PROACTIVE TAX PLANNING Proactive Tax Planning for the SECURE

28 Slides8.32 MB

PROACTIVE TAX PLANNING Proactive Tax Planning for the SECURE Act Presented By: Your Name Company

Five Key Areas of Financial Planning 1. Preservation Planning 2. Retirement Planning 3. Tax Planning 4. Estate Planning 5. Investment Planning

Proactive Tax Planning with the SECURE ACT The Setting Every Community Up for Retirement Enhancement Act of 2019 or SECURE Act is one of the largest assortments of retirement plan reforms. The SECURE Act contained numerous provisions intended to make it easier for businesses to offer retirement plans and for individuals to save for retirement. It also made significant changes impacting existing retirement plans.

Proactive Tax Planning with the SECURE ACT RMD age raised from 70 ½ to 72.

Proactive Tax Planning with the SECURE ACT Age limit for traditional IRA contributions eliminated. Formerly 70½. Watch out for Qualified Charitable Distributions complications!

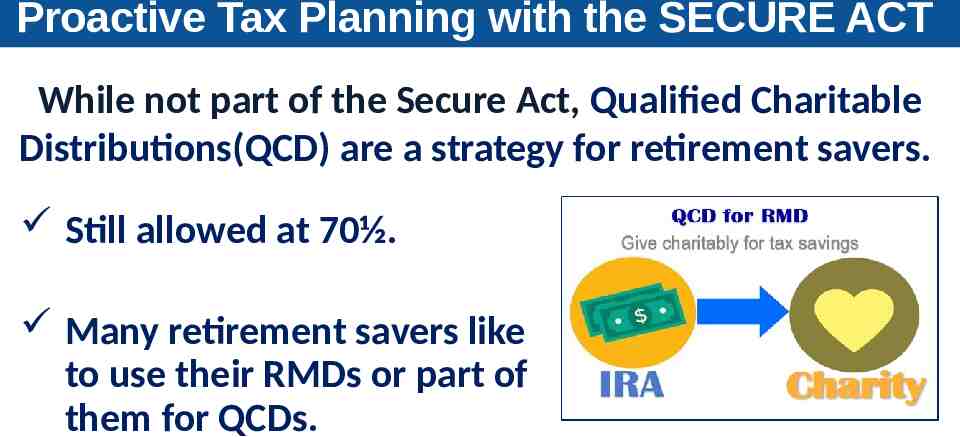

Proactive Tax Planning with the SECURE ACT While not part of the Secure Act, Qualified Charitable Distributions(QCD) are a strategy for retirement savers. Still allowed at 70½. Many retirement savers like to use their RMDs or part of them for QCDs.

Proactive Tax Planning with the SECURE ACT New 529 Educational Fund Rules Can use up to 10,000 for qualified student loan repayments.

