QDROs: Dividing 401(k)s, Private-Sector Pensions, and Massachusetts

37 Slides205.21 KB

QDROs: Dividing 401(k)s, Private-Sector Pensions, and Massachusetts Public Pensions in Divorce William S. Young, Esq. WSY Law PLLC PO Box 155, Roslindale, MA 02131 (617) 363-0000 [email protected] December 2023

Overview Part Part Part Part Part Part Part Part 1. 2. 3. 4. 5. 6. 7. 8. Retirement Assets & Pension Basics Division of Retirement Assets in Divorce Dividing Defined Contribution Plans Dividing Pensions – Concepts Dividing Public Pensions The QDRO Process – a quick summary Separation Agreements – Anticipating the QDRO Common Pitfalls www.qdrocounselor.com

Retirement crisis - Problem: - Inadequate account balances - Lack of needed retirement income - Risk of downward mobility in retirement - Causes: - Lack of coverage to any plan - Switch to 401(k)s: low participation, high fees, benefits primarily for high-income workers Source: Teresa Ghilarducci, Backgrounder: The Retirement Crisis (The New School Schwartz Center for Economic Policy Analysis) (2018) www.qdrocounselor.com

Access to and participation in 401(k)s & pensions Bureau of Labor Statistics, U.S. Department of Labor, The Economics Daily, Retirement plans for workers in private industry and state and local government in 2022 at https://www.bls.gov/opub/ted/2023/retirement-plans-for-workers-in-private-industry-and-state-and-local-government-in-2022.htm (visited April 10, 2023) www.qdrocounselor.com

Access to Cash Balance (“nontraditional”) plans Bureau of Labor Statistics, U.S. Department of Labor, The Economics Daily, Retirement plans for workers in private industry and state and local government in 2022 at https://www.bls.gov/opub/ted/2023/retirement-plans-for-workers-in-private-industry-and-state-and-local-government-in-2022.htm (visited April 10, 2023) www.qdrocounselor.com

A little history Embezzlement & underfunding Studebaker bankruptcy in 1961, see James Wooten, “The Most Glorious Story of Failure in the Business: The Studebaker-Packard Corporation and the Origins of ERISA” (2001) Pensions: The Broken Promise (1972), available at https://www.youtube.com/watch?v Sjxidl8C kU Employee Retirement Income Security Act (“ERISA”) (1974) www.qdrocounselor.com

Why a court order? A court order is necessary to get around anti-alienation rules. ERISA bars retirement funds from giving away participant money. Retirement Equity Act (1984) provides specific exceptions (marital property, child support, spousal support). I.R.C. 414(p) codifies definition of a Qualified Domestic Relations Order (“QDRO”). Definitions of “participant”, “alternate payee”, etc. www.qdrocounselor.com

QDROs, defined at I.R.C 414(p) A domestic relations order which creates or recognizes the existence of an alternate payee’s right to, or assigns to an alternate payee the right to, receive all or a portion of the benefits payable with respect to a participant under a plan and clearly specifies: - The name and last known mailing address of each alternate payee the amount or percentage of the participant’s benefits to be paid by the plan to each such alternate payee, or the manner in which such amount or percentage is to be determined the number of payments or period to which such order applies, and each plan to which such order applies. * The order may not alter amount, form, etc., of benefits (from would otherwise be available to the participant). Plan shall establish reasonable procedures to determine the qualified status of domestic relations orders and to administer distributions under such qualified orders. Massachusetts public pensions divided by “DRO” (not “QDRO”) www.qdrocounselor.com

Guidance - DOL: “FAQs about Qualified Domestic Relations Orders” - DOL: “QDROs: The Division of Retirement Benefits Through Qualified Domestic Relations Orders” www.qdrocounselor.com

Division basics in MA G.L. c. 208 § 34 allows division of retirement benefits Defined contribution plans (401(k)s, 403(b)s, etc), and defined benefit plans (pensions & cash balance plans) can be divided by court order (DROs and QDROs) QDROs are based on separation agreement www.qdrocounselor.com

