INTERNATIONAL FISCAL ASSOCIATION (IFA) EASTERN REGION CHAPTER

51 Slides1.43 MB

INTERNATIONAL FISCAL ASSOCIATION (IFA) EASTERN REGION CHAPTER Recent Developments in Transfer Pricing T. P. OSTWAL T P OSTWAL & ASSOCIATES July 2015 1

TRANSFER PRICING LITIGATION SCENARIO T P OSTWAL & ASSOCIATES July 2015 2

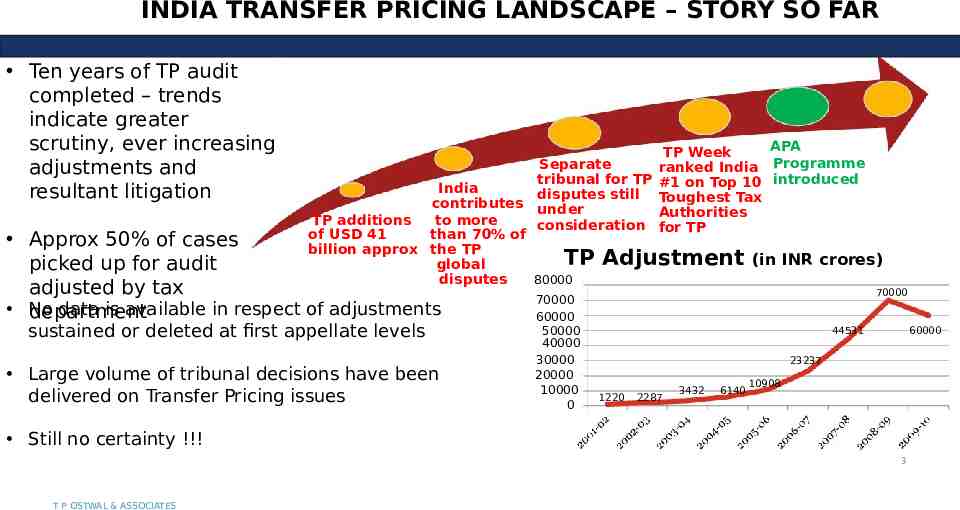

INDIA TRANSFER PRICING LANDSCAPE – STORY SO FAR Ten years of TP audit completed – trends indicate greater scrutiny, ever increasing adjustments and resultant litigation APA TP Week Separate ranked India Programme tribunal for TP #1 on Top 10 introduced India disputes still Toughest Tax contributes under Authorities TP additions to more consideration for TP of USD 41 than 70% of billion approx the TP TP Adjustment (in INR crores) global disputes 80000 Approx 50% of cases picked up for audit adjusted by tax No data is available in respect of adjustments department sustained or deleted at first appellate levels Large volume of tribunal decisions have been delivered on Transfer Pricing issues 70000 60000 50000 40000 30000 20000 10000 0 70000 44531 60000 23237 1220 2287 3432 6140 10908 Still no certainty !!! 3 T P OSTWAL & ASSOCIATES

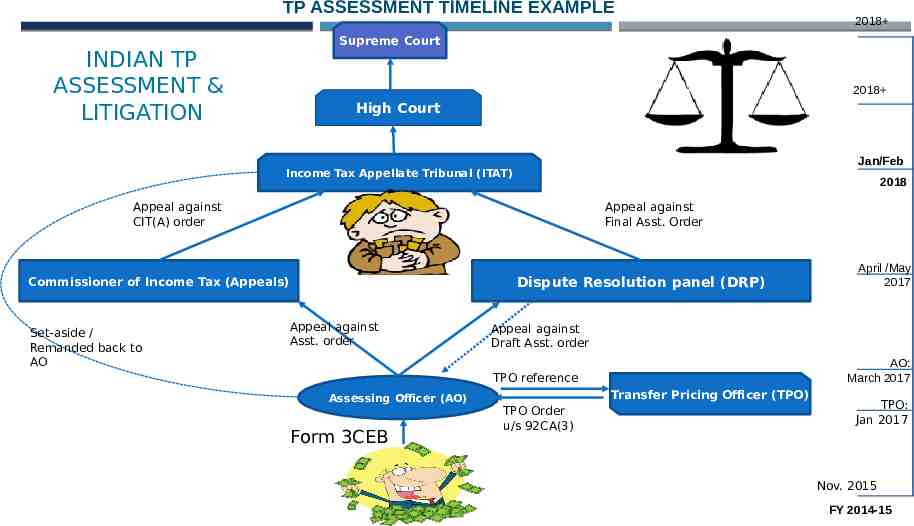

TP ASSESSMENT TIMELINE EXAMPLE Supreme Court INDIAN TP ASSESSMENT & LITIGATION 2018 High Court Jan/Feb Income Tax Appellate Tribunal (ITAT) 2018 Appeal against CIT(A) order Appeal against Final Asst. Order Dispute Resolution panel (DRP) Commissioner of Income Tax (Appeals) Set-aside / Remanded back to AO 2018 Appeal against Asst. order Appeal against Draft Asst. order AO: March 2017 TPO reference Assessing Officer (AO) Form 3CEB April /May 2017 Transfer Pricing Officer (TPO) TPO Order u/s 92CA(3) TPO: Jan 2017 Nov. 2015 FY 2014-15