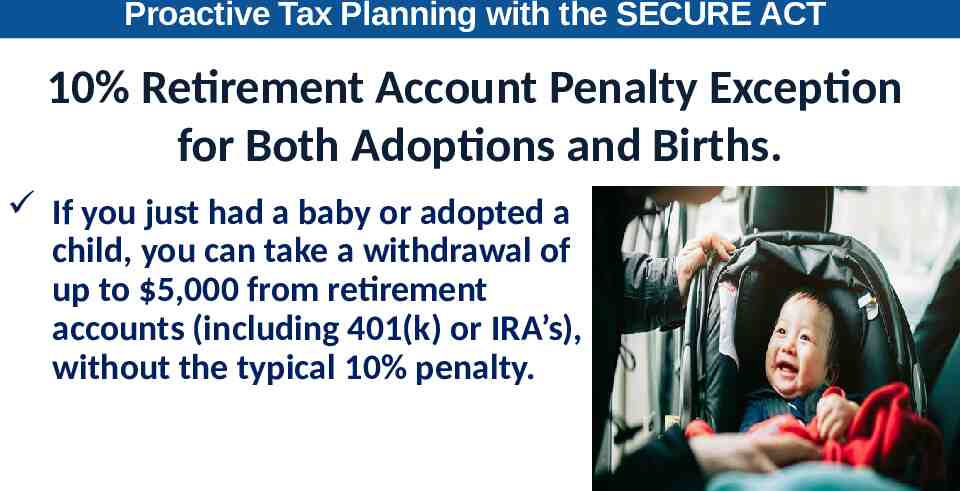

Proactive Tax Planning with the SECURE ACT 10% Retirement Account Penalty Exception for Both Adoptions and Births. If you just had a baby or adopted a child, you can take a withdrawal of up to 5,000 from retirement accounts (including 401(k) or IRA’s), without the typical 10% penalty.

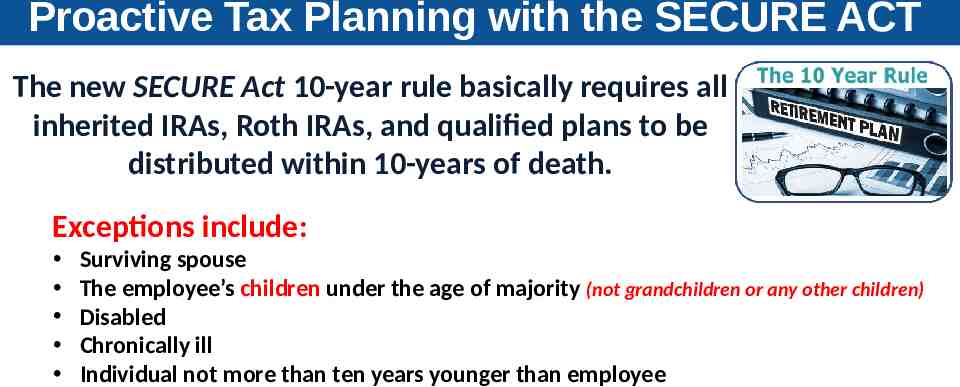

Proactive Tax Planning with the SECURE ACT The new SECURE Act 10-year rule basically requires all inherited IRAs, Roth IRAs, and qualified plans to be distributed within 10-years of death. Exceptions include: Surviving spouse The employee’s children under the age of majority (not grandchildren or any other children) Disabled Chronically ill Individual not more than ten years younger than employee

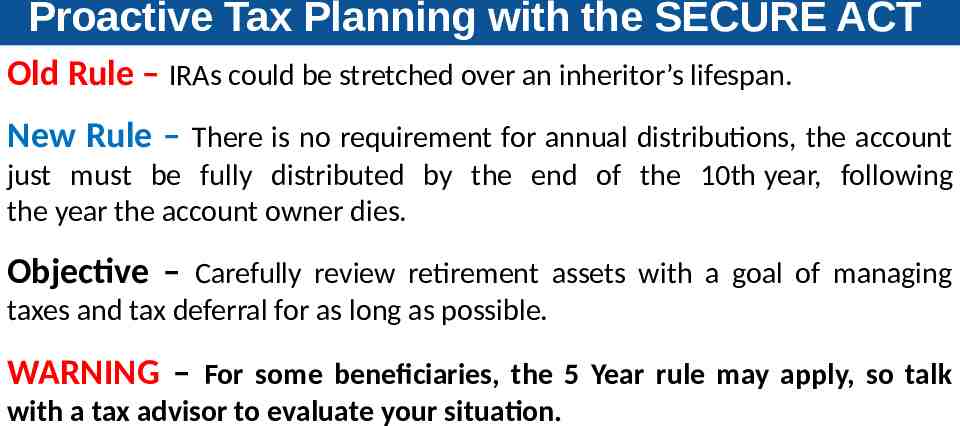

Proactive Tax Planning with the SECURE ACT Old Rule – IRAs could be stretched over an inheritor’s lifespan. New Rule – There is no requirement for annual distributions, the account just must be fully distributed by the end of the 10th year, following the year the account owner dies. Objective – Carefully review retirement assets with a goal of managing taxes and tax deferral for as long as possible. WARNING – For some beneficiaries, the 5 Year rule may apply, so talk with a tax advisor to evaluate your situation.