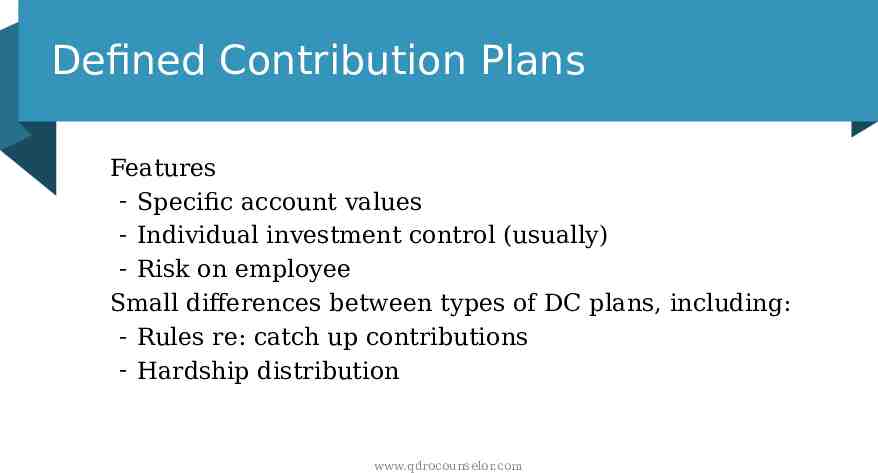

Defined Contribution Plans Features - Specific account values - Individual investment control (usually) - Risk on employee Small differences between types of DC plans, including: - Rules re: catch up contributions - Hardship distribution www.qdrocounselor.com

Defined Contribution Plan QDROs QDROs follow separation agreement - Must state or % or specify assets - Loans included? - Should specify a particular date - Should specify whether to include subsequent investment performance Examples - “ 10,000 as of the date of divorce nisi, adjusted for subsequent investment performance” or - “40% of the vested account balance, exclusive of any loans, as of January 1, 2020” www.qdrocounselor.com

Defined Contribution Plan QDROs: Questions and Advice When drafting the separation agreement, consider: main formula premarital contributions (are records are available?) loans How to ensure timely completion to avoid runaway funds These issues will affect the terms and viability of the QDRO. www.qdrocounselor.com

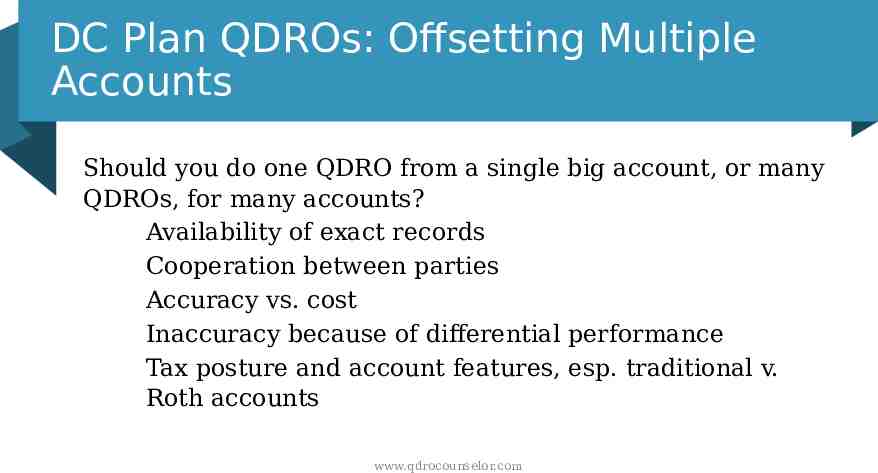

DC Plan QDROs: Offsetting Multiple Accounts Should you do one QDRO from a single big account, or many QDROs, for many accounts? Availability of exact records Cooperation between parties Accuracy vs. cost Inaccuracy because of differential performance Tax posture and account features, esp. traditional v. Roth accounts www.qdrocounselor.com

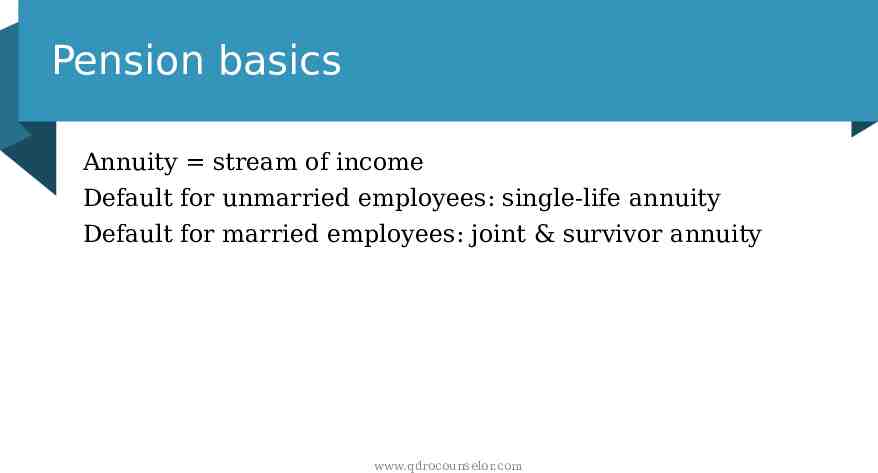

Pension basics Annuity stream of income Default for unmarried employees: single-life annuity Default for married employees: joint & survivor annuity www.qdrocounselor.com

