Student Loan Debt: Good or Bad? Dameion Lovett FASFAA

31 Slides5.70 MB

Student Loan Debt: Good or Bad? Dameion Lovett FASFAA Outreach Coordinator/Financial Literacy/Debt Management

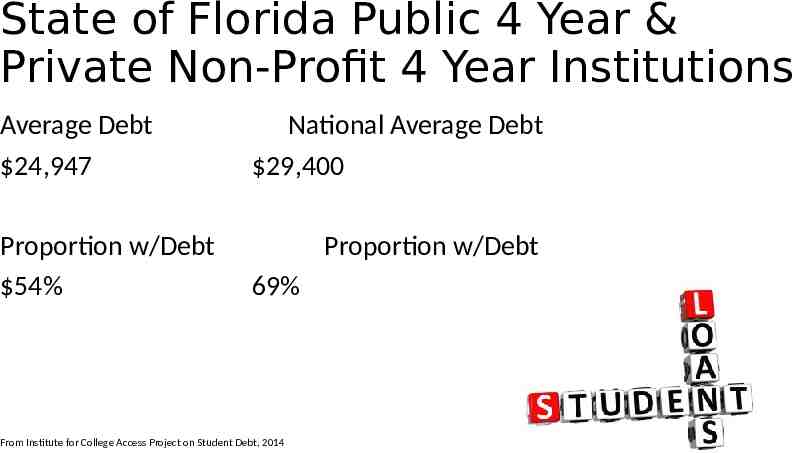

State of Florida Public 4 Year & Private Non-Profit 4 Year Institutions Average Debt 24,947 Proportion w/Debt 54% National Average Debt 29,400 Proportion w/Debt 69% From Institute for College Access Project on Student Debt, 2014

Is There A Student Loan Debt Crisis?

The Obvious Isn’t Always True “College educated people should understand their finances” “How hard can it be to add and subtract?” “If you don’t have it, don’t spend it” “Didn’t your parents teach you this?”

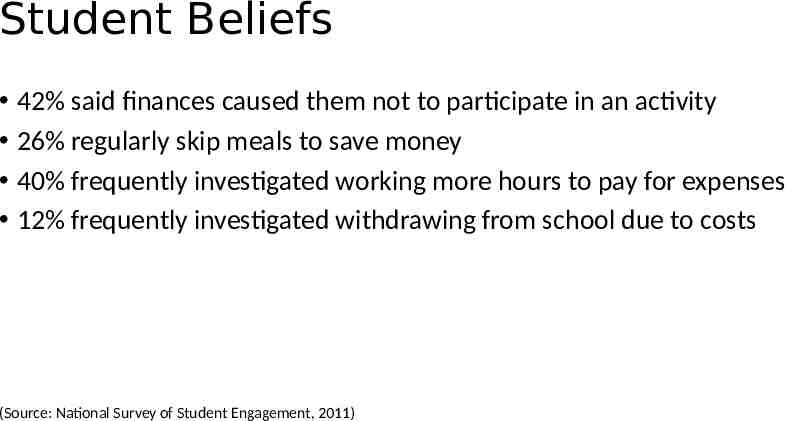

Student Beliefs 42% said finances caused them not to participate in an activity 26% regularly skip meals to save money 40% frequently investigated working more hours to pay for expenses 12% frequently investigated withdrawing from school due to costs (Source: National Survey of Student Engagement, 2011)

Is It Common Sense? You may know this, but your students probably don’t Students don’t recognize what’s happening to them and where the problems are coming from Students make poor choices Stress eating Stress spending Working more to have more spending money; supplying wants instead of needs Tend to look for instant gratification & short term results

