Cost Sharing University of Massachusetts, Amherst March 29,

47 Slides670.84 KB

Cost Sharing University of Massachusetts, Amherst March 29, 2018 Presenters: Marcia Day, John Fillio, Sandra Haynes, Ian Raphael, Denise Storm

Today’s Workshop-We Will Talk About: Concepts and Pre-Award What is Cost Sharing? Cost Sharing Trends Financial Impacts of Cost Sharing Institutional Resources Vs. Cost Sharing Commitments Mandatory and Voluntary Cost Sharing Roles and Responsibilities (preaward) Allowable items for Cost Sharing Items Not Typically Used for Cost Sharing Over the Cap Salary Post-Award Roles and Responsibilities (post-award) Financial Reporting of Cost Share Tracking Cost Share Companion Accounts Third Party Calculations Based on Waived or Unrecovered Expenses Running 7047/7062 reports Effort Reporting Closeout Audit Implications Handy Links and Guidance

What is Cost Sharing? For Federal awards, Uniform Guidance at 200.29 defines cost sharing or matching to mean the portion of a project costs not paid by Federal funds A formal commitment to be tracked and reported, and subject to audit

Cost Sharing Trends Uniform Guidance established that cost sharing is not expected, and if required, should clearly be stated in advance in the notice of funding. NSF has instructed that in most cases, cost sharing must not be provided in a solicitation Some sponsors have intentionally moved away from encouraging cost sharing when its not required We will continue to manage cost share commitments on older awards. Certain programs will still require cost share; some non-federal sponsors, particularly foundations, may still actively encourage it

Why is cost sharing significant? If the proposal is successful and the award is made, cost sharing becomes a binding legal commitment There is an audit risk if commitments are not honored Federal sponsors and institutions are tightening regulations and practices

Impacts of Cost Sharing at our University Opportunity cost of other initiatives that could have been supported If we do not meet cost share requirements, we may be required to refund a proportional amount of award funds. Audit risks

Impacts Continued Administrative burden to: Identify funding source Include commitments on IPF Review expenses for allowability Track cost share amounts Timely review and certify expenditures Document & report commitments

Mandatory Cost Sharing Only when sponsor policy is clear and documented. Check with OPAM if sponsor policy wording is ambiguous Person contributing funds has reviewed proposal & approved IPF IPF shows contributor’s name & speed type that is the source of allowable funds Ratio does not exceed sponsor requirement (if not specified, no more than 1:1)

Voluntary Cost Sharing (rare) Sponsor does not require; strongly discouraged by campus Must seek campus approval: VCRE for 3rd party (not subcontract) cost sharing OPAM Director for all else Sharing from allowable cost categories

Mandatory or Voluntary Cost Sharing – Must be Tracked and Documented Regardless of whether a sponsor requires cost sharing, the campus must track and document all cost sharing commitments

Institutional Resources Vs. Cost Sharing Commitments Voluntary Cost Share is no longer required or needed to influence sponsors to award a project Where can institutional resources be discussed in a proposal? Well-crafted letter of support Facilities and resources statement Narrative with institutional commitment language Leave out any quantifiable financial information that can trigger a cost sharing definition!

Roles and Responsibilities

Roles and Responsibilities – Pre-Award PI: follow proposal guidelines & campus procedures for including cost sharing commitment in proposals Business Manager: identify cost sharing requirements in proposal guidelines, work with PI to obtain timely approvals and appropriate documentation. Ensure AY Cost Share form and IPF are correct

Roles & Responsibilities: Pre-Award Continued. School/Department: provide appropriate source(s) to fund cost sharing. Ensure appropriate parties have signed off on AY Cost Share form, are shown correctly on IPF, and included in proposal routing OPAM: ensure proposed cost sharing commitments are based on University policy. Ensure promises of funding are guaranteed by written commitment and/or accounts. Communicates CS requirements to the Controller’s Office.

