Reverse Mortgages for Senior Homeowners Cindy Stokes Utah

30 Slides904.50 KB

Reverse Mortgages for Senior Homeowners Cindy Stokes Utah State University (adapted from AARP information)

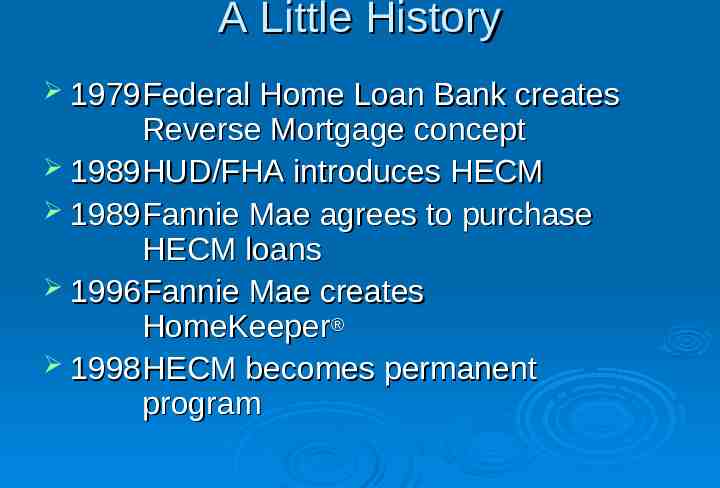

A Little History 1979 Federal Home Loan Bank creates Reverse Mortgage concept 1989 HUD/FHA introduces HECM 1989 Fannie Mae agrees to purchase HECM loans 1996 Fannie Mae creates HomeKeeper 1998 HECM becomes permanent program

Home Equity Conversion Mortgage Designed by HUD Insured by FHA Payments continue as long as one homeowner remains in home Loan balance not due until borrowers die or leave the home Total due lender cannot exceed value of home at time of sale

HECM Basic Requirements Borrowers must be at least 62 years old Home must be FHA approved Borrowers must live in home as principal residence At least one homeowner must reside in home at time of closing Home must be free of debt or nearly paid off Borrowers must receive reverse mortgage counseling Owners must not be in, or filing for, bankruptcy. Owners can be in foreclosure.

HECM Counseling Required 2-hour session HUD-approved counseling agency Free of charge Includes discussion of other alternatives Certificate of HECM Counseling issued, good for 180 days

Safeguards Loan never becomes due until last homeowner leaves the home Payments continue even if payments exceed value of the home No repayment required of amount paid out in excess of value of the home If lender fails, FHA will make payments FHA covers any shortfall if amount due exceeds value of the home

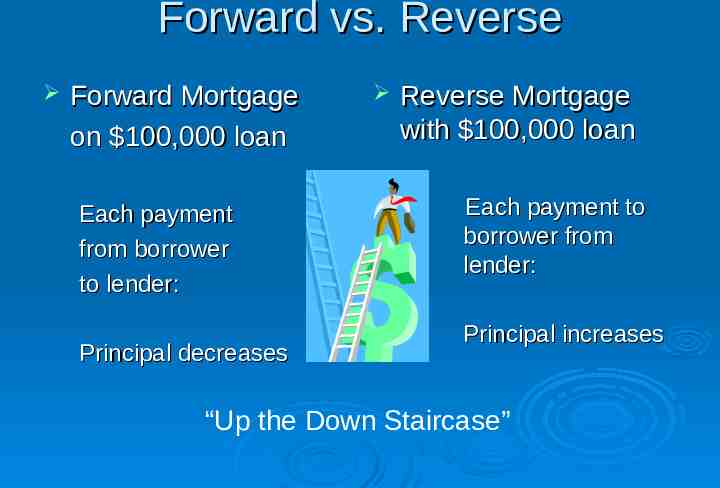

Forward vs. Reverse Forward Mortgage on 100,000 loan Each payment from borrower to lender: Principal decreases Reverse Mortgage with 100,000 loan Each payment to borrower from lender: Principal increases “Up the Down Staircase”

Reverse Mortgage Features No income-qualifying requirements Title to property remains in borrower’s name Borrower remains responsible for payment of taxes and insurance Total loan balance not due until last homeowner leaves the property Total amount due lender cannot exceed value of home at time loan is repaid

HECM Eligibility Requirements All owners must be at least 62 years old Home must be their principal residence at least 6 months of year At least one homeowner must reside in home at time of closing Borrowers must receive reverse mortgage counseling The Homeowners

