IB Economics What is Economics?

54 Slides1.05 MB

IB Economics What is Economics?

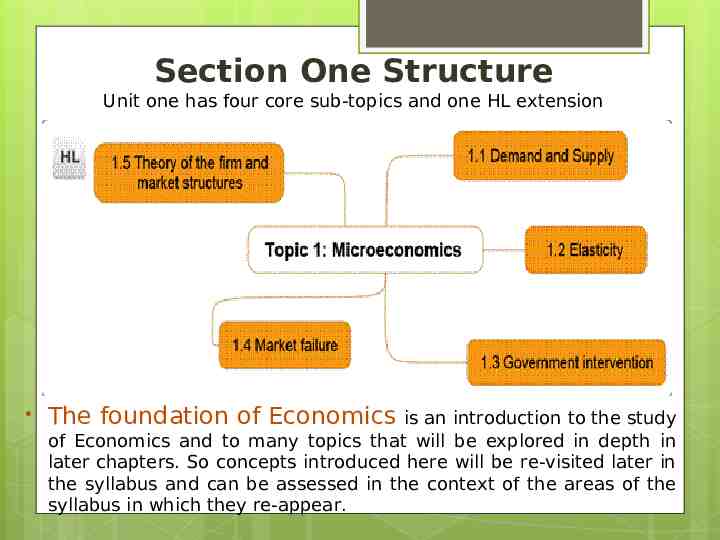

Section One Structure Unit one has four core sub-topics and one HL extension The foundation of Economics is an introduction to the study of Economics and to many topics that will be explored in depth in later chapters. So concepts introduced here will be re-visited later in the syllabus and can be assessed in the context of the areas of the syllabus in which they re-appear.

Economics is the study of Wealth Money Politics How to become rich? How to economize? CHOICES

Explain that scarcity exists because factors of production are finite while needs and wants are infinite Resources Needs and wants Human beings have unlimited needs and wants. The Earth has limited resources, which are inputs or factors of production (FOPs) used to produce GOODS and SERVICES that satisfy people’s needs and wants. The Result: People can’t have everything they want because there are not enough resources. The Solution: There must be a system to rationally use these scarce resources. (the field of Economics arises to provide this system)

Economics is The study of how scarce resources can be allocated in the best possible way among alternative uses to meet unlimited human needs and wants

Scarcity The scarcity issue arises whenever there is not enough of something in relation to the need for it To the economist, all goods and services that have a price are relatively scarce. Price is used to ration available goods Any good or service that has a price and is thus being rationed is an Economic Good

Explain that as a result of scarcity, CHOICES has to be made Choice The conflict between unlimited needs and wants and scarce resources has an important consequence, people can’t have everything they want and therefore must make CHOICES If For example, since people have limited financial resources, they need to make choices when they purchase goods and services. Therefore, they need to choose between alternatives. there were no resource scarcity, a choice would not be necessary. More of everything can always be produced and bought by human beings.

Explain the three basic economic questions that must be answered by an economic system. The Basic Economic Questions Scarcity forces every economy in the world to make choices through answering 3 basic questions: What to produce and in what quantities How to produce (Labor-intensive techniques vs. Capital-intensive techniques) For whom need) to produce (Affordability vs.

The Basic Economic Questions Resource allocation The first 2 questions deal with resource allocation, which is assigning available resources to specific uses choses among many possible alternatives. For example, if the answer to the what to produce question was 2 tons of food and 1 weapon; this means that resources will be allocated accordingly to produce this combination of output. If a decision was made to change the amount of food produced relative to weapons, such as more weapons and fewer food, this involves a reallocation of resources Sometimes, the economy produces a wrong amount of goods and services relative to what is socially desirable. For example, if too many weapons are being produced , we say that there is an overallocation of resources to the production of weapons. If too few tons of food are being produced relative to the population size, we say that there is an underallocation of resources to the food production.