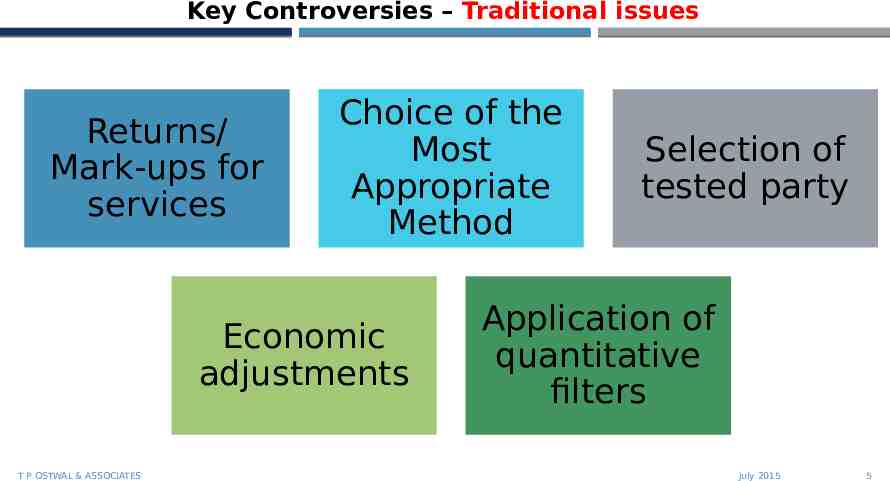

Key Controversies – Traditional issues Returns/ Mark-ups for services Choice of the Most Appropriate Method Economic adjustments T P OSTWAL & ASSOCIATES Selection of tested party Application of quantitative filters July 2015 5

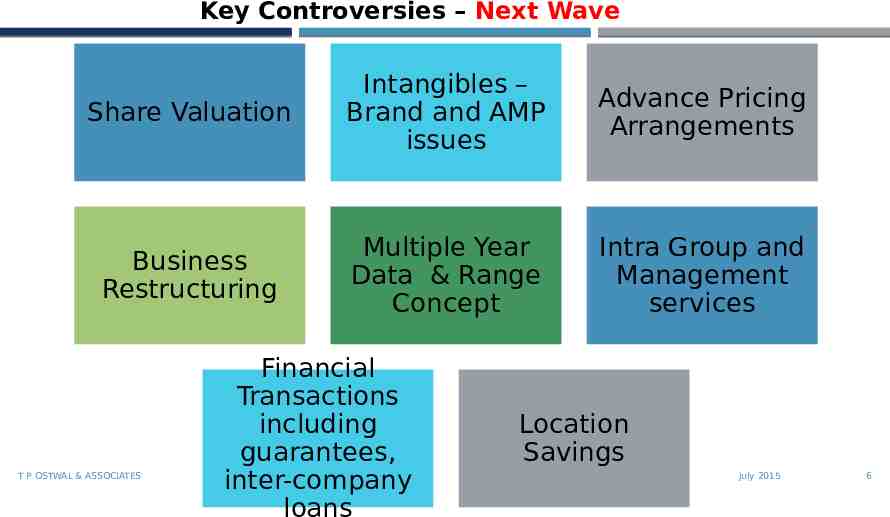

Key Controversies – Next Wave Share Valuation Intangibles – Brand and AMP issues Advance Pricing Arrangements Business Restructuring Multiple Year Data & Range Concept Intra Group and Management services T P OSTWAL & ASSOCIATES Financial Transactions including guarantees, inter-company loans Location Savings July 2015 6