Campus Approval Process Before proposal is routed to OPAM Who to approach How to indicate Budget forms IPF Academic Year Cost Share form

Allowable Line Items for Cost Sharing PI/co-PI cost-shared effort (salary & fringe) Unrecovered indirect costs when sponsor policy restricts F&A rate Other salaries and fringe Tuition waiver: discuss with Grad School first Equipment Subcontractor cost sharing 3rd party cost share if approved by VCRE

Cost-Shared Effort PI/Co-PI academic year salary and fringe benefits (not summer) Proposal documents must include signed Faculty AY Cost Share form if 9-month app’t Include all current effort commitments Upload the signed form when routing proposal to OPAM

Tuition Waiver Discuss with Debra Britt, Graduate School, while developing budget Add Ms. Britt to proposal routing See OPAM Fact Sheet for current rates allowed for cost sharing Show # of grad students in cost sharing section of the IPF

F&A (Indirect) Costs Unrecovered F&A When sponsor policy limits the F&A to less than UMass’ negotiated rate If sponsor allows, you can cost share the difference in F&A, up to the full rate F&A Associated with Costs If needed, use the F&A associated with direct costs that are shared

Equipment Must be purchased within grant period Solely dedicated to the project Name of account signatory is on the IPF with Speed type Account signatory is in the proposal routing map as an approver

Subcontractor Cost Sharing If mandatory cost sharing Ideally, subcontractors cost share the same ratio as required of UMass

Third Party (not subcontractor) Must have VCRE approval before proposal is routed to OPAM: Submit request including department and college recommendations to VCRE two weeks ahead of the 5-day OPAM internal deadline Route documentation of approval with the proposal to OPAM Show secondary source in the event all funding is not provided

Not “Typically” Used for Cost Sharing Materials:and Supplies Tuition Fees (formerly curriculum fees) Summer Effort (9-month position) Over the Salary Cap (e.g. NIH) Service Center Fees cannot be waived Institutional facilities, services, space, etc. Employee Travel Federal Funds (& other grants). Unless a grant is specifically issued for cost share.

Over the Cap Salary When faculty salary base exceeds sponsor’s regulatory maximum (e.g., NIH) Salary costs above statutory limits are not cost sharing per the UG Appendix III to part 200 Over the cap salary cannot be used to meet cost sharing commitments. It is considered unallowable cost to the sponsor Excess salary is shown on IPF but not tracked as cost share

NIH Salary Cap – Is It Cost-Sharing? The NIH Salary Cap is a salary limitation policy Excess salary above the cap is not “Cost-share” and not reportable as formal cost-share back to the sponsor Excess salary above the cap is “cost-shared” (paid) with University funds: if summer salary: paid from the capped person’s RTF If academic salary: paid by the department Example: Current NIH cap: 189,600 (calendar year) or 15,800 per month

