MCS AND RELATED DOCUMENTS UPDATES 2021/2022 1

10 Slides954.20 KB

MCS AND RELATED DOCUMENTS UPDATES 2021/2022 1

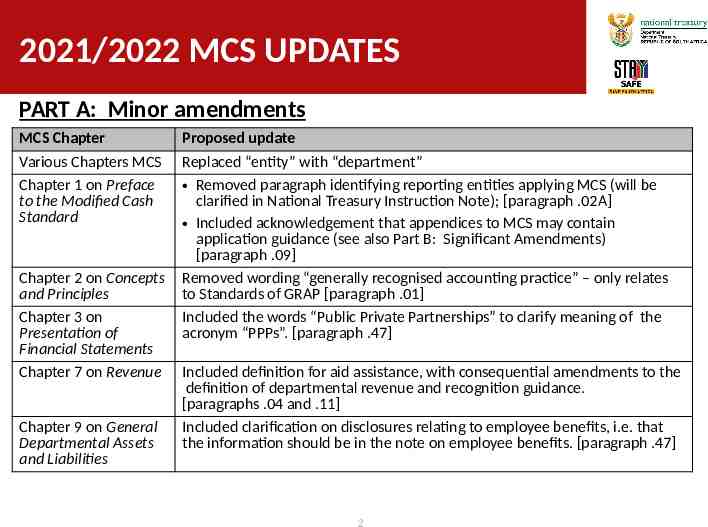

2021/2022 MCS UPDATES PART A: Minor amendments MCS Chapter Various Chapters MCS Chapter 1 on Preface to the Modified Cash Standard Chapter 2 on Concepts and Principles Chapter 3 on Presentation of Financial Statements Chapter 7 on Revenue Chapter 9 on General Departmental Assets and Liabilities Proposed update Replaced “entity” with “department” Removed paragraph identifying reporting entities applying MCS (will be clarified in National Treasury Instruction Note); [paragraph .02A] Included acknowledgement that appendices to MCS may contain application guidance (see also Part B: Significant Amendments) [paragraph .09] Removed wording “generally recognised accounting practice” – only relates to Standards of GRAP [paragraph .01] Included the words “Public Private Partnerships” to clarify meaning of the acronym “PPPs”. [paragraph .47] Included definition for aid assistance, with consequential amendments to the definition of departmental revenue and recognition guidance. [paragraphs .04 and .11] Included clarification on disclosures relating to employee benefits, i.e. that the information should be in the note on employee benefits. [paragraph .47] 2

2021/2022 MCS UPDATES PART A: Minor amendments MCS/AMD Chapter Chapter 11 on Capital Assets Chapter 13 on Leases Chapter 14 on Provisions and Contingents Chapter 16 on Accounting by Principals and Agents Chapter 19 on Transfers of Functions Chapter 20 on Mergers Proposed update Include reference to capital improvements in discussion on changes in value of capital assets; [paragraph .88] Included clarification on componentisation of assets; [paragraph .88] Replace “building” with “property”; a more general term; [paragraph .91] Included guidance on leasehold improvements; [paragraph .91] Correction of wording relating to the economic classification of leases; [paragraph .16] Similar update to Chapter 9, included clarification on disclosures relating to employee benefits, i.e. that the information should be in the note on employee benefits. [paragraph .48] Removed paragraph discussing disclosures during transitional period as transitional period has lapsed; [paragraph .69] Removed effective date paragraph as it is no longer necessary; [paragraph .46] Removed effective date paragraph as it is no longer necessary; [paragraph .47] 3