Pension formulas - Formulas - Flat payout per year (e.g., monthly benefit years of service * 100) - Final average pay (e.g., monthly benefit years of service * 0.1% * FAP) - More complicated formulas - Vesting - See plan’s summary plan description (or plan document) for details www.qdrocounselor.com

Cash Balance Plans - Notional account, controlled by employer - Interest credits (typically 4.5 or 5%), not investment performance - Legally, a type of defined benefit (pension) plan www.qdrocounselor.com

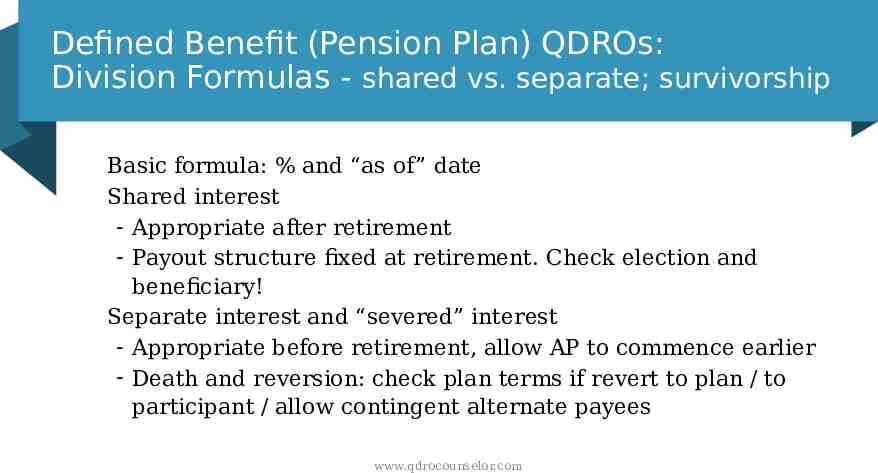

Defined Benefit (Pension Plan) QDROs: Division Formulas - shared vs. separate; survivorship Basic formula: % and “as of” date Shared interest - Appropriate after retirement - Payout structure fixed at retirement. Check election and beneficiary! Separate interest and “severed” interest - Appropriate before retirement, allow AP to commence earlier - Death and reversion: check plan terms if revert to plan / to participant / allow contingent alternate payees www.qdrocounselor.com

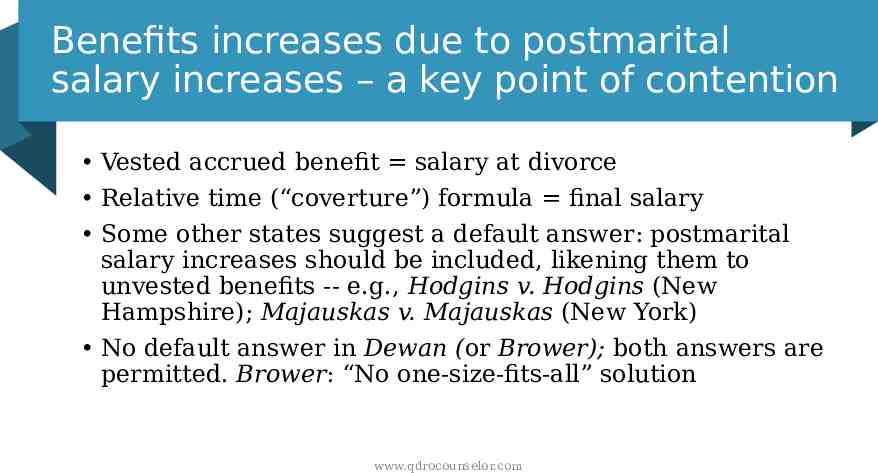

Benefits increases due to postmarital salary increases – a key point of contention Vested accrued benefit salary at divorce Relative time (“coverture”) formula final salary Some other states suggest a default answer: postmarital salary increases should be included, likening them to unvested benefits -- e.g., Hodgins v. Hodgins (New Hampshire); Majauskas v. Majauskas (New York) No default answer in Dewan (or Brower); both answers are permitted. Brower: “No one-size-fits-all” solution www.qdrocounselor.com

Other benefits increases Cost of living adjustments Early retirement subsidies Disability pay Ad hoc benefits increases www.qdrocounselor.com

Some case law basics Rice v. Rice, Mass. (1977): Trial just has discretion to assign to one spouse the property of the other whenever and however acquired Brower v. Brower, Mass App Ct. (1984): No “one size fits all” rule for division; ultimate consideration is fairness Moriarty v. Stone, Mass App Ct. (1996): Can assign premarital benefits Dewan v. Dewan, Mass App Ct. (1983): Contemporaneous division preferred, offsets permissible Contributory Retirement Board of Arlington vs. Mangiacotti, 406 Mass. 184 (1989): Massachusetts public pensions are divisible by court order www.qdrocounselor.com