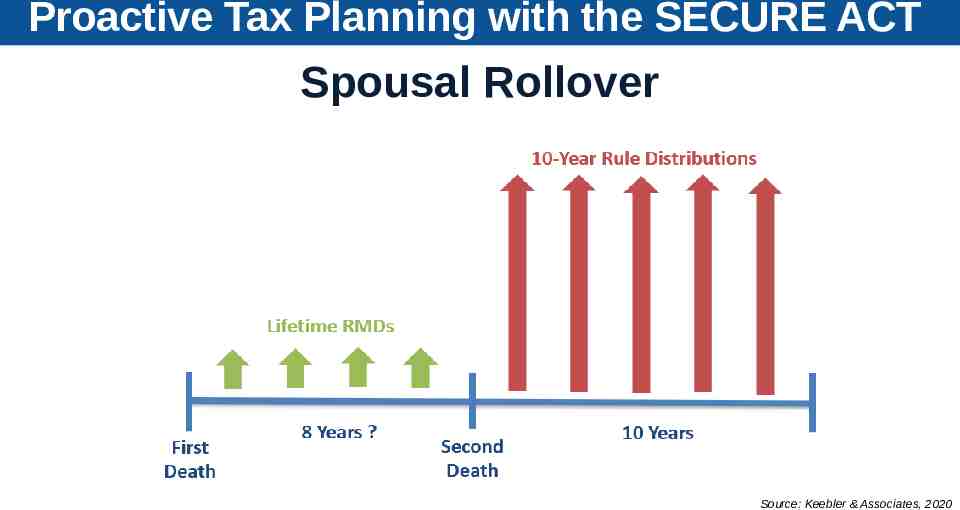

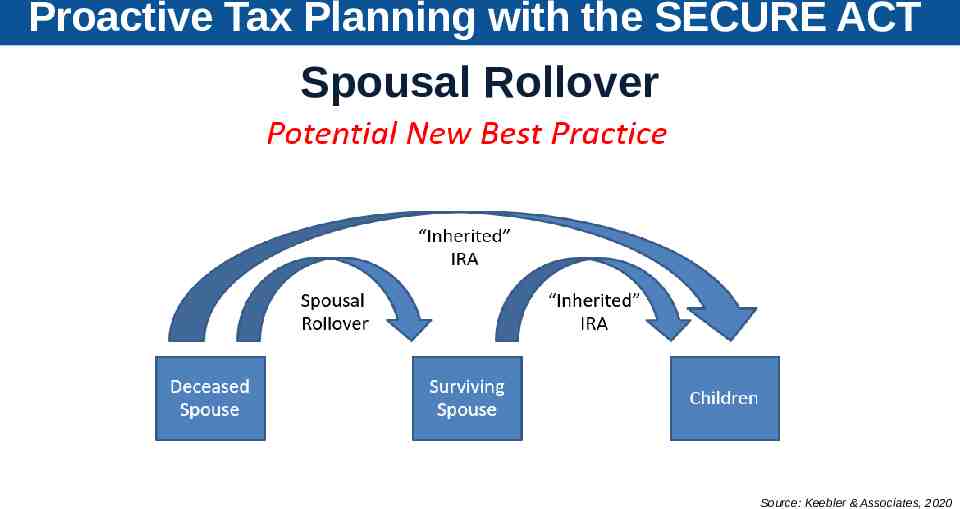

Proactive Tax Planning with the SECURE ACT Spousal Rollover Source: Keebler & Associates, 2020

Proactive Tax Planning with the SECURE ACT Spousal Rollover Source: Keebler & Associates, 2020