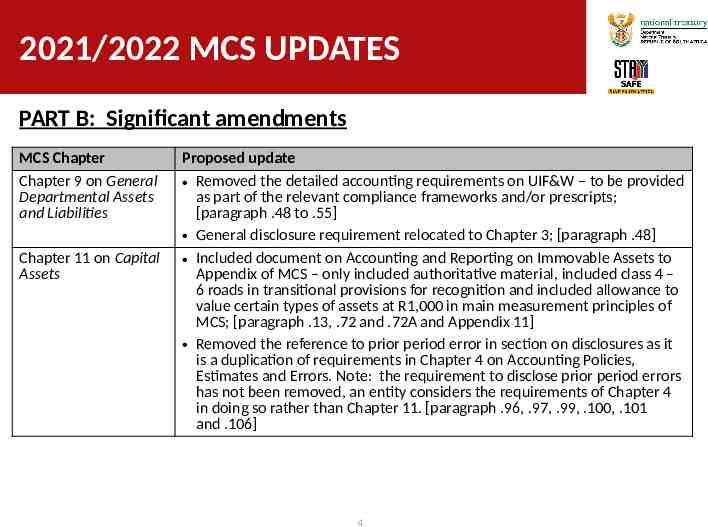

2021/2022 MCS UPDATES PART B: Significant amendments MCS Chapter Chapter 9 on General Departmental Assets and Liabilities Chapter 11 on Capital Assets Proposed update Removed the detailed accounting requirements on UIF&W – to be provided as part of the relevant compliance frameworks and/or prescripts; [paragraph .48 to .55] General disclosure requirement relocated to Chapter 3; [paragraph .48] Included document on Accounting and Reporting on Immovable Assets to Appendix of MCS – only included authoritative material, included class 4 – 6 roads in transitional provisions for recognition and included allowance to value certain types of assets at R1,000 in main measurement principles of MCS; [paragraph .13, .72 and .72A and Appendix 11] Removed the reference to prior period error in section on disclosures as it is a duplication of requirements in Chapter 4 on Accounting Policies, Estimates and Errors. Note: the requirement to disclose prior period errors has not been removed, an entity considers the requirements of Chapter 4 in doing so rather than Chapter 11. [paragraph .96, .97, .99, .100, .101 and .106] 4

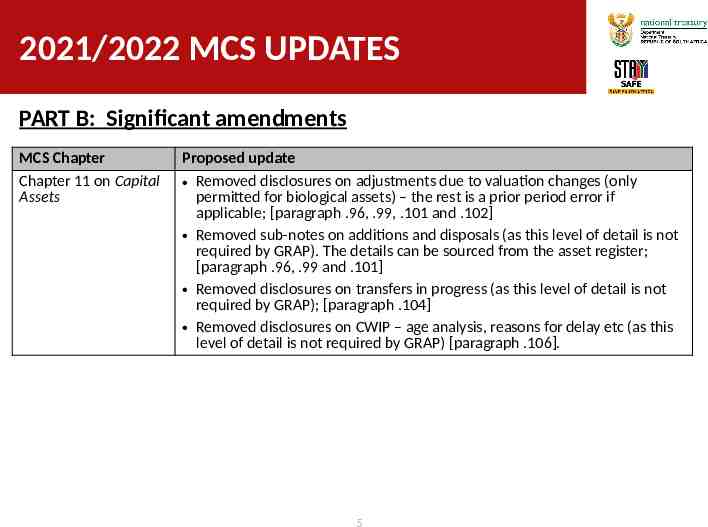

2021/2022 MCS UPDATES PART B: Significant amendments MCS Chapter Chapter 11 on Capital Assets Proposed update Removed disclosures on adjustments due to valuation changes (only permitted for biological assets) – the rest is a prior period error if applicable; [paragraph .96, .99, .101 and .102] Removed sub-notes on additions and disposals (as this level of detail is not required by GRAP). The details can be sourced from the asset register; [paragraph .96, .99 and .101] Removed disclosures on transfers in progress (as this level of detail is not required by GRAP); [paragraph .104] Removed disclosures on CWIP – age analysis, reasons for delay etc (as this level of detail is not required by GRAP) [paragraph .106]. 5