The Basic Economic Questions Income distribution The third basic economic question involves the distribution of output/income among individuals in the economy. This could be based on financial ability or need and equity. when the distribution of income changes so that individuals receive more or less income than previously; this is referred to as redistribution of income,

Answering The Economic Questions The system used to allocate resources must answer these questions There are two theoretical rationing systems, free market and planned economy In reality all economies are mixed economies

Resources/FOPs Resources, also known as Factors of Production (FOPs), are goods and services that could be used to produce other goods and services Economist group FOPs under four broad categories: Land Labor Capital Entrepreneurship/Management

Resources/ FOPs Land Includes all natural resources also known as “gifts of nature” such as basic raw materials, cultivated products, renewable and non renewable Labor physical and mental contribution of the existing workforce to production Capital is a man-made factor of production such as investment in physical and human capital Management the (entrepreneurship) organizing and risk taking factor of production

Payments to the Factors of Production Land rent Labor wage Capital interest rate Entrepreneurship / management profit

Explain that when an economic choice is made, an alternative is always foregone Scarcity Choice Opportunity Cost The opportunity cost is the value of the next best alternative forgone or sacrificed when a choice is made to obtain something else. A few examples: If the government chooses to spend more on health care, this means less spending on housing. The reduction in housing is the opportunity cost. The opportunity cost of working overtime is the leisure time that you have sacrificed. You were given 400 as an 18th birthday present. You buy a CD instead of purchasing lunches for a week. The opportunity cost of the CD is the lunches given up.

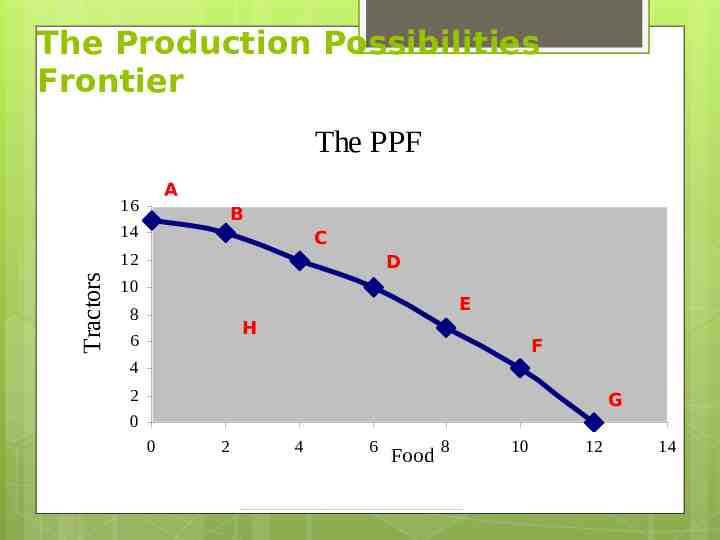

Explain that the PPC/PPF model may be used to show the concepts of scarcity, choice, opportunity cost and a situation of unemployed resources and inefficiency. Our very first economic model The Production Possibilities Frontiers (PPF) In this simple economic model used to show concepts of scarcity, choice, and opportunity cost etc. The following assumptions are made: The economy produces 2 goods only: food and tractors Resources are fixed (unchanging) in quantity and quality and technology (the method of production) is fixed.

The PPF The production possibilities frontier is a graph that shows all the possible combinations of the maximum amounts of two goods that can be produced by an economy, given its resources and technology, such that all available resources are used efficiently (productive efficiency is achieved) For the economy to produce the greatest possible output and operate on the PPC, two conditions must be met: All resources must be fully employed, this means that all resources must be fully used. If some resources were not used, the economy would not be producing the maximum it can produce. All resources must be used efficiently, this means that productive efficiency is achieved. “Efficiency” means no waste. Productive efficiency means that output is produced by use of the fewest possible resources or output is produced at the lowest possible unit cost. Alternatively, if output were not produced using the fewest possible resources, there economy would be wasting some resources.

The PPF If either of the two conditions is not met Simply, the economy will not operate at a point on the PPC; it will be somewhere inside the PPC, such as point H. In the real world, NO ECONOMY IS OPERATING ON ITS PPC. An economy’s actual output is always inside the PPC because all economies have some unemployment of resources and some productive inefficiencies. The greater the unemployment or inefficiencies, the further away the economy is from its PPC.

The PPF The scarcity of resources forces the economy to make a choice about what particular combination of goods it wishes to produce The choices made by an economy involve opportunity costs. Why? Because if the economy were at any point on the PPC, it would be impossible to increase the quantity produced of one good without giving up or sacrificing or decreasing the quantity produced of the other good Let’s see an example

An example: If all the economy’s resources are used to produce15 tractors, 0 tons of food will be produced (point A on the PPC) On the other hand, if all resources are used to produce 12 tons of food, 0 tractors will be produced (point G on the PPC) All the points on the curve between A and G represent other production possibilities where some of the resources are used to produce tractors and the rest to produce food. For example, at point B, all the resources can be used to produce 14 tractors and 2 tons of food. HOW does that happen? If the economy is currently at point A and would like to move to point B, given the resources it has, it’s impossible to have more food without sacrificing the production of tractors. So, to produce 2 tons of food instead of 0 tons of food, the economy had to reduce tractors production from 15 to 14 at point B. The sacrifice of 1 tractor is the opportunity cost of 2 extra tons of food (increasing food by 2 tons)