Proactive Tax Planning with the SECURE ACT Spousal Rollover Source: Keebler & Associates, 2020

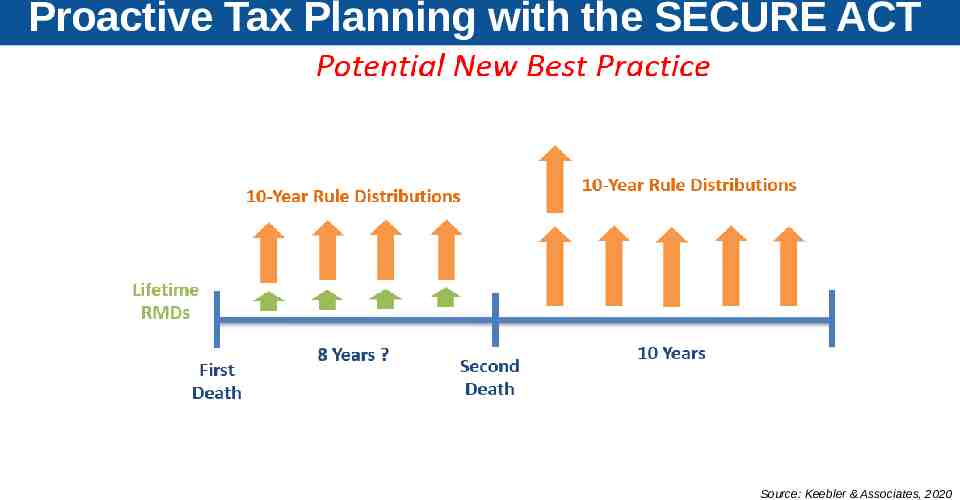

Proactive Tax Planning with the SECURE ACT Source: Keebler & Associates, 2020

Proactive Tax Planning with the SECURE ACT The new 10–Year rule reminds us that a proactive approach could potentially reap rewards. To maximize your situation under the new 10-year rule, you may want to consider Roth conversions and possibly spreading distributions over many years and lower brackets.