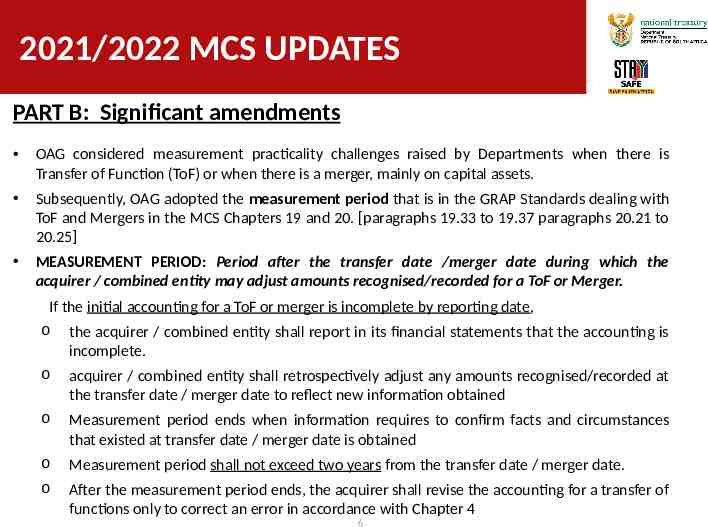

2021/2022 MCS UPDATES PART B: Significant amendments OAG considered measurement practicality challenges raised by Departments when there is Transfer of Function (ToF) or when there is a merger, mainly on capital assets. Subsequently, OAG adopted the measurement period that is in the GRAP Standards dealing with ToF and Mergers in the MCS Chapters 19 and 20. [paragraphs 19.33 to 19.37 paragraphs 20.21 to 20.25] MEASUREMENT PERIOD: Period after the transfer date /merger date during which the acquirer / combined entity may adjust amounts recognised/recorded for a ToF or Merger. If the initial accounting for a ToF or merger is incomplete by reporting date, o the acquirer / combined entity shall report in its financial statements that the accounting is incomplete. o acquirer / combined entity shall retrospectively adjust any amounts recognised/recorded at the transfer date / merger date to reflect new information obtained o Measurement period ends when information requires to confirm facts and circumstances that existed at transfer date / merger date is obtained o Measurement period shall not exceed two years from the transfer date / merger date. o After the measurement period ends, the acquirer shall revise the accounting for a transfer of functions only to correct an error in accordance with Chapter 4 6

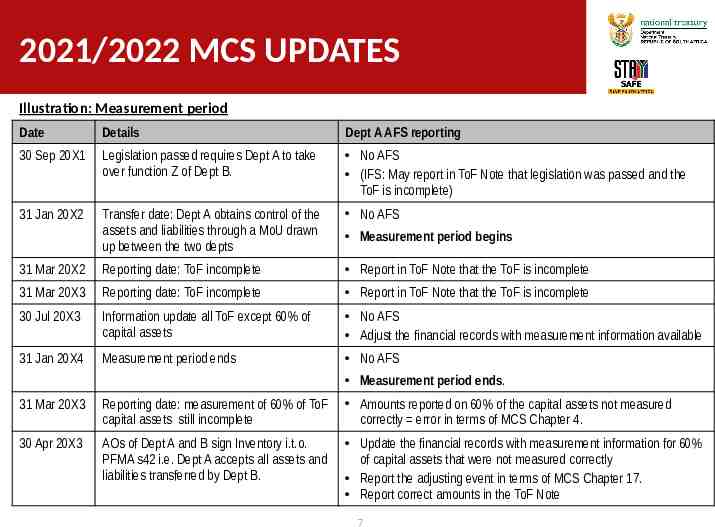

2021/2022 MCS UPDATES Illustration: Measurement period Date Details Dept A AFS reporting 30 Sep 20X1 Legislation passed requires Dept A to take over function Z of Dept B. No AFS (IFS: May report in ToF Note that legislation was passed and the ToF is incomplete) 31 Jan 20X2 Transfer date: Dept A obtains control of the assets and liabilities through a MoU drawn up between the two depts No AFS 31 Mar 20X2 Reporting date: ToF incomplete Report in ToF Note that the ToF is incomplete 31 Mar 20X3 Reporting date: ToF incomplete Report in ToF Note that the ToF is incomplete 30 Jul 20X3 Information update all ToF except 60% of capital assets No AFS Adjust the financial records with measurement information available 31 Jan 20X4 Measurement period ends No AFS Measurement period begins Measurement period ends. 31 Mar 20X3 Reporting date: measurement of 60% of ToF capital assets still incomplete Amounts reported on 60% of the capital assets not measured correctly error in terms of MCS Chapter 4. 30 Apr 20X3 AOs of Dept A and B sign Inventory i.t.o. PFMA s42 i.e. Dept A accepts all assets and liabilities transferred by Dept B. Update the financial records with measurement information for 60% of capital assets that were not measured correctly Report the adjusting event in terms of MCS Chapter 17. Report correct amounts in the ToF Note 7