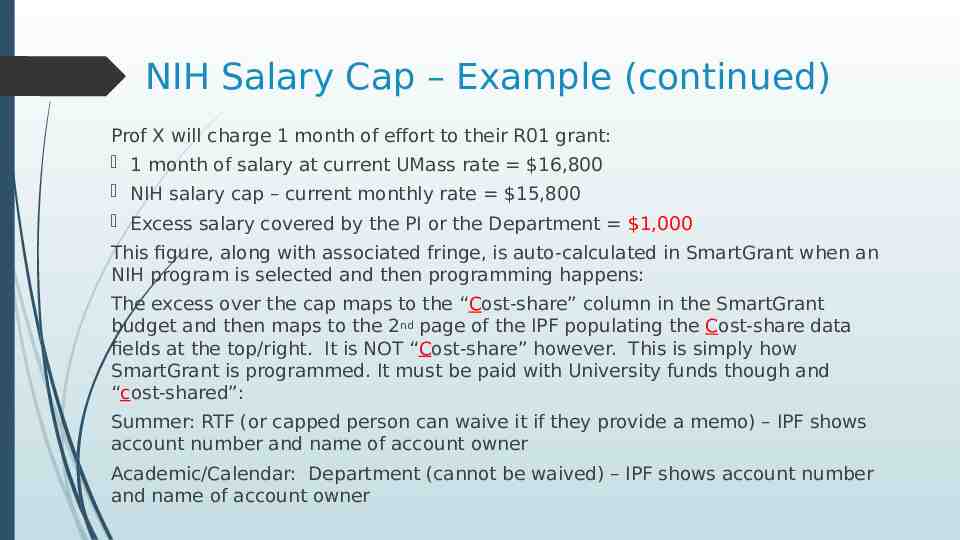

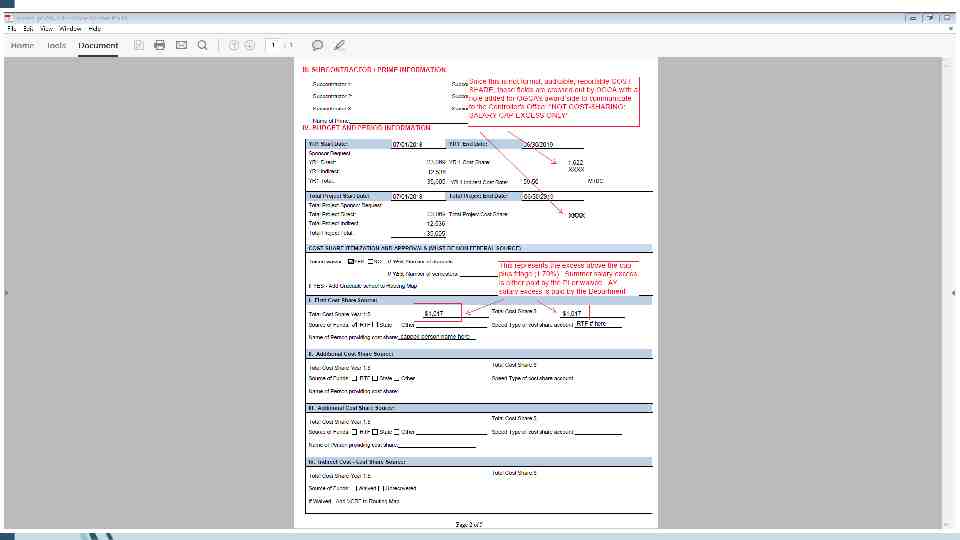

NIH Salary Cap – Example (continued) Prof X will charge 1 month of effort to their R01 grant: 1 month of salary at current UMass rate 16,800 NIH salary cap – current monthly rate 15,800 Excess salary covered by the PI or the Department 1,000 This figure, along with associated fringe, is auto-calculated in SmartGrant when an NIH program is selected and then programming happens: The excess over the cap maps to the “Cost-share” column in the SmartGrant budget and then maps to the 2nd page of the IPF populating the Cost-share data fields at the top/right. It is NOT “Cost-share” however. This is simply how SmartGrant is programmed. It must be paid with University funds though and “cost-shared”: Summer: RTF (or capped person can waive it if they provide a memo) – IPF shows account number and name of account owner Academic/Calendar: Department (cannot be waived) – IPF shows account number and name of account owner

Roles and Responsibilities-Post Award PI-Ultimately responsible to ensure cost sharing commitments are met. PI’s approve cost share transactions and certify effort reports. School/Dept.-Day to day management of cost sharing, ensures that all cost share is processed on the appropriate account(s), keeps the PI informed of whether s/he is on target to meet commitments, review allowability of costs. Controller’s Office-Overall monitoring to ensure commitments have been met before filing the necessary reports to the sponsor. Regardless of reporting requirements, we must have appropriate documentation to show that we have met our cost share commitments before closing out the award.

Cost Sharing-Post Award The Controller’s Office receives the award from OPAM to [email protected] The OPAM award slip lets the Research Accountant (RA) know that we have a commitment to cost share “mandatory cost share” in the Notes section. If an RA identifies a possible cost sharing commitment in the award documents, and “mandatory cost share” is not indicated on the slip. The RA will work with OPAM to determine our requirements prior to award set up.

Review Terms and Conditions It is always important to carefully review terms and conditions of an award so that we all understand what is expected by the sponsor. This is particularly important when we have a commitment to cost share and the sponsor is nonfederal. The types of costs that may be used, method of valuation of donations, standards for support documentation may be different than for our Federal sponsors.

Financial Reporting Non-reportable per the terms of the awardCommitted cost sharing that must be documented but is not reportable to the sponsor. Although this type of cost sharing is not reported to the sponsor, it is subject to audit. Reportable per the terms of the awardCommitted cost sharing that must be documented by the department and must be reported to the sponsor by the Controller's Office

Tracking Cost Share and use of Cost Share Speed Type/Companion Account When cost sharing salary and related fringe, equipment, or providing cash contributions, a cost share speed type/companion account (using allowable funds) is created by the RA to help us track our commitment(s). The total amount of cost share is recorded in PS to appear on the PIN report. We do not set up a budget on the companion account. The PIN report notifies the PI/Department with the cost share speed type.