The Production Possibilities Frontier FoodThe Tractors PPF A 16 14 Tractors 12 10 8 6 4 2 0 0 0 B 2 C 4 H 6 8 104 2 12 15 14 D 12 E 10 7 64 8 Food 0 F G 10 12 14

To sum up The PPF illustrates the concept of opportunity cost. To produce more of one good, less is produced of the other due to the scarcity of the resources. Points on the PPF exhaust all of society’s resources. Points outside the PPF are unattainable given the available resources. Points inside the PPF are inefficient as some resources are unemployed or are not used to their full potential. In this case, an economy can produce more of both goods with no sacrifice, hence no opportunity cost, simply by making better use of its resources: reducing unemployment or increasing productive efficiency.

The shape of the PPC The PPF could be curved (bowed out) or straight line When the PPC is curved, this means that the opportunity costs change as the economy moves from one point on the PPC to another. For example, for each additional ton of food produced, the opportunity cost, which is the amount of tractors given up changes and increases. For the first 2 tons of food produced, the economy gave up 1 tractor and for the second 2 tons of food the economy gave up 2 tractors. WHY? This is because of specialization of factors of production which makes them not equally suitable for the production of different goods and services. For example, as production switches from tractors to more food, the economy must give up increasingly more tractors to produce extra unit of food because factors of production suited to tractors will be less suited to food production. So, as more is produced of food, resources which are best suited to food production are exhausted and less productive resources, which better suit the tractors production, will be used in the food production leading to more losses in the tractors production.

The shape of the PPC By contrast, when the PPC is a straight line, opportunity costs are constant and don’t change as the economy moves from one point on the PPC to another Constant opportunity costs arise when the factors of production are equally well suited to the production of both goods such as the case of basketballs and volleyballs, which are very similar to each other, therefore, needing similarly specialized factors of production to produce them.

Economics is a Science Economics is a social science. Scientific methods are used to study this subject As a social science, it tries to explain in a systematic way why the economic events happen the way they do Data about an economic issue is collected identify variables needed to tackle the issue formulate theories about how the variables are related to each other Test the theory against empirical data

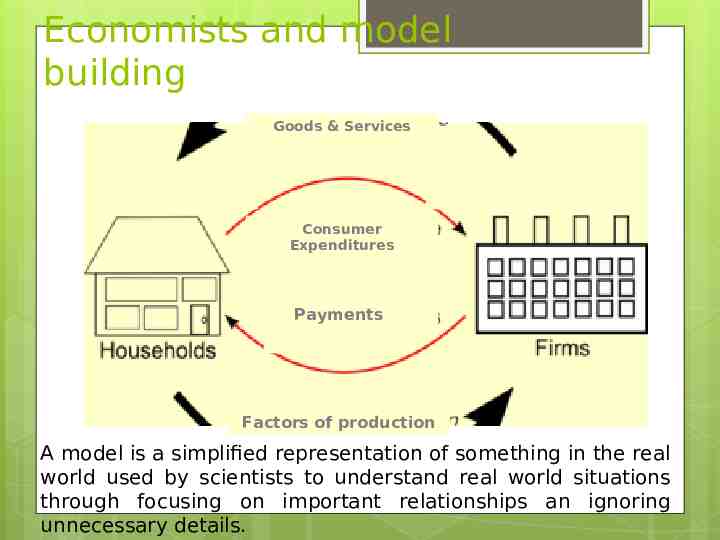

Economists and model building Goods & Services Consumer Expenditures Payments Factors of production A model is a simplified representation of something in the real world used by scientists to understand real world situations through focusing on important relationships an ignoring unnecessary details.

Two assumptions in economic model-building Ceteris Paribus A Latin expression meaning all else equal When studying the relationship between 2 variables, other variables should be kept constant In a scientific setting, this is equivalent to keeping the control variables constant Rational economic decision-making Individuals are assumed to act in their best selfinterest, trying to maximize the satisfaction they expect to receive from their economic decision. For example, workers will want to secure the highest possible wage when they get a job.