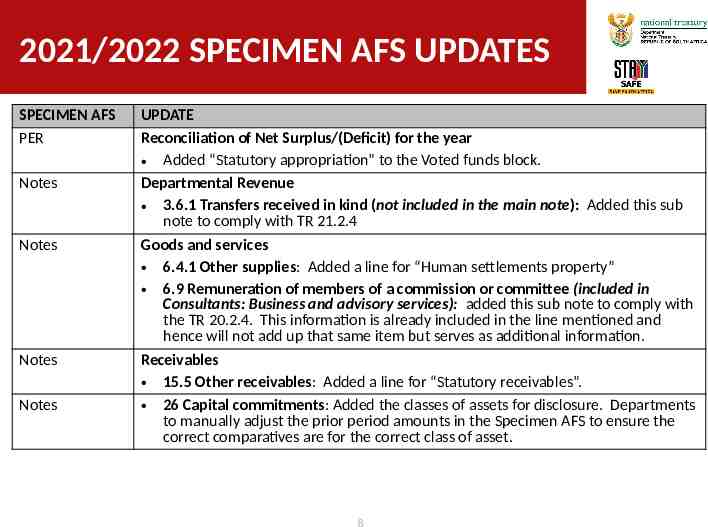

2021/2022 SPECIMEN AFS UPDATES SPECIMEN AFS PER Notes Notes Notes Notes UPDATE Reconciliation of Net Surplus/(Deficit) for the year Added “Statutory appropriation” to the Voted funds block. Departmental Revenue 3.6.1 Transfers received in kind (not included in the main note): Added this sub note to comply with TR 21.2.4 Goods and services 6.4.1 Other supplies: Added a line for “Human settlements property” 6.9 Remuneration of members of a commission or committee (included in Consultants: Business and advisory services): added this sub note to comply with the TR 20.2.4. This information is already included in the line mentioned and hence will not add up that same item but serves as additional information. Receivables 15.5 Other receivables: Added a line for “Statutory receivables”. 26 Capital commitments: Added the classes of assets for disclosure. Departments to manually adjust the prior period amounts in the Specimen AFS to ensure the correct comparatives are for the correct class of asset. 8

2021/2022 SPECIMEN AFS UPDATES SPECIMEN AFS Notes Notes UPDATE Capital assets notes Adjustments made in accordance with the changes to the MCS. Note 39 Movable tangible capital assets: greyed out all asset categories other than biological assets for the Value adjustments column, deleted sub notes 39.1 Additions, 39.2 Disposals, 39.7 S42 Movable capital assets. Note 40 Intangible capital assets: deleted a column in the main note 40 for Value adjustments, deleted sub notes 40.1 Additions, 40.2 Disposals Note 41 Immovable tangible capital assets: deleted a column in the main note 41 for Value adjustments, deleted sub notes 41.1 Additions, 41.2 Disposals, deleted the age analysis in sub note 41.4 Capital work-in-progress, deleted sub note 41.6 S42 Movable capital assets. Transfer of functions 46.1.2 Notes: Where the accounting for the transfer of functions is incomplete, the added narrative block per MCS Chapter on Transfer of functions paragraph .47 should be completed. Mergers 46.2.2 Notes: Where the accounting for the merger is incomplete, the added narrative block per MCS Chapter on Mergers paragraph .39 should be completed. 9

2021/2022 SPECIMEN AFS UPDATES SPECIMEN AFS UPDATE Annexures Annexure 10: Department of Human Settlements Housing Related Expenditure Classification Capital commitments: Added the classes of assets. 10