any time Minimum participation requirements are waived annually between 11/15 and 12/15 Employees are subject to an open enrollment period unless they experience a qualifying event

SHOP For 2014 “Direct Enrollment” using broker or insurer For 2015 (planned November 2014 availability) Enroll through broker, insurer or directly on the SHOP For 2016 (due to state decision to delay an additional year) Option to offer employees a choice among qualified health plans across multiple health insurance companies

What Insurers Are Participating in 2015 (Individual and Small Group)? On Marketplace Anthem Health Plans of Maine Harvard Pilgrim Health Care Inc. Maine Community Health Options Multi-state plan (for individuals) An additional plan will be offered by the Blue Cross/Blue Shield (BC/BS) Association, however it will be virtually identical to the Anthem plan (the BC/BS affiliate in Maine) Off Marketplace All marketplace insurers Aetna Health Inc United Healthcare (small group plans only) Note Mega is exiting the market and non-renewing its current customers as their plans expire

What Dental Insurers Are Participating? Individual On Marketplace All medical insurers offering plans with integrated pediatric dental Anthem, Delta and Dentegra offering stand-alone dental Individual Off Marketplace All of the above plus Renaissance Small Group On Marketplace All medical insurers offering plans with integrated pediatric dental Anthem, Delta and Dentegra and Guardian Life offering stand-alone dental Small Group Off Marketplace Many!

Part 2

Employer Specifics Notice of Marketplace Options (samples available on DoL website: http://www.dol.gov/ebsa/healthreform/) For new employees and annually for existing staff Summary of Benefits and Coverage (SBC) For insured plans should be created by insurer and given to the employer to distribute Applies to all individual and group plans (no exception for grandfathered plans) COBRA New model notice now includes notification of marketplace options. Often with available subsidies Marketplace plans are a better option than COBRA

Employer Specifics Additional Items (cont.) New hire waiting period cannot exceed 90 days (all plans, grandfathered or not) W2 disclosure of benefit costs began January 2013 (for 2012 year) If issued less than 250 W2s in January 2012, exempt until final regulations issued Note this is NOT taxable income. For informational purposes only similar to the 401k box on current forms

Employer Specifics Additional Items (cont.) Flexible Spending Account (FSA) limit of 2,500 including Health and Dependent Care FSAs. HRA and HSA not impacted by new limit (begins in 2013) but are impacted by new regulations Medicare Tax Increase for income over 200,000 for individuals and 250,000 for joint filers Patient Centered Outcomes Research Institute Fee (First annual fee payable by July 2013 ) First year, 1 per covered life, second year 2 per covered life, thereafter the 2 is indexed for Medical Inflation

Employer Specifics Additional Items (cont.) Simple Cafeteria Plans (2014 plan year) Congress amended the Internal Revenue Code to allow eligible employers' cafeteria plans to qualify as simple cafeteria plans. Simple cafeteria plans are treated as meeting certain nondiscrimination requirements and benefits for cafeteria plans making the process simpler. Medical Loss Ratio (MLR) Rebates Distribution depends on who pays the premium (employer or employee)

Premium Calculations Before the ACA the common practice was to provide your broker (or insurer) a census of your employees. They would then respond with a single per-employee rate. What you may not have realized is that the rate they quoted was created by calculating a rate for each employee individually and using those to create a single composite rate. In the interest of transparency, the ACA required that the broker and insurer provided individual rates for each employee. While the theory may be sound, in practice this introduced some problems. As a result of the issues experienced by employers, new regulations have now been issued and as of January 1, 2015 composite premiums are once again permitted. Composite Premiums are calculated based on the total group premium (average derived from per-member rating) at the time of enrollment at the beginning of the plan year. The use of Composite Premiums is at each insurer's discretions. While the process is somewhat different than the pre-ACA process, it returns a key benefit for employers. It allows for the single per employee rate to be used during the entire plan year, meaning that if an employee leaves and is replaced with one of a significantly different age, the employer's costs will not be dramatically impacted mid-year. This adds back a level of certainty to the employer's planning process. As of now, no marketplace insurers are planning on offering composite premiums.

Health Insurance Marketplace: Subsidies Who can get an individual subsidy? If NO access to employer coverage: Household income between 100 and 400% FPL (under 100% FPL legally present non-citizens) If YES access to employer coverage: Income between 100 and 400% FPL (under 100% FPL legally present noncitizens) AND Employer plan coverage less than 60% of average expenses or Employer plan for employee costs more than 9.5% of income Sample 2013 FPLs: 100% Single - 11,490, Family of 4 - 23,550 400% Single - 45,960, Family of 4 - 94,200