VALUATION OF SHARES T P OSTWAL & ASSOCIATES July 2015 7

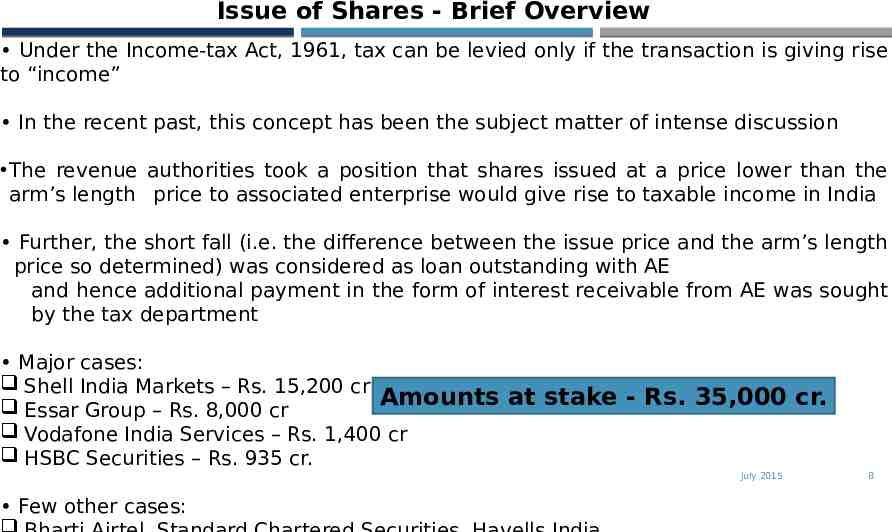

Issue of Shares - Brief Overview Under the Income-tax Act, 1961, tax can be levied only if the transaction is giving rise to “income” In the recent past, this concept has been the subject matter of intense discussion The revenue authorities took a position that shares issued at a price lower than the arm’s length price to associated enterprise would give rise to taxable income in India Further, the short fall (i.e. the difference between the issue price and the arm’s length price so determined) was considered as loan outstanding with AE and hence additional payment in the form of interest receivable from AE was sought by the tax department Major cases: Shell India Markets – Rs. 15,200 cr Amounts at stake - Rs. 35,000 cr. Essar Group – Rs. 8,000 cr Vodafone India Services – Rs. 1,400 cr HSBC Securities – Rs. 935 cr. July 2015 Few other cases: 8

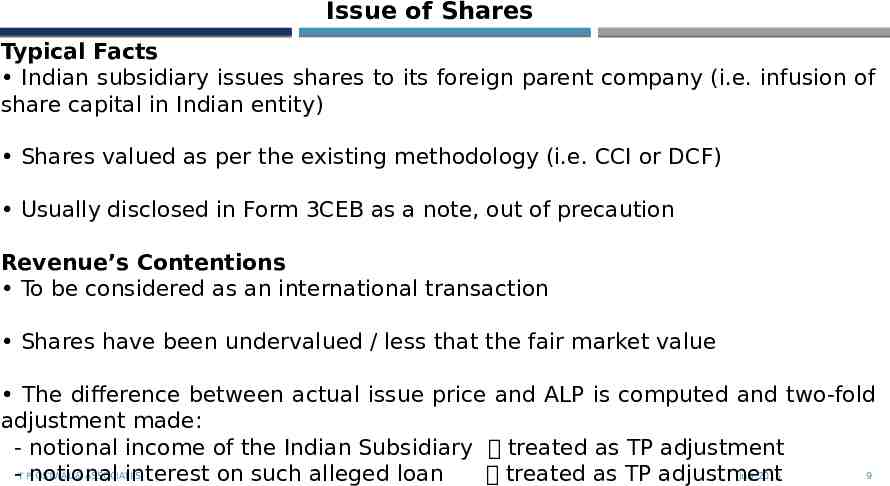

Issue of Shares Typical Facts Indian subsidiary issues shares to its foreign parent company (i.e. infusion of share capital in Indian entity) Shares valued as per the existing methodology (i.e. CCI or DCF) Usually disclosed in Form 3CEB as a note, out of precaution Revenue’s Contentions To be considered as an international transaction Shares have been undervalued / less that the fair market value The difference between actual issue price and ALP is computed and two-fold adjustment made: - notional income of the Indian Subsidiary treated as TP adjustment OSTWAL & ASSOCIATES July 2015 9 -T Pnotional interest on such alleged loan treated as TP adjustment

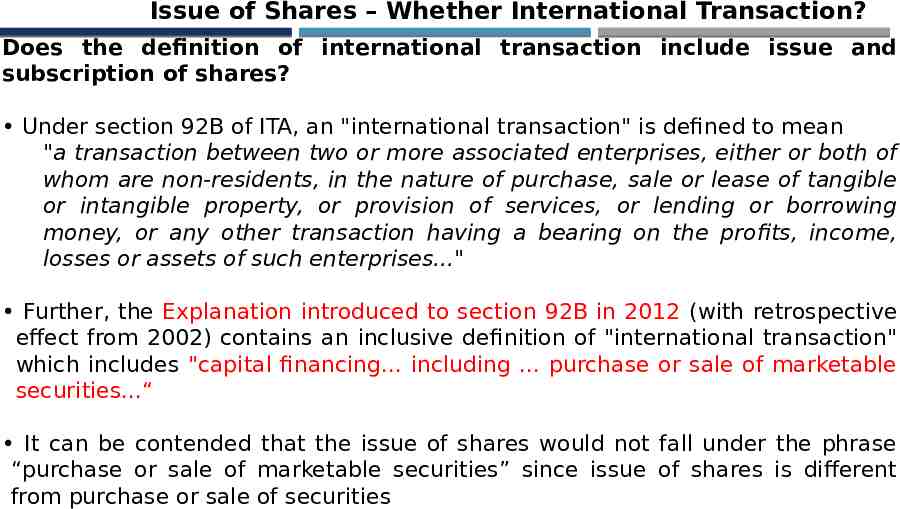

Issue of Shares – Whether International Transaction? Does the definition of international transaction include issue and subscription of shares? Under section 92B of ITA, an "international transaction" is defined to mean "a transaction between two or more associated enterprises, either or both of whom are non-residents, in the nature of purchase, sale or lease of tangible or intangible property, or provision of services, or lending or borrowing money, or any other transaction having a bearing on the profits, income, losses or assets of such enterprises." Further, the Explanation introduced to section 92B in 2012 (with retrospective effect from 2002) contains an inclusive definition of "international transaction" which includes "capital financing. including . purchase or sale of marketable securities.“ It can be contended that the issue of shares would not fall under the phrase “purchase or sale of marketable securities” since issue of shares is different from purchase or sale of securities