Positive & Normative Concepts Positive vs. Normative Concepts Positive statements are descriptive and could be tested The unemployment rate in Egypt is 13% As the price of a good increases, its quantity demanded decreases Normative The statements are subjective government should spend more on education

Microeconomics vs. Macroeconomics Economics is studied on two levels: Microeconomics focuses on details and studies part of the economy Decisions made by one firm (what to produce), or by one individual (demand and expenditure) Macroeconomics studies issues pertaining to the whole economy Unemployment, Inflation, economic growth

Central themes There are some central economic themes that will run through your study of economics. There is no single right or wrong answer to the issues posed. 1. 2. 3. 4. The distinction between economic growth and economic development The threat to sustainability as a result of the current patterns of resources allocation The extent to which the government should intervene in the allocation of resources The extent to which the goal of economic efficiency may conflict with the goal of equity

The distinction between economic growth and economic development Economic growth is an increase in real national output/income/Gross Domestic Product (GDP) over time. Economic growth is an increase in actual output, graphically represented by a movement from a point inside the PPF to a point closer to the curve If actual output produced in an economy decreased, this is called negative economic growth or economic contraction Economic development refers to raising the standard of living and social well-being of people. This means not only increasing incomes and output, but also reducing poverty, redistributing income to narrow down the gap between the rich and the poor, increasing provision of important goods like sanitation, education, healthcare and shelters so that they can be enjoyed by everyone. Economic growth is important to achieve economic development, but this is not always the case. Sometimes growth may not be reflected on the poor people’s living standards due to income inequalities. Human Development Index (HDI) is used to measure development.

Human Development Index (HDI) HDI rank countries based on their real GDP/Capita, adult literacy rate and life expectancy It gives countries values between 0 and 1, with 0 being the worse and 1 being the best

Examples of issues to evaluate Should growth be a priority since it is required to achieve development? Or should development be the priority? What are the best policies to achieve growth and development?

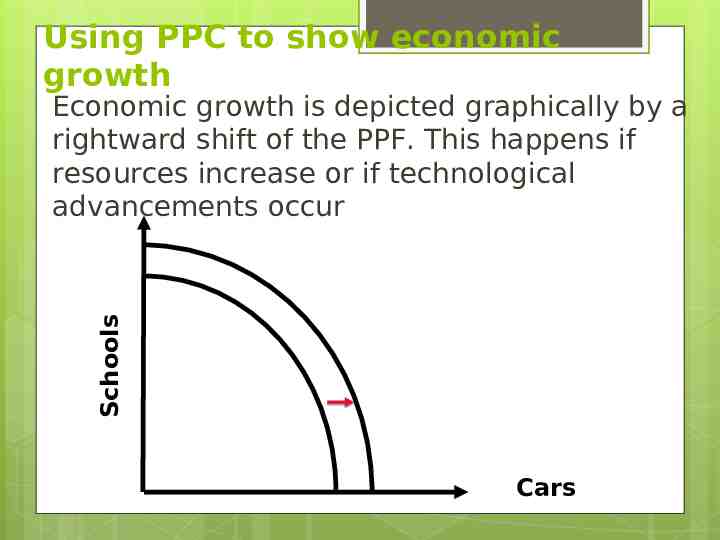

Using PPC to show economic growth Schools Economic growth is depicted graphically by a rightward shift of the PPF. This happens if resources increase or if technological advancements occur Cars

Capital TractorsGoods Future Consumption Relaxing Assumptions Food Consumer Goods Present Consumption