HECM Eligibility Requirements The Home Can be single-family, 1 to 4 unit owner occupied, FHAapproved condominium, PUD, or manufactured home Must meet minimum FHA property standards

HECM Eligibility Requirements Any existing mortgage must be paid off at closing HECM must be first mortgage but can be used to pay off existing debt FHA mortgage insurance required Origination and Servicing fees The Loan

How Much Can Be Borrowed Total amount available is based on: Age of borrowers Value of property Average interest rate

“How Much Can I Get?” Location, Location, Location Market value at time of closing Maximum loan limits Equity in the home Age of borrowers Interest rate

Reverse Mortgage Calculator When were you born? When was your spouse or co-owner born? How much is your house worth? Your ZIP Code http://www.rmaarp.com/

Four Basic Plans Tenure - Monthly payments for life Term number Monthly payments for set of years Line of Credit - Draws in amount and time of borrower’s choosing Lump Sum at Total amount available drawn closing

Tenure Plan Monthly payments for life Advances are secured by mortgage or deed of trust Amount of payment remains fixed Interest, insurance, and servicing fees added each month Total loan balance increases every month No payment due until last homeowner dies or leaves the property

Term Plan Amount available calculated same as for Tenure Plan Payments made for set number of years Borrower designates number of years At end of term, payments stop Repayment of total loan balance not due until last homeowner leaves the home Monthly amount received depends on length of time payments are desired

Amount of Monthly Payment Actual amount to be received monthly is based on: Location of home Value of home Equity in home Age of youngest homeowner Interest rate at time of closing

Line of Credit Plan Line of credit established based on equity Homeowner can draw any amount at any time until available principal is depleted Interest is charged only on amount drawn No repayment is required until last homeowner either dies or leaves the home Amount of cash available increases Needs to be used to be cost-effective

Lump Sum Plan Calculated same as Tenure or Term One lump sum of all available funds drawn at closing Can be combined with tenure or term plan Interest is calculated and charged each month along with insurance and servicing Total balance becomes due whenever property is sold

The Process Step 1: Counseling 2-hour session Certificate of HECM Counseling good for 180 days Step 2: Find a Lender www.hud.gov www.fanniemae.com www.aarp.org

Things to Consider Cost - Origination & Servicing Fees Experience - Number of Reverse Mortgages Servicing - Administrative Costs Commitment - Professional Relationships

Closing Costs for RM Loan Total Annual Loan Cost (TALC) Application Fee Appraisal and Credit Check Origination Fee Preparation and Processing Closing Costs/3rd Party Closing Costs (varies) Title search and insurance, survey, inspection, recording fees, property tax Mortgage Insurance Premium HECM loan 2% of value or 2000 – can be financed

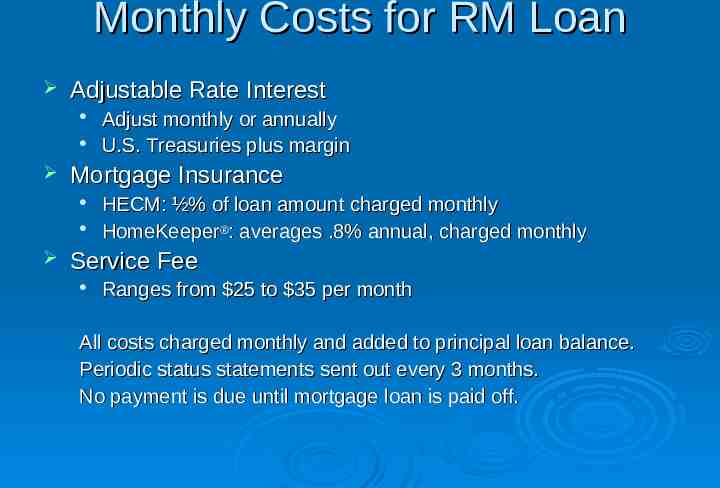

Monthly Costs for RM Loan Adjustable Rate Interest Mortgage Insurance Adjust monthly or annually U.S. Treasuries plus margin HECM: ½% of loan amount charged monthly HomeKeeper : averages .8% annual, charged monthly Service Fee Ranges from 25 to 35 per month All costs charged monthly and added to principal loan balance. Periodic status statements sent out every 3 months. No payment is due until mortgage loan is paid off.