Issue of Shares – Whether International Transaction? (contd) The crucial question is whether Chapter X of ITA confers the jurisdiction to treat a transaction on the capital account as a revenue transaction? treat a single transaction of issue of shares as two transactions as that of issue of shares and of grant of a financial accommodation (equal to the difference in value of the arm's length price determined and the issue price of shares) to bring to tax a notional amount as interest foregone on this notional amount of financial accommodation? T P OSTWAL & ASSOCIATES July 2015 11

Other Issues for consideration Whether the difference in the share price (‘alleged undervaluation’) can be considered as an “income” under ITA? How to value equity shares? Valuation methodology to be adopted Whether TPO correct in treating the difference in valuation of shares treated as deemed loan / deemed receivable ? Whether imputing a notional interest on deemed loan is correct? Whether outbound investment attract transfer pricing? What is the method of computation of arm’s length price? [Refer Top Securities Case] Does issue of new shares attract transfer pricing? Whether share application money on outbound investment attract transfer T P OSTWAL & ASSOCIATES July 2015 12 pricing?

Vodafone India – Bombay High Court Facts Vodafone India is a wholly owned subsidiary of a Mauritius Vodafone entity, issued equity shares of face value of Rs. 10 at a premium of Rs. 8,591 per share to its holding company TPO / DRP TPO disputed the valuation of shares and re-computed the value per share [based on the Net Asset Value (NAV) to Rs. 53,775. TPO treated the shortfall in the value of shares [Rs.53,775 less Rs. 8,591 per share] as deemed loan by the taxpayer to its foreign parent and charged a notional interest @ 13.5% and accordingly made TP adjustment. DRP also upheld the TP order T P OSTWAL & ASSOCIATES July 2015 13

Vodafone India – Bombay High Court High Court Ruling TP regulations are applicable only to international transactions that give rise to taxable income. Neither the capital receipt on issue of equity shares nor the shortfall (if any) in share premium can be considered as taxable income within the ambit of ITA Further, there is no specific provision in ITA for treating inflow of funds from shares issued to non-residents as taxable income. Hence, TP provisions do not apply to capital transaction itself T P OSTWAL & ASSOCIATES July 2015 14

Vodafone India – Bombay High Court Update Attorney General advised Government not to file Special Leave Petition CBDT instruction No.2/2015 dated 29 January 2015: Board accepted decision of HC, field officers directed to adhere Press release by Ministry of Finance: “bring greater clarity and predictability” and thereby improve the investment climate in the country T P OSTWAL & ASSOCIATES July 2015 15

ADVERTISING, MARKETING AND PROMOTION EXPENSES T P OSTWAL & ASSOCIATES July 2015 16

Marketing Intangibles Meaning of “Marketing Intangibles” Ordinarily includes a bundle of IP rights such as: Trade names, trademarks, knowhow on distribution channels and customer relationships Nebulous & unclear Varies in application by jurisdiction & industry Breadth continues to grow as tax authorities use it Main investment in marketing intangibles is through AMP spend

Key Issues on AMP Globally Benefit to Foreign AE: How will AE benefit from residual AMP cost (and resulting intangible) for which it is required to bear the cost of development? Economic vs. Legal Ownership: If legal ownership of intangible is more important than economic ownership, and brand name is legally owned by AE, then Indian sub should pay a healthy non-zero royalty for its use. Entrepreneur vs. Limited Risk Entity: Impact of Indian sub being a low-risk entity vis-à-vis an entrepreneur on how the costs should be handled. T P OSTWAL & ASSOCIATES July 2015 18

Special Bench Decision of Delhi Tax Tribunal on AMP There is a valid transaction in the form of excessive AMP expense incurred by Indian company (“ICo”) sub-enhancing the foreign brand, legally owned by the foreign associated enterprise (“AE”) Amount of the transaction calculated by applying Bright Line Test (“BLT”) Bright line test refers to the testing the AMP expenditure incurred by the taxpayer in proportion to its sales (AMP/sales) with the average AMP/sales of the comparables to determine the routine and non routine AMP expenses incurred by the taxpayer. Based on BLT, ICo’s AMP costs bifurcated towards: assisting local product sales enhancing global brand value ICo to be compensated by AE for amounts incurred towards “enhancing brand value” along with a markup T P OSTWAL & ASSOCIATES July 2015 19

Delhi High Court on AMP - Summary TP adjustment on account of AMP expenditure incurred by Indian entities as part of distribution business in India like Canon India, Reebok India, Sony India Pvt. Ltd and others. AMP expenditure does not presuppose contribution to brand building by the Indian entity for its overseas AE. Brand value is created by synergetic impact of reputation, quality and other facts relevant to a particular business and not just by incurring AMP expense. HC rejected the application of Bright line test for determining non-routine AMP expense and TP adjustment on account of separate consideration for such alleged non routine AMP expense incurred by the taxpayers. T P OSTWAL & ASSOCIATES July 2015 20

