SBA 504 Lending Regulatory Considerations Randy Christiansen

14 Slides324.50 KB

SBA 504 Lending Regulatory Considerations Randy Christiansen National Bank Examiner OCC Large Bank Division 1

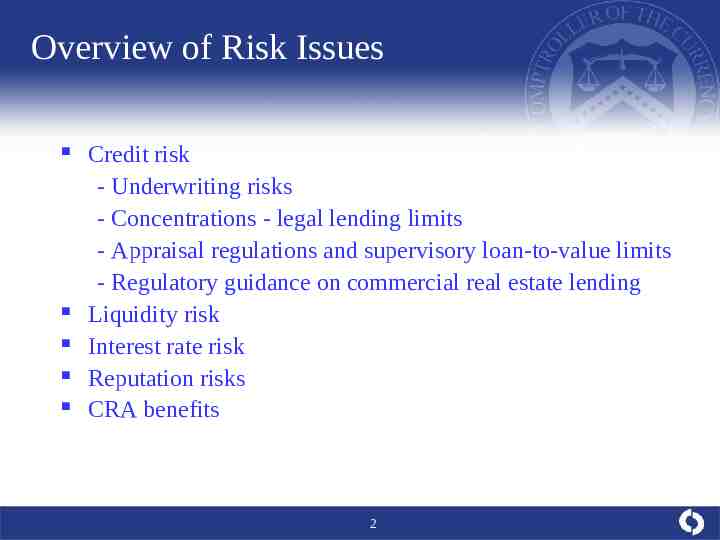

Overview of Risk Issues Credit risk - Underwriting risks - Concentrations - legal lending limits - Appraisal regulations and supervisory loan-to-value limits - Regulatory guidance on commercial real estate lending Liquidity risk Interest rate risk Reputation risks CRA benefits 2

Credit Risk Issues Underwriting Risks – Summary Favorable risk structure Above average obligor risk Below average collateral and structural risk Relatively low credit loss type of lending 3

Credit Risk Issues (continued) Underwriting Risks – Obligor Risk Above average risk of repayment Primary underwriting focus – repayment ability Principal or guarantor due diligence critical 4

Credit Risk Issues (continued) Underwriting Risks – Structure and Collateral Favorable structure and collateral protection CAUTION: Collateral based lending Losses can and do occur 5

Credit Risk Issues (continued) Credit Concentrations and Lending Limits Second lien loan Secondary market Quality underwriting and due diligence is key 6

Credit Risk Issues (continued) Appraisal Regulation Requirements Appraisal regulations apply Business loan exemption may apply Appraisal independence standards Qualified appraisers and quality appraisals Poor appraisals or environmental studies 7

Credit Risk Issues (continued) Supervisory Loan-to-Value (SLTV) Exceptions Temporary high LTV transaction High LTV status can be extended for construction loans SLTV monitoring and reporting 8

Credit Risk Issues (continued) Commercial Real Estate Risk Management Guidance Owner occupied exemption Development or construction phase Majority of cash flow test 9

Liquidity Risk Issues Take-Outs and Secondary Market Second lien take-out Active secondary market Repurchases 10

Interest Rate Risk Issues Rate Risk Management Negotiable rate structures Secondary market 11

Reputation Risks CDC and SBA Secondary Market Borrower 12

Community Reinvestment Act (CRA) Small business development Job creation, community and economic development Consideration given in CRA examinations CRA consideration a function of bank and loan size - Loans of 1 million or less may qualify as small business loans - Loans greater than 1 million may qualify as community development loans 13

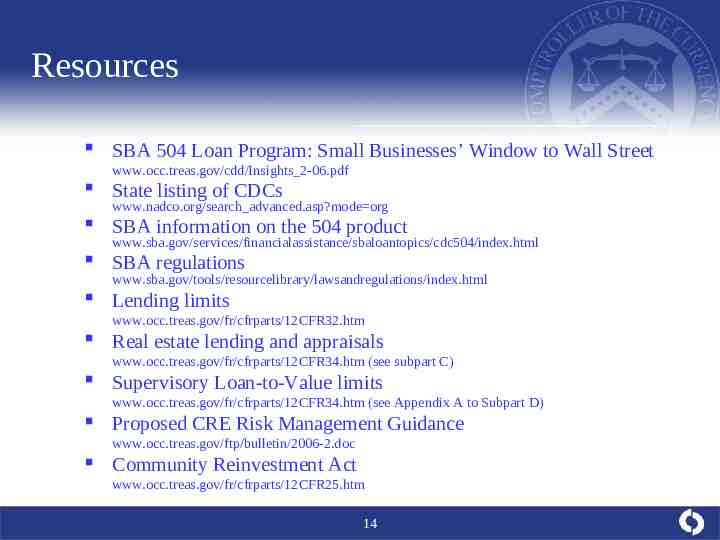

Resources SBA 504 Loan Program: Small Businesses’ Window to Wall Street www.occ.treas.gov/cdd/Insights 2-06.pdf State listing of CDCs www.nadco.org/search advanced.asp?mode org SBA information on the 504 product www.sba.gov/services/financialassistance/sbaloantopics/cdc504/index.html SBA regulations www.sba.gov/tools/resourcelibrary/lawsandregulations/index.html Lending limits www.occ.treas.gov/fr/cfrparts/12CFR32.htm Real estate lending and appraisals www.occ.treas.gov/fr/cfrparts/12CFR34.htm (see subpart C) Supervisory Loan-to-Value limits www.occ.treas.gov/fr/cfrparts/12CFR34.htm (see Appendix A to Subpart D) Proposed CRE Risk Management Guidance www.occ.treas.gov/ftp/bulletin/2006-2.doc Community Reinvestment Act www.occ.treas.gov/fr/cfrparts/12CFR25.htm 14