Using a Cost Share Speed Type / Companion Account It is the departments responsibility to use the speed type and to know whether we are on target to meet our cost sharing commitment(s) and to review the allowability of the costs. Prepare a PAF using the cost share speed type (payroll) Prepare a purchase requisition using the cost share speed type (equipment) Transfer allowable costs to the cost share speed typed to correct an error (direct costs vs. cost shared costs) Please note: The analysis type for the Cost share account is CGE NOT GLE

Fringe Rates on Companion Accounts/Speed types Full fringe rates are not automatically calculated on non-sponsored funds The Dept. and RA does a manual calculation of fringe to ensure that the correct amount of cost share is identified to meet cost share commitments and therefore documented as cost share Funds which do not charge full fringe rates 11000, 51006, 51369

Tracking Cost Share: Third Party 2 types Separate Award-third party issues an award matching Cost Share commitment to UMass. The RA extracts information as required. Commitment letter-third party (in kind) issues a well crafted letter detailing obligated effort/service with an assigned monetary value and this is submitted at proposal. Third party then provides a report which shows actual cost share.

Tracking Cost Share: Calculations Based on Waived or Unrecovered Expenses Tuition Waivers-Graduate student tuition charge rates are set by the University on a fiscal year basis and are used as cost share. Departments provide the number of students and waiver amount to the RA as necessary. Unrecovered F&A-Sponsor approves lower F&A rates than the University’s official F&A rate and the variance is used to calculate cost share F&A Waivers-University official F&A rates are waived, the percentage waived is calculated on the applicable expenditures for cost share

Tracking Cost Share-People Soft When you run a 7047 or 7062 using the P/G # or award # you will generate the cost share companion account financial info, as well as the P/G financial info. The reports will reflect only the expenses on the account because there is no budget for cost share. Compare the cost sharing commitment per the terms of the award to the expenditures on the companion account. Please Note: If the companion account is set up with fund code 11000, you should see shadow account 51369 show on your reports because the payroll is transferred by the system to that fund.

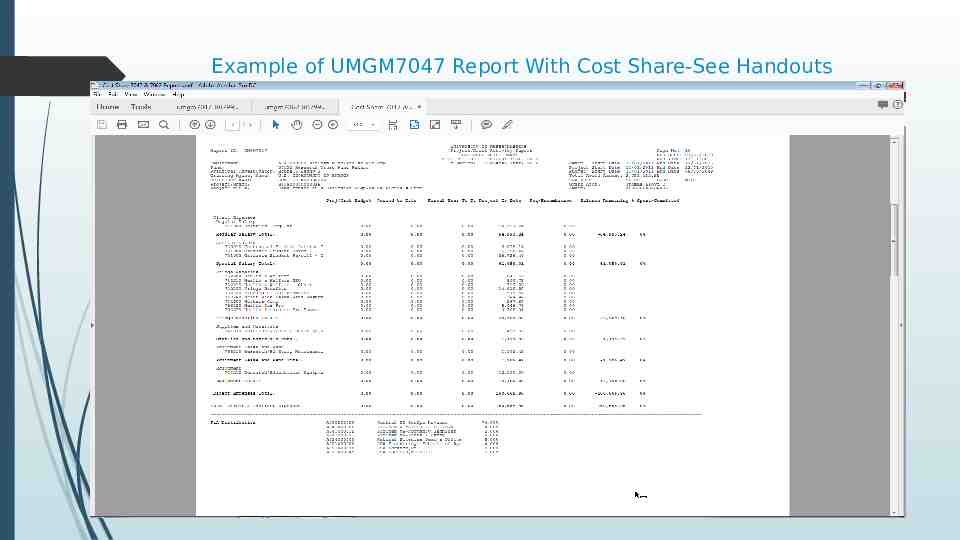

Example of UMGM7047 Report With Cost Share-See Handouts

Effort Reporting Salary cost sharing is separately identified and certified as part of the effort certification process using companion accounts.