Delhi High Court on AMP – Facts The taxpayers are Indian subsidiaries of MNEs engaged in importing, marketing and distribution of branded products manufactured by its AEs Intangible rights in the brand name are owned by AEs. The taxpayers substantiate the arm’s length nature of their transaction with AEs relating to import of goods for resale in India using TNMM (in case of Sony and Reebok India) and RPM in case of Canon India; CUP method was used in Reebok India’s case to benchmark the royalty payment. The TPO in all the above cases, in line with the Special Bench (SB) ruling in case of LG Electronics applied the ‘Bright line test’ to determine the excess/ non- routine AMP expenditure incurred by the taxpayer for building brand for its AEs in India. T P OSTWAL & ASSOCIATES July 2015 21

Delhi High Court on AMP – Facts The TPO proposed a Transfer Pricing adjustment that the taxpayer should be separately remunerated for building brand by the taxpayer in India for its AEs at cost plus mark- up basis The Dispute Resolution Panel (DRP) upheld the order of the TPO. The ITAT provided limited relief to the taxpayers in line with the SB ruling in the LG case Aggrieved by the ITAT order, both the Revenue and taxpayers filed appeals before the HC to decide on the substantial questions of Law. T P OSTWAL & ASSOCIATES July 2015 22

Delhi High Court on AMP – Ruling Jurisdiction of the TPO Retrospective amendment u/s 92CA(2B) of the Act giving the TPO power to determine the arm’s length nature of a transaction (that he may come across during the assessment proceedings), even if such transaction has not specifically been referred by the AO to the TPO. AMP - an international transaction Upheld the views of the SB in LG case and held that AMP expenditure would amount to an international transaction. Taxpayers themselves made an argument that the declared price of international transactions in Form 3CEB included a remuneration for their AMP function, the argument challenging it as not an international transaction is incorrect. OSTWAL & ASSOCIATES July 2015 T PRejected the contention of the taxpayers that AMP expenses incurred by the23 taxpayer is not an international transaction as these expenses are third party

Delhi High Court on AMP – Ruling Bundled/ Inter-connected Transaction Taxpayers could aggregate the controlled transactions if the transactions are closely linked and as such cannot be evaluated adequately on separate basis. The HC further held that once the TPO accepts TNMM as the most appropriate method for determining arm’s length price of bundled transactions, then it is impermissible to separately determine the arm’s length price of a particular expenditure like AMP, since, such expense is already factored in the net profit of the interlinked transactions. Brand and Brand Building The HC observed that brand building is an outcome of various factors and is largely associated with the reputation and quality of the product or service. There are situations where brands are built without incurring any substantial AMP and vice versa. Therefore, brand building cannot be commensurate with the quantum of AMP

Delhi High Court on AMP – Ruling Bright Line Test The HC held that universal application of bright line test to segregate AMP into routine and non routine AMP is unwarranted. Further, the HC also held that such application of bright line test would amount to adding provisions to the statute and rules, which are non-existent. Such approach is not permissible, especially in the absence of any statutory recognition or any international practice in this regard. Cost plus method for separate remuneration for AMP expenses The HC held that once AMP expense has been included as part of bundled transaction, it cannot be separately benchmarked under Cost plus method.

Delhi High Court on AMP – Ruling Determination of arm’s length price When the Indian entity carrying on distribution activity incurs AMP expenditure, the arm’s length analysis is required to ascertain whether Indian entity has been adequately and properly compensated for incurring such expenditure. The HC emphasised the importance of a systematic transfer pricing analysis for arriving at the arm’s length price by selection of most appropriate methods and appropriate comparables in line with the functions, assets and risks of the tested party. Where the margin of the taxpayer is in line with comparables carrying similar functions of the taxpayer including AMP function, no separate TP adjustment is warranted

ADVANCE PRICING ARRANGEMENTS (APA) T P OSTWAL & ASSOCIATES July 2015 27

INTRODUCTION TO APA. An APA is a contract Usually for multiple years Between a taxpayer and at least one tax authority Mainly to prospectively resolve real or potential transfer pricing issues Involving transactions between related parties

INTRODUCTION TO APA . t en em e r Ag Once APA has been entered into, the ALP will be determined only in accordance with the APA The APA process is voluntary Supplements appeal and other resolving transfer pricing disputes DTAA mechanism for Provides greater certainty on the transfer pricing method adopted Mitigates the possibility of disputes Facilitates the financial reporting of potential tax liabilities Reduces the incidence of double taxation, and the costs associated with both audit defense and documentation preparation