Additional considerations Survivorship Reversion Dividing Cash Balance Plans Purposes & taxation www.qdrocounselor.com

Massachusetts Public Pensions Defined benefit plans Two funding sources: employee contributory account and taxpayer money Paid as shared interest Basic formula set by statute: age, salary, & service www.qdrocounselor.com

MA Public Pensions: Key Issues Superannuation Ordinary disability Accidental disability Preretirement survivor benefits Postretirement survivor benefits: Option A/B/C Refund of participant’s annuity account www.qdrocounselor.com

MA Public Pensions: Superannuation Superannuation benefits defined by G. L. c. 32, §5 Workers typically vest after 10 years of service, can retire after 20 years of service at age 55; earlier, for public safety officers Benefit calculated by statutory age factor, years and months of service, and salary at retirement www.qdrocounselor.com

MA Public Pensions: DRO Superannuation Formulas Superannuation: “old enough” pension (what the worker expects) Formulas typically differ on salary (as with private sector pensions) Formulas: - “Deferred vested” or “Static” formula: age at retirement, service as of the divorce (or during the marriage), and salary at divorce - “Active” or “Dynamic” formula: age at retirement, service as of the divorce (or during the marriage), and salary at retirement - Other formulas permitted (relative time; specific monthly amounts, etc.) www.qdrocounselor.com

MA Public Pensions: Advanced Question We’re not limited to deferred vested or active formulas. Salary factor may vary: meet in the middle, with a complex formula based on salary sometime between divorce and retirement; or separation, especially if significantly prior to divorce Service and age factors may vary: be careful, as the service and age requirements vary for different groups of employees But: formula must be clear to, and feasible to implement by, the retirement board www.qdrocounselor.com

MA Public Pensions: Ordinary Disability Retirement Defined by G.L. c. 32, §6 For injury outside performance of duties Equal to the superannuation benefit as if participant were age 55, if younger Typically divided parallel to superannuation benefit www.qdrocounselor.com

MA Public Pensions: Accidental Disability Defined by G.L. c. 32, §7 Injury in the performance of work duties Increases automatically to 72% Key question: Should the former spouse share in this increase? www.qdrocounselor.com

MA Public Pensions: Preretirement Benefits and Participant’s Remarriage. Watch out! G.L. c. 32, §12(2)(d): employee (participant) may elect a single preretirement survivor annuity beneficiary. Named beneficiary can’t remarry before retirement If employee remarries before retirement, new spouse has “dibs” (after a year) on the entire survivor benefit, potentially depriving the former spouse of all awarded pension benefits. Solution: life insurance upon remarriage? www.qdrocounselor.com

MA Public Pensions: 12(2)(d), but why? Thinking question: What policy aim does the c. 32 sec. 12(2)(d) restriction serve? Does it merit the hassle to every divorcing couple? www.qdrocounselor.com

MA Public Pensions: Postretirement Survivor Benefits (Option A/B/C) Defined by G.L. c. 32, §12(2)(a)-(c) Superannuation or disability benefits end upon the participant’s death Option A: single life annuity. No “cost” Option B: refund of contributions and interest (to one or more beneficiaries). Lump sum, no stream of income. Cost 1-5% Option C: survivor annuity 60% of option A benefit (after reducing for “cost”). Cost 7-15%, depending on ages “Cost” reduction during joint lifetimes to pay for the survivor benefits N.B.: If AP dies first, employee annuity “pops up” to full Option www.qdrocounselor.com A benefit

MA Public Pensions: Refund of Participant’s Annuity Account If the employee doesn’t vest, or quits and cashes out, employee can refund the annuity account to one or more beneficiaries. Split: 50% as of divorce/from marriage to divorce, with interest? Or otherwise? www.qdrocounselor.com

QDRO Preparation Process: Step by Step Information gathering Drafting Party/attorney review Preapproval Submission to court Qualification Review Interpretation www.qdrocounselor.com

Separation agreements Identify retirement assets Determine valuation date Address each class of asset separately Offset within each class Consult an actuary if offsetting pensions Detailed description of each division formula – discuss shared/separate interest, final average pay considerations, etc. Phrasing here provides the basics for the QDRO(s) www.qdrocounselor.com

Common Pitfalls Process: Misunderstanding the nature of an asset – categorize it correctly Failure to review SPD and benefits statements Clients often misunderstand what they have Expecting a pension to pay immediately Failure to explain that a “separate interest” order means actuarial adjustment Failing to get the QDROs done before a party retires or dies Substance of agreement: Failing to include an “as of” date Failing to specify the division formula Neglecting survivorship and cost thereof Assuming retroactive application Failing to specify who pays cost of QDROs www.qdrocounselor.com

Ask for help! Call a QDRO specialist during the bargaining process I’ll be happy to tell you all this again William S. Young, Esq. www.qdrocounselor.com