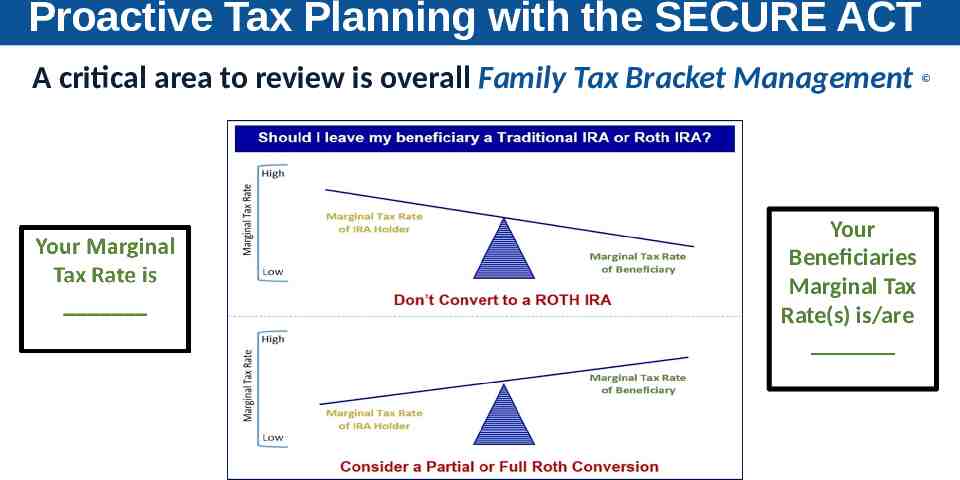

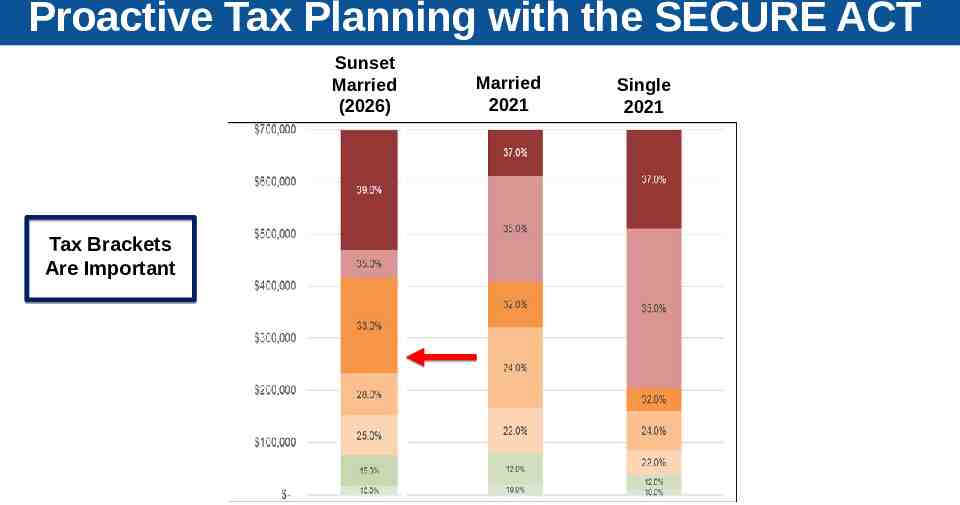

Proactive Tax Planning with the SECURE ACT A critical area to review is overall Family Tax Bracket Management Your Beneficiaries Marginal Tax Rate(s) is/are

Proactive Tax Planning with the SECURE ACT Sunset Married (2026) Tax Brackets Are Important Married 2021 Single 2021

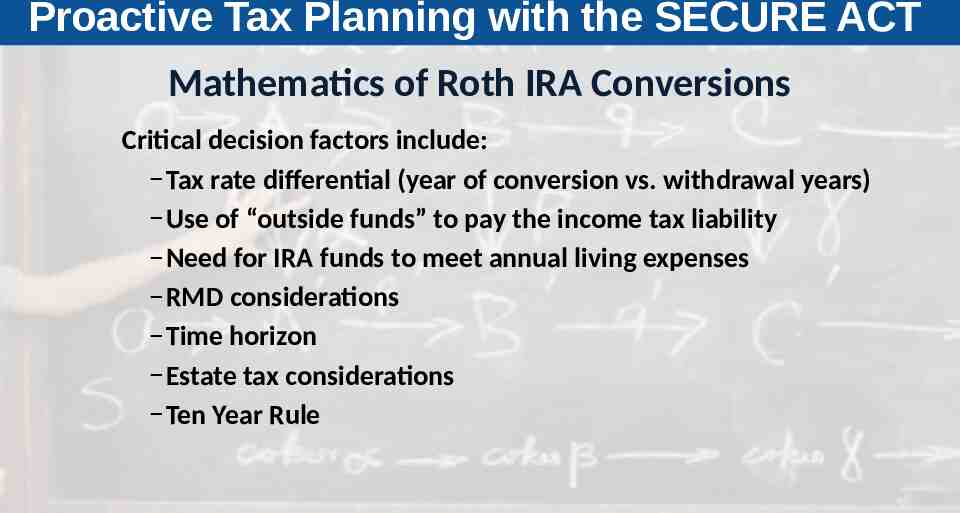

Proactive Tax Planning with the SECURE ACT Mathematics of Roth IRA Conversions Critical decision factors include: – Tax rate differential (year of conversion vs. withdrawal years) – Use of “outside funds” to pay the income tax liability – Need for IRA funds to meet annual living expenses – RMD considerations – Time horizon – Estate tax considerations – Ten Year Rule