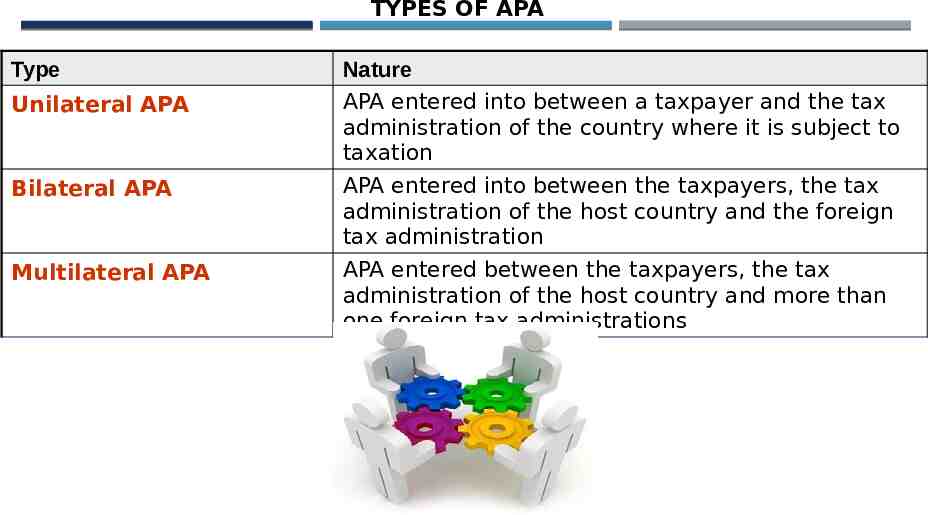

TYPES OF APA Type Unilateral APA Bilateral APA Multilateral APA Nature APA entered into between a taxpayer and the tax administration of the country where it is subject to taxation APA entered into between the taxpayers, the tax administration of the host country and the foreign tax administration APA entered between the taxpayers, the tax administration of the host country and more than one foreign tax administrations

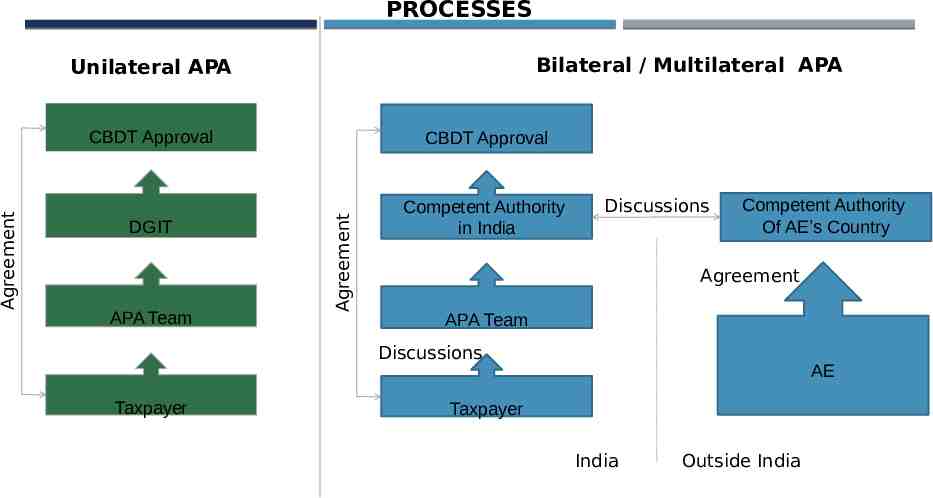

PROCESSES Bilateral / Multilateral APA CBDT Approval CBDT Approval DGIT Competent Authority in India APA Team Agreement Agreement Unilateral APA Discussions Competent Authority Of AE’s Country Agreement APA Team Discussions Taxpayer AE Taxpayer India Outside India

ADVANTAGES OF APA Provides certainty of tax treatment by relevant tax authority Investment decisions regarding overseas operations clarified: Projection of future tax liabilities possible Mitigates risk of a difficult potential TP audit/ future litigation Substantially reduces possibility of future double taxation (bilateral or multilateral APA) APAs have the potential to cover most TP issues including: - Tangible goods pricing. - Services - Intangibles issues involving royalties - Cost-sharing issues Taxpayer has participation in the process (unlike MAP) Slide 32

DISADVANTAGES OF APA Increases the risk of audits and adjustments in the related party country (in case of unilateral APA) Cost of implementation is high - However, it’s likely that APA costs audit defense fees - However, high cost involved in preparing APA application makes it economically justifiable only when there is large volume of transaction May reduce tax planning opportunities Immediately draws attention to an entity’s tax planning in different nations Usefulness of APA diminished if no agreement reached until period proposed to be covered almost expires Potential reluctance of taxpayers to disclose information unless confidentiality

EXAMPLE Indian subsidiary engaged in machinery distribution, had very high profits over a number of years Concern about exposure of foreign parent to adjustment by its tax authority Earlier assessment: both foreign parent tax authority and Indian TP authorities adjusted income, resulting in double taxation Goal: Obtain tax authority approval for resetting transfer prices Strategy: Obtain bilateral APA, adjust to closest point in the range (high end)

APA: INTERNATIONAL SCENARIO More than 30 Countries allow APA Almost 20 years ago, only a few countries (e.g. the United States, Canada and Australia) were frontrunners in the implementation of formal APA schemes Up to 2010, the United States had signed the highest number of APAs (over 950) in the world Following the introduction of the OECD guidelines on APAs in 1995, a number of countries began to enter into APA schemes The experiences of these countries (especially the Asian countries due to economic similarities) in the