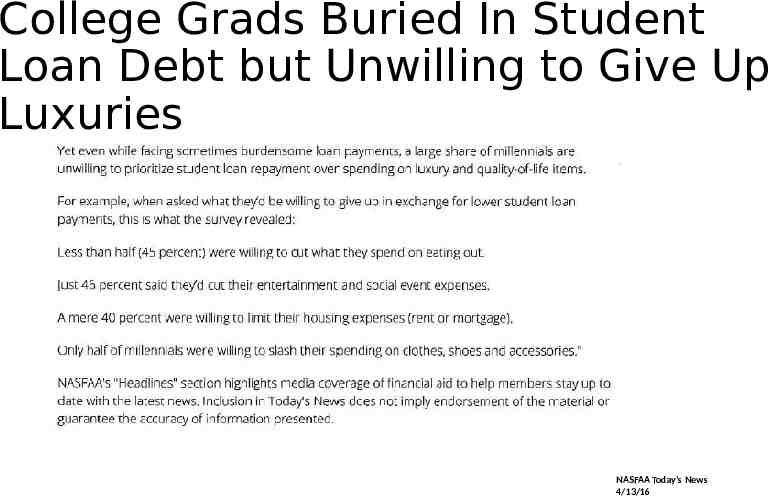

College Grads Buried In Student Loan Debt but Unwilling to Give Up Luxuries NASFAA Today’s News 4/13/16

“If You Think Education Is Expensive, Try Ignorance” Derek Bok

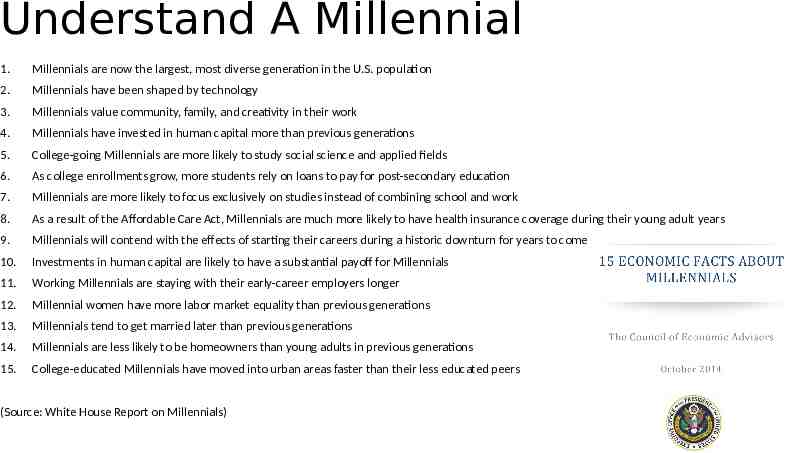

Understand A Millennial 1. Millennials are now the largest, most diverse generation in the U.S. population 2. Millennials have been shaped by technology 3. Millennials value community, family, and creativity in their work 4. Millennials have invested in human capital more than previous generations 5. College-going Millennials are more likely to study social science and applied fields 6. As college enrollments grow, more students rely on loans to pay for post-secondary education 7. Millennials are more likely to focus exclusively on studies instead of combining school and work 8. As a result of the Affordable Care Act, Millennials are much more likely to have health insurance coverage during their young adult years 9. Millennials will contend with the effects of starting their careers during a historic downturn for years to come 10. Investments in human capital are likely to have a substantial payoff for Millennials 11. Working Millennials are staying with their early-career employers longer 12. Millennial women have more labor market equality than previous generations 13. Millennials tend to get married later than previous generations 14. Millennials are less likely to be homeowners than young adults in previous generations 15. College-educated Millennials have moved into urban areas faster than their less educated peers (Source: White House Report on Millennials)