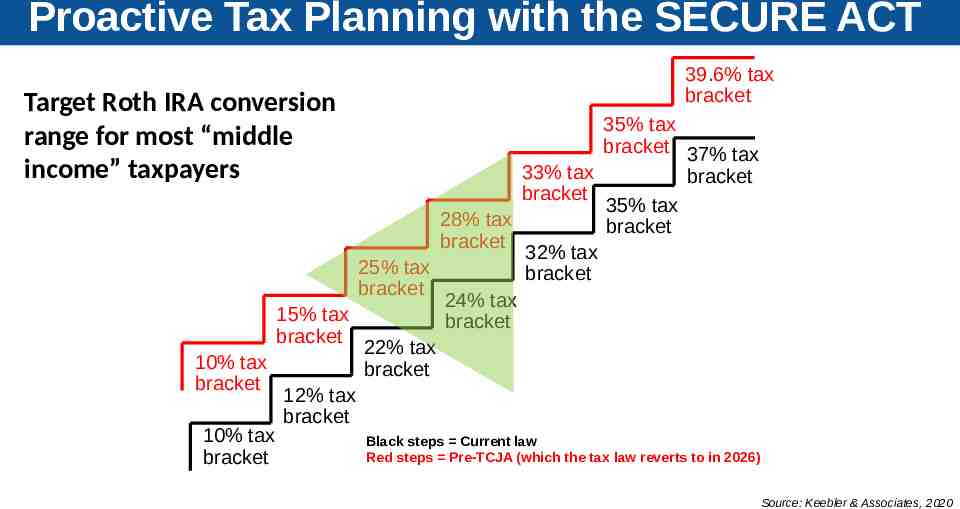

Proactive Tax Planning with the SECURE ACT Target Roth IRA conversion range for most “middle income” taxpayers 39.6% tax bracket 35% tax bracket 37% tax 33% tax bracket bracket 35% tax 28% tax bracket bracket 32% tax 25% tax bracket bracket 24% tax 15% tax bracket bracket 22% tax 10% tax bracket bracket 12% tax bracket 10% tax Black steps Current law Red steps Pre-TCJA (which the tax law reverts to in 2026) bracket Source: Keebler & Associates, 2020

Proactive Tax Planning with the SECURE ACT Some other reasons to consider Roth conversions, if appropriate include Tax brackets could rise Account values might be down Please check with your tax advisor before converting to a Roth IRA. Roth Conversions involve complicated rules. Traditional IRA account owners should consider the tax ramifications, age and income restrictions in regard to executing a conversion from a Traditional IRA to a Roth IRA. The converted amount is generally subject to income taxation.