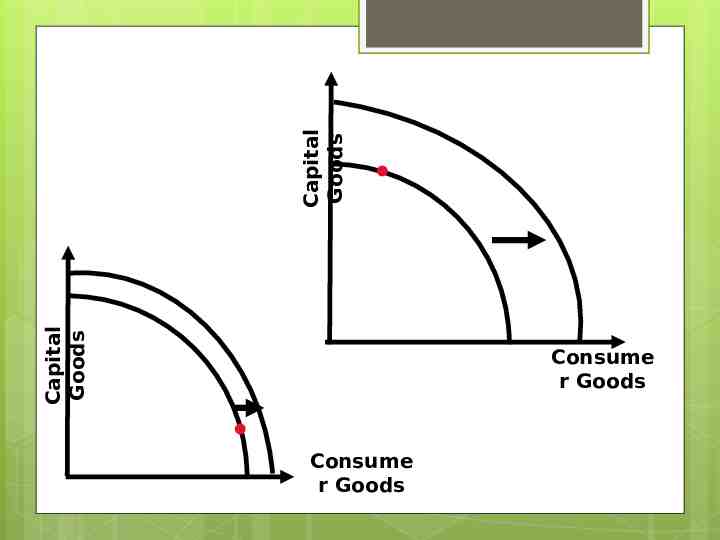

Capital Goods Capital Goods Consume r Goods Consume r Goods

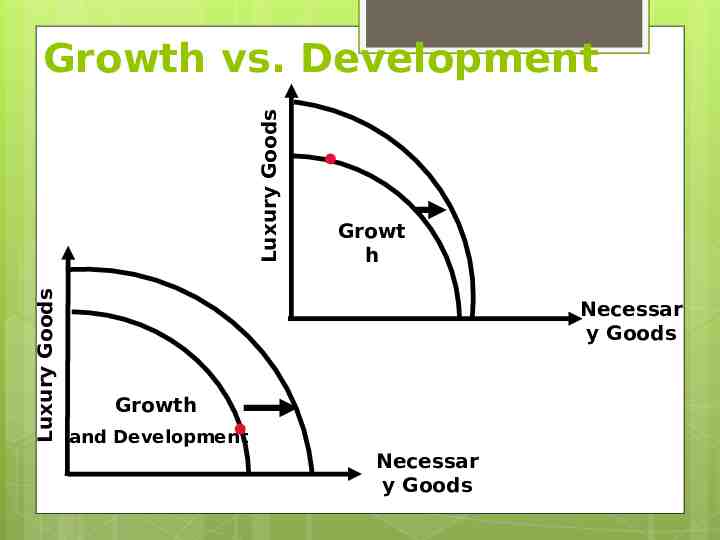

Luxury Goods Luxury Goods Growth vs. Development Growt h Necessar y Goods Growth and Development Necessar y Goods

The threat to sustainability as a result of the current patterns of resources allocation Growth in output very often comes at the expense of natural resources and environment Growth may result in air and water pollution, destruction of forests, depletion of non renewable resources and the ozone layer and the like. This is referred to as unsustainable development or uneconomic growth. Sustainable development is defined as “development the meets the needs of the present generation without compromising the ability of the future generations to meet their own needs”. This occurs when economies grow an develop without leaving behind fewer or lower quality resources for future generations.

Examples of current patterns of resources allocation that result in threats to sustainability Enjoying the benefits of production and consumption today that cause the change in the global climate, use up clean water, forests, and damage the ozone layer means that we are putting the future generations at a disadvantage Unsustainable resource use means that resources are used at a very fast rate that does not give them enough time to reproduce themselves so that they can be maintained over time and not be destroyed or depleted In rich economies, consumption patterns that rely strongly on burning fossil fuels that pollute the environment like excessive use of private cars and home heating are examples of resource allocation that threatens sustainability in rich economies In poor economies, poverty itself causes threats to sustainability as it drives the very poor to destroy their natural environment to survive like cutting down forests to sell the trunks or build shelters or picking up plants before they ripe to eat which destroy the plant’s ability to reproduce in the future.

The extent to which the government should intervene in the allocation of resources There are two main economic systems that economies adopt to make their economic choices: 1. The market economy 2. The command economy In the real world, there is no economy that is entirely a market economy or entirely a command economy. Real world economies combines features of both economies and are thus referred to as: 3. The mixed economy

Free market Economy Private ownership of capital Freedom of choice People are free to buy what they want and firms can enter any market they want responding to price signals Markets Prices are determined by the forces of supply and demand without government intervention

The Basic Questions How are the basic economic questions addressed in a free market economy? 1. What? The freedom to choose ensures that consumer sovereignty prevails so that producers produce what consumers want 2. How? The price of FOPs will induce entrepreneurs to produce in the most efficient way 3. For Whom? The price system rations goods

Centrally Planned Economy (CPE) Capital is owned by the government The government makes all decisions The central planner decides what to produce, which technology to use (how) and how the output is to be distributed (for whom) Prices are controlled by the government