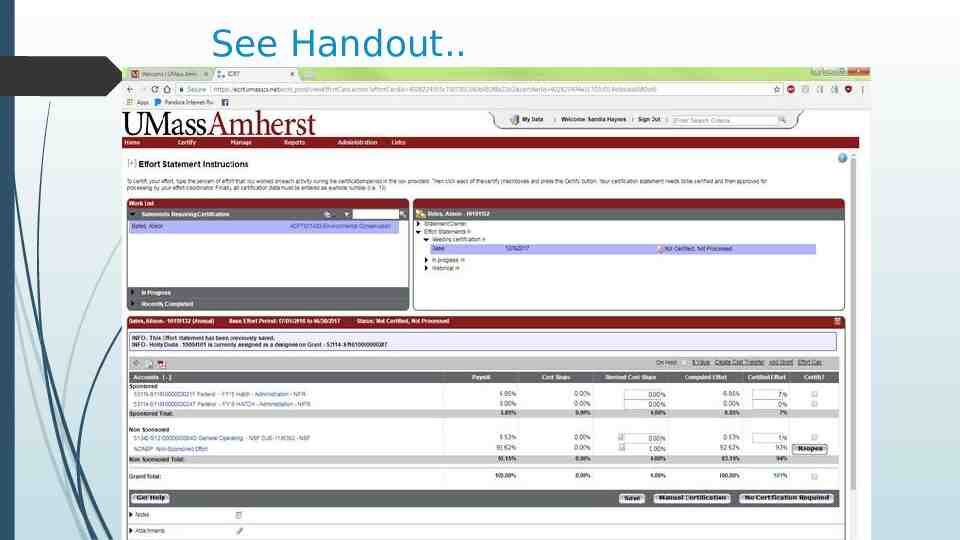

See Handout.

Closeout The Controller’s Office ensures that the necessary reports are being submitted to the sponsor and that the cost sharing commitments have been met and are properly documented as a part of the closeout process. Departments must provide any necessary additional cost share information to the RA in a timely fashion so that the RA can process/submit reports on time. We as the prime are ultimately responsible for cost sharing, if the subawardee does not meet commitments, we are ultimately responsible

Audit Implications NSF Award and Administrative Guide states: “Grantees should be aware that cost sharing commitments are subject to audit. Audit findings involving cost sharing have pertained to: Grantee accounting systems not capturing cost sharing Failure to keep adequate source documentation for claimed cost sharing Unclear valuation of in-kind donated contributions Lack of support for cost sharing contributions by subrecipients Failure to complete annual certifications for awards with cost sharing requirements of 500,000 or more

Awarded Cost Share-Things to Remember All cost share is subject to audit Cost sharing must normally be from non-sponsored sources. Exception: When a third party issues a separate award matching CS commitments to UMass Cost shared expenses must contribute directly to the project (allocable) All cost share must be allowable for project spending. If costs are not allowed on the grant, they are not allowed to be cost shared (unless prior approval is obtained from the sponsor) All cost share must be spent within the grant period Cost share may need to be reported to the sponsor (if required) Sponsor may reduce the award if cost share is under reported Cost share can be tracked in PeopleSoft/Summit Companion accounts are inactivated at the same time as the project PI’s must certify cost shared effort

Handy Links-Cost Share Cost Sharing, Policy and Procedure Amherst Campus Cost Sharing Approval Process http://www.umass.edu/research/form/cost-share-request-form-ay-faculty-salary Procedures for Request of Indirect Cost Waiver or Reduction http://www.umass.edu/research/guidance/cost-sharing-requests-vcre-or-provost Faculty AY Effort Cost Share Approval Form http://www.umass.edu/research/guidance/cost-sharing-sources-and-types Procedure for Requesting VCRE and Provost Cost Share http://www.umass.edu/research/guidance/cost-sharing-faq Cost share guidance regarding sources and types http://www.umass.edu/research/guidance/cost-sharing-approval-process Cost Share FAQs http://www.umass.edu/research/policy/cost-sharing-policy http://www.umass.edu/research/guidance/indirect-cost-waiverreduction Template for Subrecipient Invoices which includes Cost Sharing https://www.umass.edu/controller/sites/default/files/Subrecipient Invoice.pdf

Uniform Guidance-Rules and Guidelines about Cost Sharing 200.29 defines cost sharing 200.99 defines voluntary committed cost sharing 200.306 establishes administrative standards 200.434 contributions and donations –how value of donated services and property may be used to meet cost sharing requirements Appendix I to part 200(C,2)-Eligibility information when cost sharing is required Appendix III to part 200-Committed cost share must be included in the organized research base for computing the F&A cost rate. Salary costs above statutory limits are not considered cost sharing

Q&A Q1) Effort reporting is confusing. If we cost share salary because of the NIH cap, how do we figure that out and make a note in the effort reporting system? For example, what if a faculty member makes 250K and they cost share part of their salary on state funds. How do we do the math to figure out how much was cost shared and how do we put that in ECRT? Answer: Over the Cap Salary is the portion of a faculty or staff members salary that exceeds regulatory maximum imposed by the sponsor. It cannot be used to meet cost sharing commitments because it is unallowable to the sponsor. Per the U.G. costs above statutory limits are not considered cost sharing. Over the cap is included in the total of the nonsponsored effort line.

Q&A Q2) When actual effort is more than paid effort due to a salary cap limitation, how is this best handled in the effort certification system? Answer: the best way to handle this is to certify the payroll on the effort card as calculated and then add a note to the effort card for audit purposes, about the certification percentage needing to be adjusted due to the salary cap.