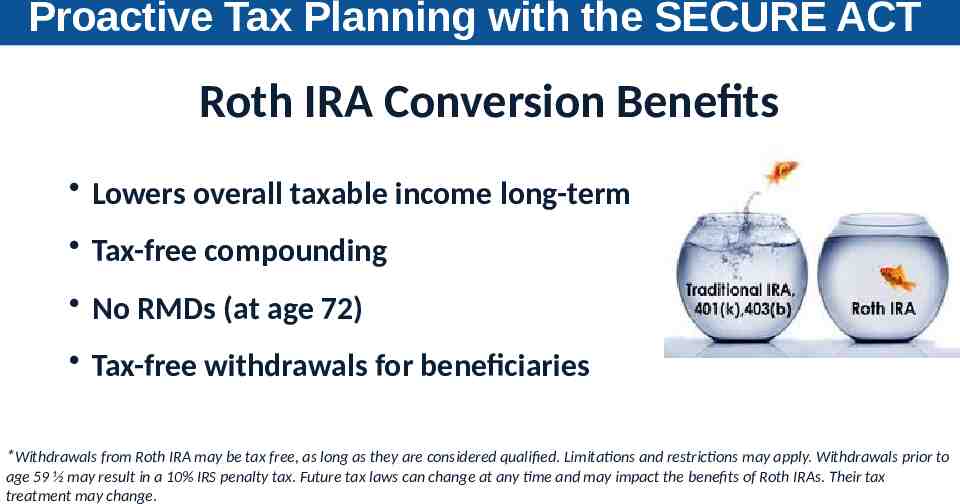

Proactive Tax Planning with the SECURE ACT Roth IRA Conversion Benefits Lowers overall taxable income long-term Tax-free compounding No RMDs (at age 72) Tax-free withdrawals for beneficiaries *Withdrawals from Roth IRA may be tax free, as long as they are considered qualified. Limitations and restrictions may apply. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax. Future tax laws can change at any time and may impact the benefits of Roth IRAs. Their tax treatment may change.

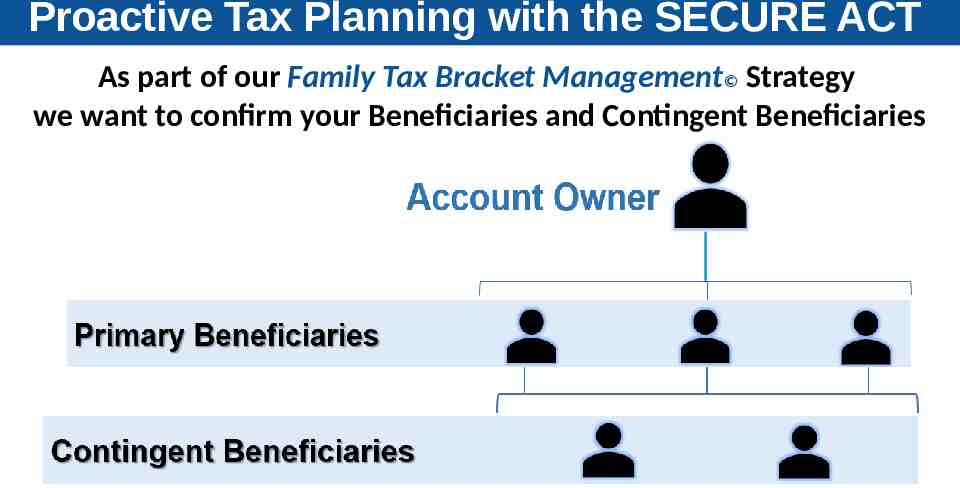

Proactive Tax Planning with the SECURE ACT As part of our Family Tax Bracket Management Strategy we want to confirm your Beneficiaries and Contingent Beneficiaries

Proactive Tax Planning with the SECURE ACT We can coordinate this with your tax preparer.

Key Takeaways The Secure Act changed retirement. Your situation and the 10-year rule should be reviewed. Our goal is to help clients understand their choices. Your health is our highest priority! Focus on your personal goals and call us with any concerns.

What Can You Expect From Us? Regular communication More frequent discussions Review of economic, tax, estate and investment issues for our clients

Thank You! Your health and well-being is our highest priority! We appreciate the opportunity to assist with YOUR financial needs!

Help Us Help Others! ! e r a h s e s a Ple

The views expressed are not necessarily the opinion of (Insert Broker-dealer name). Information is based on sources believed to be reliable, however, their accuracy or completeness cannot be guaranteed. This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice and should not be construed as a recommendation or solicitation to buy or sell any security. Please note that statements made in this presentation may be subject to change depending on any revisions to the tax code or any additional changes in government policy. Please note that individual situations can vary. Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax. Unless certain criteria are met, Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted. Additionally, each converted amount may be subject to its own five-year holding period. Converting a traditional IRA into a Roth IRA has tax implications. Investors should consult a tax advisor before deciding to do a conversion. rebalancing a non-retirement account could be a taxable event that may increase your tax liability. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material may contain forward looking statements and projections. There are no guarantees that these results will be achieved. Contents provided by: The Academy of Preferred Financial Advisors, Inc. 2021. All rights reserved. Insert Approved BD Disclaimer here Insert registered branch address, contact information