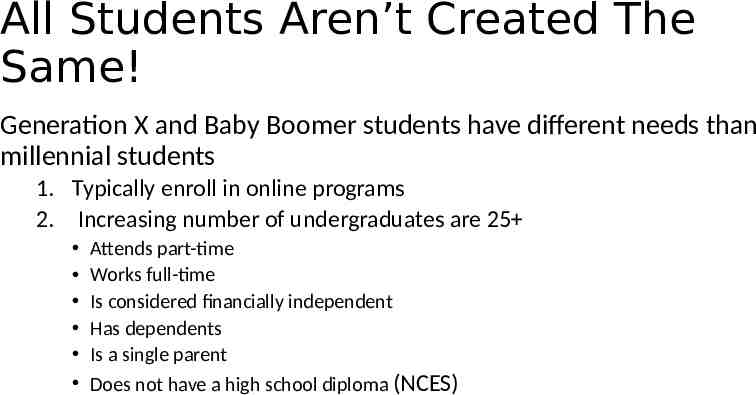

All Students Aren’t Created The Same! Generation X and Baby Boomer students have different needs than millennial students 1. Typically enroll in online programs 2. Increasing number of undergraduates are 25 Attends part-time Works full-time Is considered financially independent Has dependents Is a single parent Does not have a high school diploma (NCES)

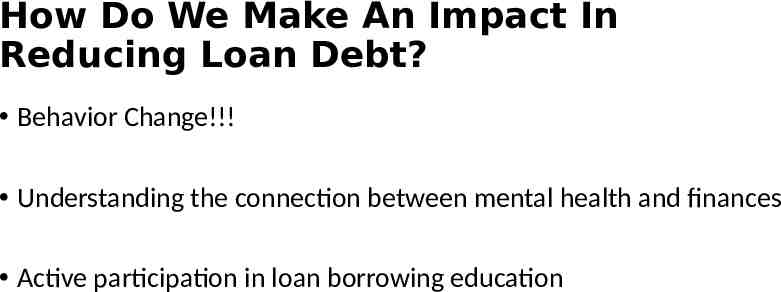

How Do We Make An Impact In Reducing Loan Debt? Behavior Change!!! Understanding the connection between mental health and finances Active participation in loan borrowing education

Momma Made Me Do It! Parents have greatest influence on developing positive financial attitudes & behaviors in young adults, until long-term romantic relationships become larger influence Source (Financial Behavior, Debt, and Early Life Transitions (2014), University of Arizona)

Financial Abstraction Money isn’t real so it doesn’t matter if we know how to manage it

The World Is Bigger Than Our Anxieties! Life altering decisions are made with as little understanding based on taking the minimum amount of time possible 18% say money is a taboo subject in their family 36% say talking about money makes them uncomfortable 69% say financial problems and conflicts are their primary cause of anxiety (Source: American Psychological Association, 2014)

Behavior Change

Can You Change Your Behavior? 1. Stand Up 2. Cross Your Arms 3. Let’s Talk

Mental Health & Finances

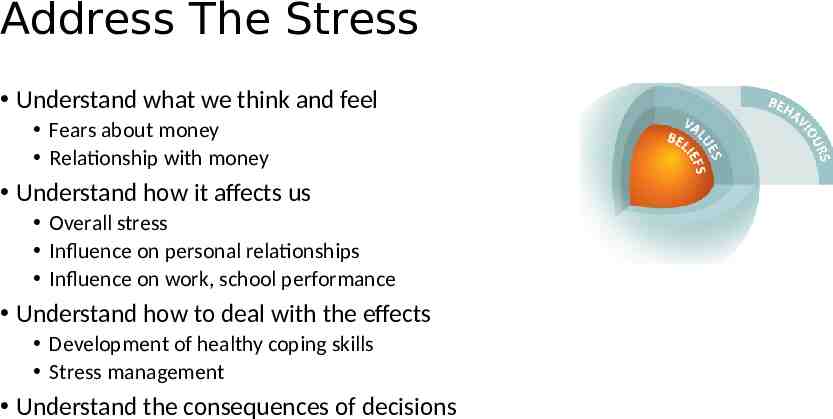

Address The Stress Understand what we think and feel Fears about money Relationship with money Understand how it affects us Overall stress Influence on personal relationships Influence on work, school performance Understand how to deal with the effects Development of healthy coping skills Stress management Understand the consequences of decisions