APA: INTERNATIONAL SCENARIO Country Year of introduction Type of APA Term of agreement Pre-filing Japan 1987 Unilateral & Bilateral 3-5 years Optional USA 1991 Unilateral, Bilateral & Multilateral 3-5 years Mandatory UK 1999 Unilateral, Bilateral (No distinction in bi and multilateral 18 to 21 months Optional China 2004 Unilateral, Bilateral & Multilateral 3-5 years Mandatory India 2012 Unilateral, Bilateral & Multilateral Upto 5 years Mandatory

APA SCHEME IN INDIA The APA regime was initially slated to be a part of the Direct Taxes Code However, the APA scheme released with its introduction through the Union Budget 2012-13, and has been woven into the existing set of Regulations Introduced through sections 92CC and 92CD and Rules 10F to 10T The Indian tax department received 386 applications from MNCs in FY 2012-2013, FY 2013-14 & FY 2014-15 Of the 386, 329companies are seeking “unilateral APA” (pact between tax payer and CBDT). The rest applied for “bilateral APA” (pact between taxpayers, tax authorities of the host country and the foreign tax administration) CBDT signed 5 “unilateral APAs” making it one of the fastest turnarounds in transfer pricing history across the world Recently, India signed its first bilateral APA with a Japanese Company.

APA SCHEME IN INDIA At present, a parallel mechanism exists i.e. advance rulings from the Authority for Advance Rulings (AAR) AAR is empowered to examine a prospective contract of a resident taxpayer with a non-resident in order to determine the taxability thereof The main difference between AAR and APA: under the APA scheme, the tax authorities may determine/quantify the value of the international transaction or profits, whereas the Authority for Advance Rulings does not have a power to do so

SIGNIFICANT FEATURES OF THE APA FRAMEWORK IN INDIA The use of existing prescribed methodologies with necessary adjustments/variations or any other method to determine the arm's length price One may choose any method in addition to the methods prescribed in the Regulations This gives flexibility to agree upon a method that may be more suitable This also makes the APA regime more attractive to those MNEs that are dealing with difficult scenarios where the prescribed methods may not best reflect an arm’s length outcome

SIGNIFICANT FEATURES OF THE APA FRAMEWORK IN INDIA The duration (i.e. term) of an APA would be limited to a maximum of five consecutive fiscal years Coverage of five years is consistent with the coverage of APAs in other countries A period of three to five years is considered adequate as regards the cost of the APA process, expected changes to the business and various conditions affecting the transactions covered

SIGNIFICANT FEATURES OF THE APA FRAMEWORK IN INDIA APAs are binding on the taxpayer and the tax authorities unless there is a change in the law or facts of the case This will give certainty to both taxpayers and the tax authorities. However, care should be taken to ensure that minor changes in the course of business due to market dynamics do not render the APA void.

SIGNIFICANT FEATURES OF THE APA FRAMEWORK IN INDIA Approval of the Central Government will be necessary This suggests that the government intends to monitor and possibly even control the APA process Other than its obvious effects, this will ensure that the APA process is completed within a reasonable time frame

SIGNIFICANT FEATURES OF THE APA FRAMEWORK IN INDIA An APA applies to the determination of the arm's length price in respect of prospective transactions only even if the transaction is a continuing one The APA process is a forward-looking exercise and is applicable only with regard to prospective transactions that are either being contemplated to be undertaken or those which are continuing transactions that will be carried out in the following year by the taxpayer Further, as APA will involve the determination of the arm’s length price, a detailed transfer pricing audit by a transfer pricing officer will not be undertaken for the term of the agreement, however, the taxpayer will need to satisfy the transfer pricing officer as regards the compliance with the terms of the agreement, critical assumptions, correctness of the supporting data and consistency of the applications of the transfer pricing method

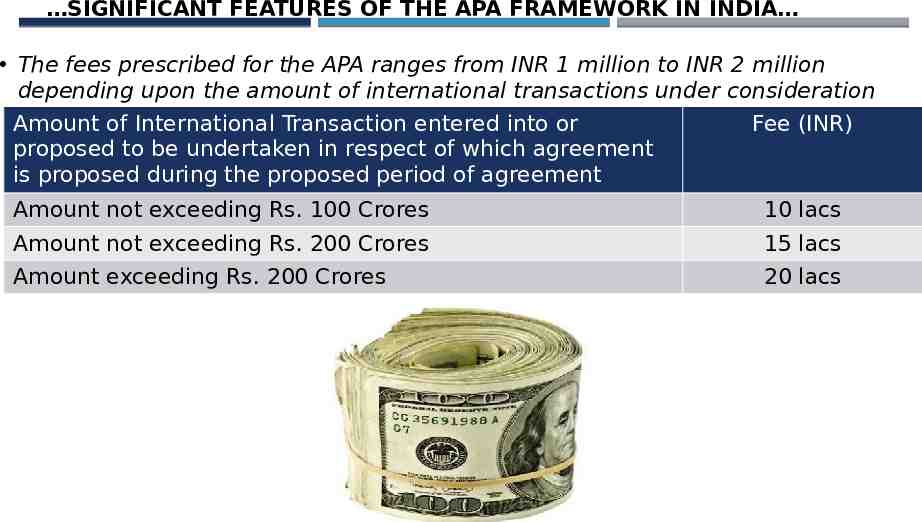

SIGNIFICANT FEATURES OF THE APA FRAMEWORK IN INDIA The fees prescribed for the APA ranges from INR 1 million to INR 2 million depending upon the amount of international transactions under consideration Amount of International Transaction entered into or Fee (INR) proposed to be undertaken in respect of which agreement is proposed during the proposed period of agreement Amount not exceeding Rs. 100 Crores 10 lacs Amount not exceeding Rs. 200 Crores 15 lacs Amount exceeding Rs. 200 Crores 20 lacs