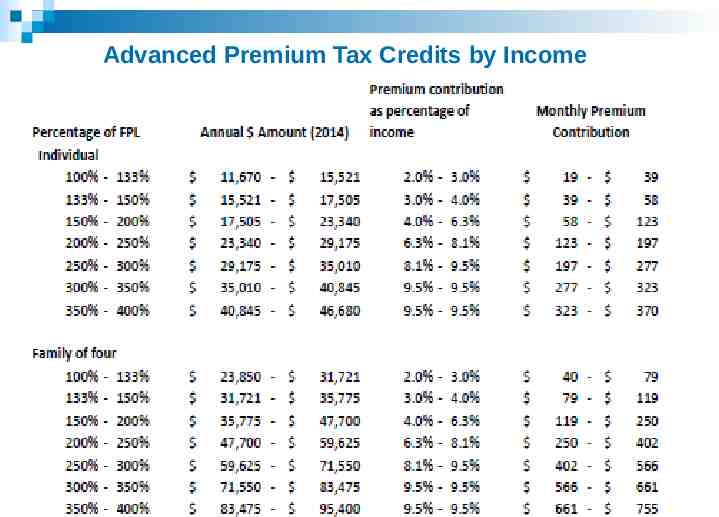

Advanced Premium Tax Credits by Income

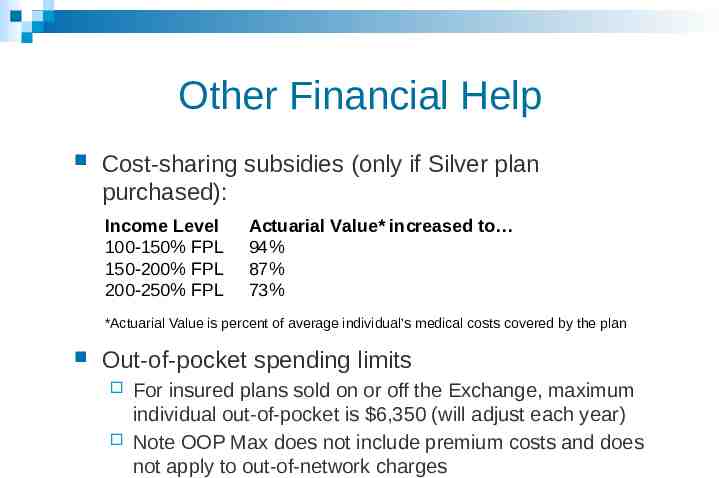

Other Financial Help Cost-sharing subsidies (only if Silver plan purchased): Income Level 100-150% FPL 150-200% FPL 200-250% FPL Actuarial Value* increased to 94% 87% 73% *Actuarial Value is percent of average individual’s medical costs covered by the plan Out-of-pocket spending limits For insured plans sold on or off the Exchange, maximum individual out-of-pocket is 6,350 (will adjust each year) Note OOP Max does not include premium costs and does not apply to out-of-network charges

Affordability Issues: The Family Glitch If an INDIVIDUAL has access to affordable coverage at work (defined as costing less than 9.5% of household income for employee-only coverage), and the FAMILY is offered coverage from the employer (even if there is no employer contribution) then the FAMILY cannot access subsidies in the Marketplace However, if the cost of FAMILY coverage for the spouse and dependents of a covered employee exceeds 8% of the household income, they are exempt from the penalty (but still not eligible for subsidies)

Affordability Issues: Employee Coverage Subsidies are not available for employees as long as the employer’s coverage is deemed affordable (less than 9.5% of household income) and credible (60% actuarial value). Unlike individual coverage in the Marketplace, where subsidies vary be income level, employee premiums do not vary by income nor does the definition of affordability.

Employer-sponsored Coverage: Common Issues/Questions (cont.) Employer Contributions to Individual Coverage There may be a way for employees to buy coverage outside the Marketplace using a 125 salary reduction agreement. Recent guidance seems to indicate that employers can supplement this to a certain extent under certain circumstances. (See your broker/tax professional for details.) However, there is no way for the employer to structure the plan so that the employee can use pre-tax contributions (from either the employer or employee) to purchase plans on the Marketplace and be eligible for individual subsidies

To offer or partially offer or not to offer, that is the question Three options: Offer to Employee and Dependents Offer to Employees Only (only if not subject to pay-or-play) Do Not Offer

To offer or partially offer or not to offer, that is the question Variables to consider Employer’s cost The coverage offered is tax deductible to the employer Potential need to increase salary to compensate for the reduction in total compensation (if eliminating existing coverage) Employee’s cost The cost of individual coverage is NOT tax deductible to the employee (as opposed to their contribution to employer coverage which is tax deductible) Coverage might be more expensive than their employer coverage is now, especially if they are not eligible for subsidies If an INDIVIDUAL has access to affordable coverage at work (defined as costing less than 9.5% of income for individual coverage), then the FAMILY cannot access subsidies in the Marketplace What is the competition doing Impact of decision in attracting and retaining employees

Businesses Specific Resources Government (business focused): http://business.usa.gov/healthcare Department of Labor FAQs: http://www.dol.gov/ebsa/faqs/ IRS: http://www.irs.gov/uac/Affordable-Care-Act-Tax-Provisions

Businesses Specific Resources Healthcare.gov tax credit estimator: https://www.healthcare.gov/small-business-tax-credit-calcul ator/ Healthcare.gov Full-time Equivalent Employee (FTE) Calculator: https://www.healthcare.gov/fte-calculator/ U C Berkeley Summary of Provisions Affecting Employer-Sponsored Insurance http://laborcenter.berkeley.edu/pdf/2010/ppaca10.pdf