DALLAS COUNTY HOME LOAN COUNSELING CENTER Upfront Cost

12 Slides820.71 KB

DALLAS COUNTY HOME LOAN COUNSELING CENTER Upfront Cost Assistance Program(UPCAP)

PREPARING TO APPLY FOR UPCAP PROGRAM Credit Score: In order to get a mortgage loan to buy a house you must have “Good Credit”. If your credit needs improvement get that done first. Apply for a Mortgage: Choose a mortgage lender and get pre-approved or Pre- qualified. Save Money for “Upfront Expenses”: Such as earnest money, inspection fee, appraisal fee. This will be 1% - 2% of home price.

UPCAP PROGRAM The UPCAP Program provides loan of up to 7,500 for down payment, closing costs, and pre-paid costs to first-time homebuyers. Lender see’s other area to allocate funds APPLICATIONS: Anyone wishing to receive the UPCAP loan must request an UPCAP application from our office. Applicants must be pre-qualified for a mortgage loan from a lender. Applications may be mailed or turned in to our office by the home buyer only Application must be turned in with all required additional documentation as detailed on Application Instruction Sheet. Incomplete applications will not be accepted. Applications may be submitted before or after attending the Homebuyer Seminars. Applicants are encouraged to submit applications as soon as mortgage approval is received. If a sales contract has been executed, applications should be submitted immediately.

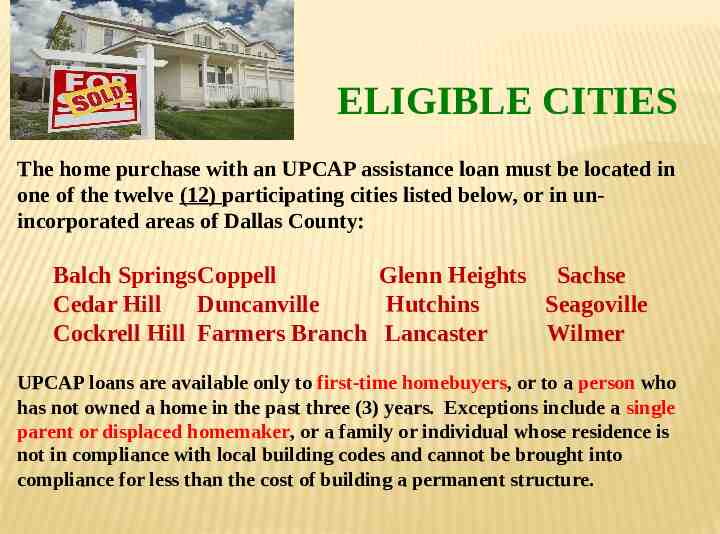

ELIGIBLE CITIES The home purchase with an UPCAP assistance loan must be located in one of the twelve (12) participating cities listed below, or in unincorporated areas of Dallas County: Balch SpringsCoppell Glenn Heights Sachse Cedar Hill Duncanville Hutchins Seagoville Cockrell Hill Farmers Branch Lancaster Wilmer UPCAP loans are available only to first-time homebuyers, or to a person who has not owned a home in the past three (3) years. Exceptions include a single parent or displaced homemaker, or a family or individual whose residence is not in compliance with local building codes and cannot be brought into compliance for less than the cost of building a permanent structure.

INCOME LIMITS Household gross annual income cannot exceed HUD income limits as follows;2 Family size: 1 3 4 Maximum 48,300 68,950 Income Family Size : 5 8 Maximum 74,500 91,050 Income 55,200 6 80,000 62,100 7 85,500

Property Requirements Maximum purchase price is 237,000 for existing homes and 251,000 for new construction homes. Eligible properties: new construction properties, existing properties, condominiums, townhomes, one unit of a duplex. Properties, both structure & lot cannot be located in flood zones per FEMA maps. Properties must be vacant or owner occupied. Tenant occupied properties must have been vacant for 60 days prior to executing a sales contract. However, a tenant may purchase the home they are renting. The home purchase price may not be more than the lenders appraisal value. HUD homes are not eligible for the UPCAP Program. Bank foreclosures, and short sales may be eligible on a case by case basis. Properties built prior to 1978 must pass a lead based paint visual assessment during the home inspection. If exposed lead based paint is found it must be stabilized by the seller.