SIGNIFICANT FEATURES OF THE APA FRAMEWORK IN INDIA APA shall not be binding if there is a change in law or facts relating to the agreement Void-ab-initio if agreement is obtained by fraud or misrepresentation of facts If ROI already filed, the same can be modified after APA is entered into Assessment if already completed , the officer should assess or reassess as per the APA

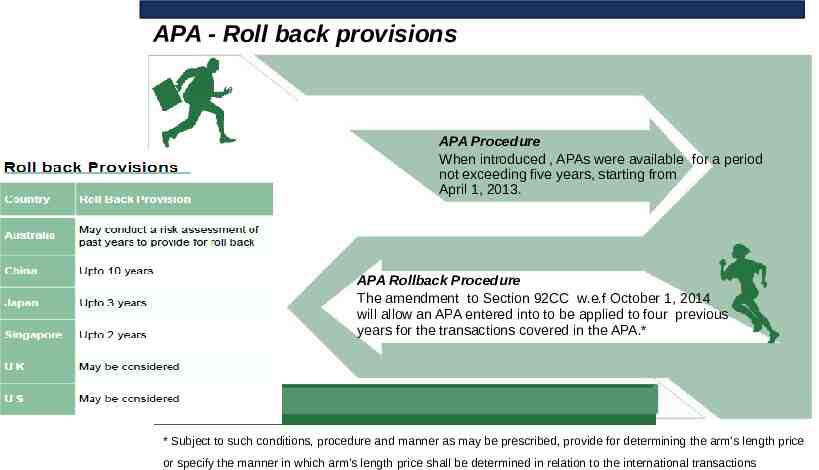

APA - Roll back provisions APA Procedure When introduced , APAs were available for a period not exceeding five years, starting from April 1, 2013. APA Rollback Procedure The amendment to Section 92CC w.e.f October 1, 2014 will allow an APA entered into to be applied to four previous years for the transactions covered in the APA.* * Subject to such conditions, procedure and manner as may be prescribed, provide for determining the arm’s length price or specify the manner in which arm’s length price shall be determined in relation to the international transactions

MULTIPLE YEAR DATA RANGE CONCEPT T P OSTWAL & ASSOCIATES July 2015 47

Draft rules for the range concept and multiple year data unveiled With the intention of aligning transfer pricing regulations in India with global best practices and reducing litigation considerably, Finance Minister, Arun Jaitley, in his Budget speech in July 2014, had announced the introduction of the ‘range concept’ for determining the arm's length price (ALP) and allowing the use of multiple year data for comparability analysis. Consequently, section 92C(2) of the Income Tax Act, 1961 (ITA) was amended to allow taxpayers to determine the ALP (where more than one price exists) in relation to international transactions or specified domestic transactions in the prescribed manner. On 21 May 2015, CBDT released a draft scheme of the proposed rules for computation of ALP The manner of computation of ALP is proposed to be provided through an amendment in the Income Tax Rules.

Draft rules for the range concept and multiple year unveiled Range data Concept The range concept would apply only where a minimum of nine companies are selected as comparable, and where inadequate comparable companies exist, the arithmetic mean concept would continue to apply. Weighted average of three years’ data of the comparables would be considered wherein all the numerators and denominators would be aggregated entity-wise for all the years and margins would be computed thereafter. Data points lying within the 40th and 60th percentile of the dataset would constitute the range. In case the transfer price of the tested party falls outside the range arrived at, the median of the range would be considered as the ALP. There would not be a separate tolerance band once the range is allowed. In cases where the range concept does not apply, arithmetic mean as applied

Draft rules for the range concept and multiple year data unveiled Multiple year data Multiple year data should comprise of three years' data including the year in which the transaction was undertaken. Use of two years' data out of three years for a comparable company is permitted if the data is not available on account of the following: data is not available on the database at the time of filing the return of income; a comparable fails to clear a quantitative filter in any of the years; and a comparable commenced operations only in the last two years or may have closed down operations during the current year. If data of the year in which the transaction is undertaken is available at the time of the transfer pricing audit by the department, it can be used by both the taxpayer and the department. The benefit of using multiple year data is now extended to cases where arithmetic mean is used to determine ALP.

THANK YOU T. P. Ostwal & Associates CHARTERED ACCOUNTANTS 4th Floor, Bharat House, 104 Mumbai Samachar Marg, Fort, MUMBAI-400001. Tel No.: 91-22-40693900 Fax No.: 91-22-40693999 Mobile: 91-9004660107 Email: [email protected] T P OSTWAL & ASSOCIATES July 2015 51