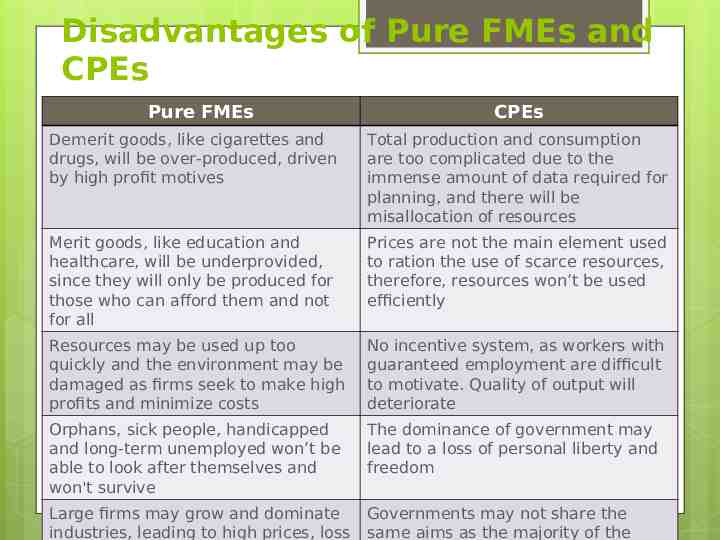

Disadvantages of Pure FMEs and CPEs Pure FMEs CPEs Demerit goods, like cigarettes and drugs, will be over-produced, driven by high profit motives Total production and consumption are too complicated due to the immense amount of data required for planning, and there will be misallocation of resources Merit goods, like education and healthcare, will be underprovided, since they will only be produced for those who can afford them and not for all Prices are not the main element used to ration the use of scarce resources, therefore, resources won’t be used efficiently Resources may be used up too quickly and the environment may be damaged as firms seek to make high profits and minimize costs No incentive system, as workers with guaranteed employment are difficult to motivate. Quality of output will deteriorate Orphans, sick people, handicapped and long-term unemployed won’t be able to look after themselves and won't survive The dominance of government may lead to a loss of personal liberty and freedom Large firms may grow and dominate industries, leading to high prices, loss Governments may not share the same aims as the majority of the

Mixed Economy Most economies are mixed, combining some features of free markets and some features of CPEs In the last 30 years, there have been a trend around the world for economies to move towards becoming free market economies In mixed economies, the command method of making resource allocation is referred to as government intervention. Examples of government intervention include provision of public and merit goods, minimum wage legislation, tax collection among other regulatory and supervisory roles The market economy offers important benefits, yet it does not always produce the best answers to the what, how and for whom questions; therefore, government intervention is needed to guarantee effective operation of the market economy

The extent to which the goal of economic efficiency may conflict with the goal of equity Economic efficiency involves making the best use of resources and avoiding waste; this happens by answering the what and how questions by allocating resources in the best possible way to producing only goods that society needs most to avoid wasting resources Equity is interpreted as greater equality and less inequality in the amount of income received by individuals in in a society The aim is not to distribute income equally but to ensure that people with little or no income in a market economy will be able to survive and have access to food, shelter, healthcare and other basic needs.

The extent to which the goal of economic efficiency may conflict with the goal of equity According to many economists, there is a tradeoff between efficiency and equity; more income equality involves less efficiency and vice versa. For example, government intervention to achieve equity may result in a less efficient resource allocation; for instance, “government subsidizing bread to make it affordable may result in people misusing it”

The extent to which the goal of economic efficiency may conflict with the goal of equity It is widely believed that government intervention to achieve equity results in many of the following: Changes in the work effort Changes in saving and investment patterns No or less incentive to learn and acquire new skills to become more productive Contrarily, other economists believe that government intervention to achieve equity will improve efficiency since it will increase people’s ability to work and make them more productive as it will provide them with money needed for better education and medical services, appropriate shelters etc.

Free Goods There are few things that are unlimited in supply i.e air and salt water and therefore have no opportunity cost. Since these goods are not relatively scarce and have no price they will be known as Free Goods

Free Goods vs. Economic Goods A free good is a good, which does not have an opportunity cost because it is abundant e.g. sea water, sand, etc. An economic good is a good, which has an opportunity cost

Consider the following You buy a Wilson racket because it advertises a set of tennis balls for free. Is the advertised gift a free good? No, because scarce resources were used to produce it.

Technology The technology available sets a limit on how resources can be combined to produce a given amount of output. If it takes 1 ton of steel to produce a car, and society has 10 tons of steel, then a maximum of 10 cars could be produced. Technology improvements allow society to use its resources more efficiently. i.e. to produce more output with a given amount of resources.

Goods vs. services Goods are physical (tangible) objects that satisfy people’s needs and wants, ex. food, cars, books, computers, houses etc. Services are non-physical (intangible) activities that satisfy human’s needs and wants such as education, health care, food delivery, car repair, banking etc.

The End