Property Inspection All properties must be inspected by a home inspector from the “Dallas County Minimum Property Standards (MPS) Inspectors List”. Inspections made by other inspectors are not accepted. A TREC inspection, and MPS Inspection, and a “Texas Wood Destroying Insect Report” must all be done. All inspector or lender required repairs must be made prior to closing. Real estate sales contracts must state that all lender or inspector required repairs will be made prior to closing. A property may be ineligible for the UPCAP Program if major damage to the foundation, roof electrical or plumbing systems, or other excessive damage is found. The inspection must be paid for by the buyer at the time of the inspection.

Financing Applicant must have received a pre-qualification letter from their mortgage lender. Applicant must have acceptable credit history and be able to qualify for a fixed rate mortgage with a lending institution. Subprime loans: ARM loans: owner financing: contracts for deed and interest only loans are not eligible. Lender fees and charges cannot exceed 2,500. Applicants housing ratios cannot exceed 35% and debt ratios cannot exceed 45% of gross monthly income.

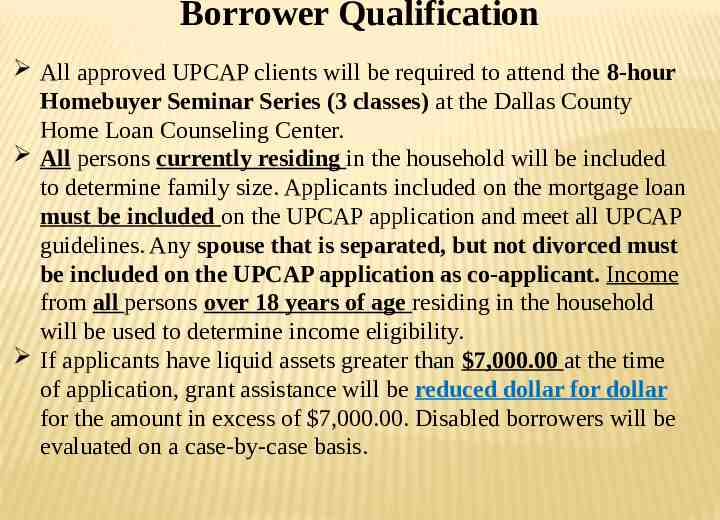

Borrower Qualification All approved UPCAP clients will be required to attend the 8-hour Homebuyer Seminar Series (3 classes) at the Dallas County Home Loan Counseling Center. All persons currently residing in the household will be included to determine family size. Applicants included on the mortgage loan must be included on the UPCAP application and meet all UPCAP guidelines. Any spouse that is separated, but not divorced must be included on the UPCAP application as co-applicant. Income from all persons over 18 years of age residing in the household will be used to determine income eligibility. If applicants have liquid assets greater than 7,000.00 at the time of application, grant assistance will be reduced dollar for dollar for the amount in excess of 7,000.00. Disabled borrowers will be evaluated on a case-by-case basis.

Borrower Qualification Applicants and Co-Applicants must be a US citizen or a permanent resident or possess a current work authorization Visa. Permanent residents and individuals with a work authorization visa must provide to HLCC a copy of both sides of the unexpired immigration documents. No member of the household shall own any improved real estate, lot or structure, which is or can be used for residential purposes, including mobile homes with a permanent fixed foundation. Applicants must contribute a minimum investment of a least 1,000 or 1% of the purchase price whichever is greater, to the home buying process. Earnest money, option fee, appraisal fee, inspection fee, cash due at closing and any paid outside of closing expenses will all be credited to the applicant’s minimum investment requirement.

Occupancy Requirements Dallas County will hold a second lien on the property for the amount of the UPCAP loan ( 7,500) for a five year term. The buyer must live in the property for five years as their sole primary residence. If a buyer sells, leases out, transfers the title to the property to anyone else, or is foreclosed upon, a Repayment and Release Procedure will be required.

QUESTIONS