Effective Loan Borrowing Education

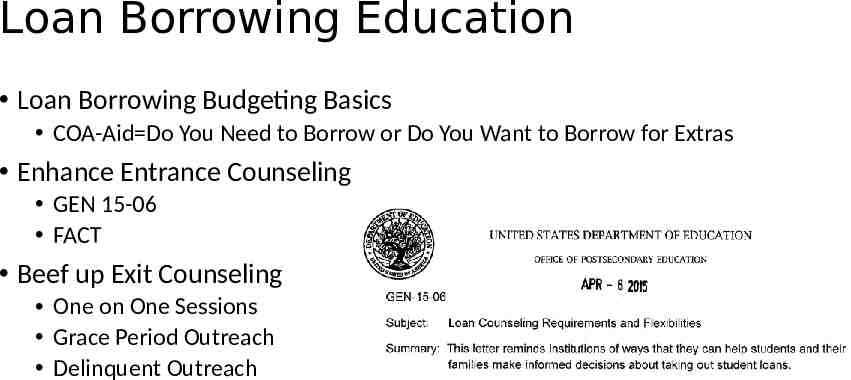

Loan Borrowing Education Loan Borrowing Budgeting Basics COA-Aid Do You Need to Borrow or Do You Want to Borrow for Extras Enhance Entrance Counseling GEN 15-06 FACT Beef up Exit Counseling One on One Sessions Grace Period Outreach Delinquent Outreach

Effective Entrance Counseling Texas Guarantee Research “A Time To Every Purpose: Understanding and Improving the Borrower Experience with Online Student Loan Entrance Counseling”

Effective Exit Counseling Texas Guarantee Research “From Passive To Proactive: Understanding and Improving the Borrower Experience with Online Student Loan Exit Counseling” Texas Guarantee Research “Above and Beyond: What Eight Colleges Are Doing to Improve Student Loan Counseling”

Pending Legislative Relief HR 3179: Empowering Students Through Enhanced Financial Counseling Act (Not a Law) Change the one-time entrance counseling requirement to an annual counseling requirement Must be completed before the student accepts the loan(s) Passive confirmation of subsequent loans would no longer be permitted Students must, annually, actively accept every loan by either signing a MPN or by signing a statement accepting the loan

Pending Legislative Relief HR 3179: Empowering Students Through Enhanced Financial Counseling Act (Not a Law) Contact information for the servicers of each of the borrower’s loans Summary of the outstanding balance of principle & interest due on loans made to the borrower Information on the repayment plans available, including a description of the different plans’ features based on the borrower’s outstanding balance— showing the anticipated monthly payments, the difference in interest paid and total payments under each plan

Simple Solutions Provide a number of financial literacy related information (programs, events, services) Offer information in a variety of formats (in person, online, group settings) Partner with admissions, housing, counseling & health services, student affairs, student organizations, career services, orientation Link loan borrowing to earnings and budgeting after graduation to maximize understanding and lifelong habit formation Understand your drop/stop-outs

Barriers Eliminate the stigma of seeking help It’s not sexy! Having open discussions of needs vs wants Time Resources

Little Things Add Up Over Time

Resources/References http://www.ticas.org/posd/map-state-data-2015# http://www.tgslc.org/research/counseling.cfm http:// digitalcommons.georgefox.edu/cgi/viewcontent.cgi?article 1008&context gfsb Money Savvy Students: www.moneysavvy.com/summit Colinryanspeaks.com National Summit on Collegiate Financial Wellness www.nscfw.org https://www.whitehouse.gov/sites/default/files/docs/millennials report.pdf National Endowment for Financial Education http://www.tgslc.org/research/counseling.cfm http://www.forbes.com/sites/elizabethharris/2016/08/31/the-real-answer-to-t he-student-loan-crisis-changing-borrower-behavior-says-study/2/# a13b8c1cf3ab

QUESTIONS Dameion Lovett Campus Director University of South Florida [email protected] Financial Education@USF “Bull2Bull” www.usf.edu/fin-ed