Additional Costs Homeowner Insurance and Property Tax Maintenance and Repairs

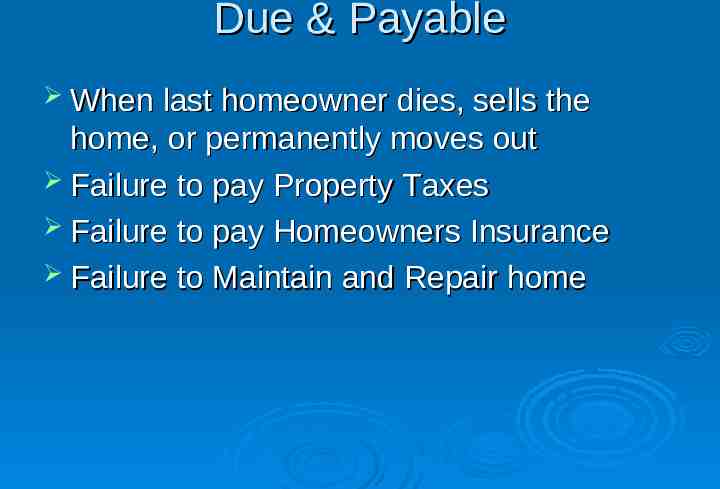

Due & Payable When last homeowner dies, sells the home, or permanently moves out Failure to pay Property Taxes Failure to pay Homeowners Insurance Failure to Maintain and Repair home

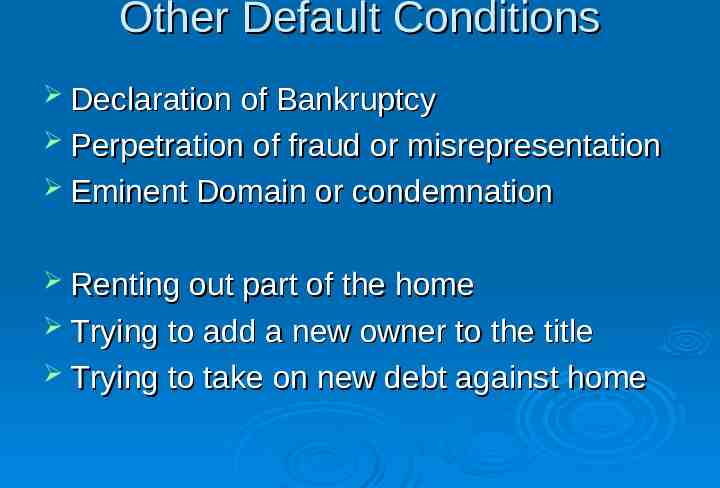

Other Default Conditions Declaration of Bankruptcy Perpetration of fraud or misrepresentation Eminent Domain or condemnation Renting out part of the home Trying to add a new owner to the title Trying to take on new debt against home

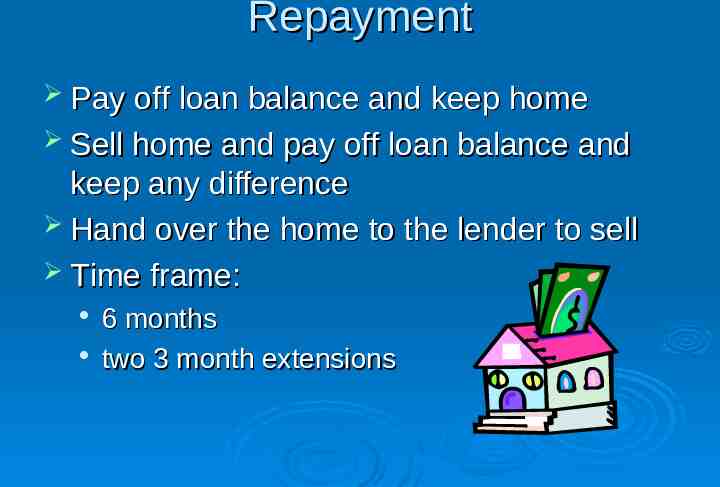

Repayment Pay off loan balance and keep home Sell home and pay off loan balance and keep any difference Hand over the home to the lender to sell Time frame: 6 months two 3 month extensions

Key Decisions Who else should I involve in considering this loan? Which counselors should I choose? Have I given due consideration to all my choices? When would be the best time to take out a reverse mortgage? What interest rate should I choose? Which lender should I choose? How should I use this loan?

AARP Booklet: Home Made Money To order a complimentary copy by phone: Call 1-800-209-8085. To order a complimentary copy online: http://www.aarp.org/money/revmort/ revmort basics/a2003-04-07homemademoney.html