Appropriations Used/Expended – Accrued vs. Disbursed For USSGL Board

6 Slides305.85 KB

Appropriations Used/Expended – Accrued vs. Disbursed For USSGL Board May 2020

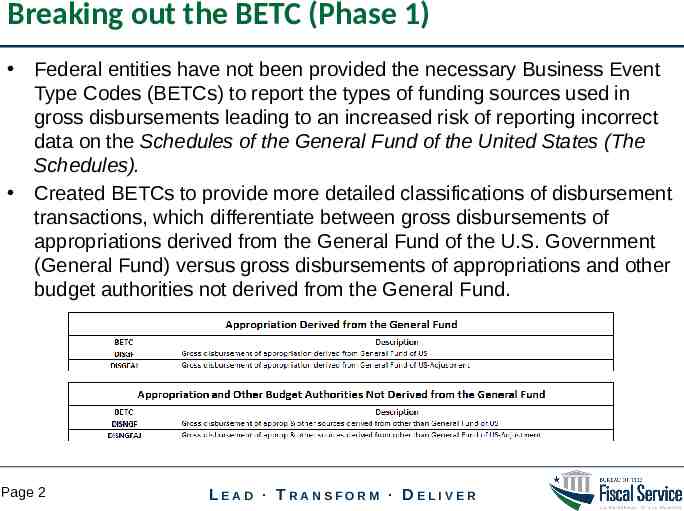

Breaking out the BETC (Phase 1) Federal entities have not been provided the necessary Business Event Type Codes (BETCs) to report the types of funding sources used in gross disbursements leading to an increased risk of reporting incorrect data on the Schedules of the General Fund of the United States (The Schedules). Created BETCs to provide more detailed classifications of disbursement transactions, which differentiate between gross disbursements of appropriations derived from the General Fund of the U.S. Government (General Fund) versus gross disbursements of appropriations and other budget authorities not derived from the General Fund. Page 2 LEAD TRANSFORM DELIVER

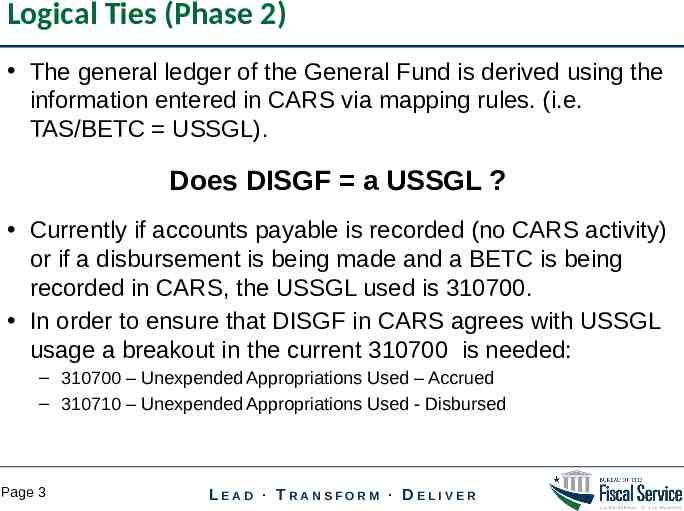

Logical Ties (Phase 2) The general ledger of the General Fund is derived using the information entered in CARS via mapping rules. (i.e. TAS/BETC USSGL). Does DISGF a USSGL ? Currently if accounts payable is recorded (no CARS activity) or if a disbursement is being made and a BETC is being recorded in CARS, the USSGL used is 310700. In order to ensure that DISGF in CARS agrees with USSGL usage a breakout in the current 310700 is needed: – 310700 – Unexpended Appropriations Used – Accrued – 310710 – Unexpended Appropriations Used - Disbursed Page 3 LEAD TRANSFORM DELIVER

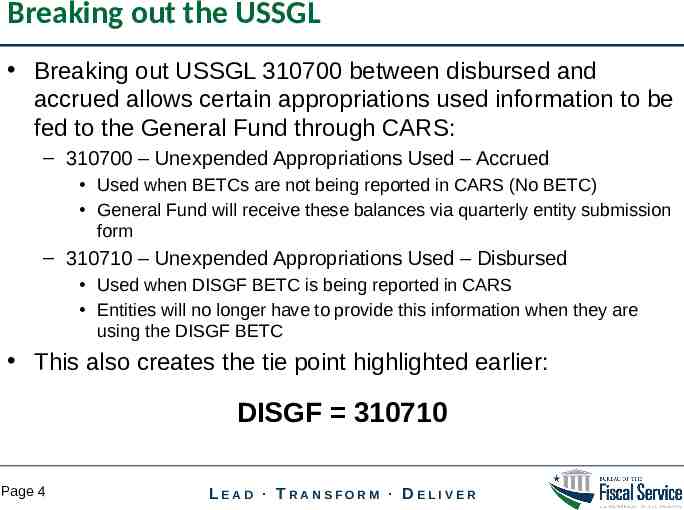

Breaking out the USSGL Breaking out USSGL 310700 between disbursed and accrued allows certain appropriations used information to be fed to the General Fund through CARS: – 310700 – Unexpended Appropriations Used – Accrued Used when BETCs are not being reported in CARS (No BETC) General Fund will receive these balances via quarterly entity submission form – 310710 – Unexpended Appropriations Used – Disbursed Used when DISGF BETC is being reported in CARS Entities will no longer have to provide this information when they are using the DISGF BETC This also creates the tie point highlighted earlier: DISGF 310710 Page 4 LEAD TRANSFORM DELIVER

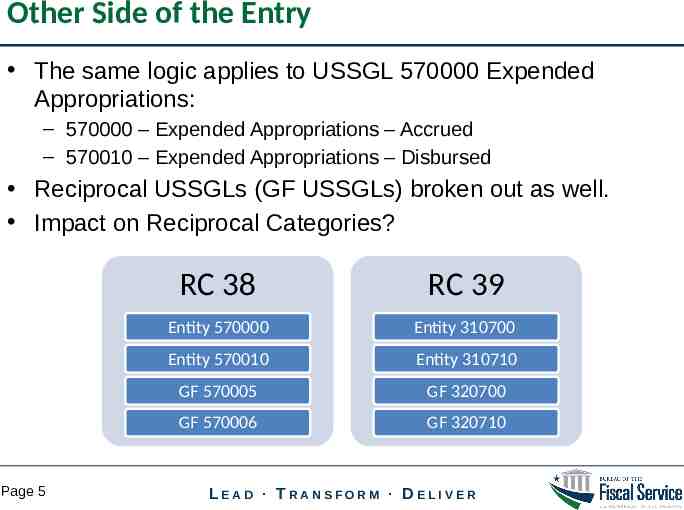

Other Side of the Entry The same logic applies to USSGL 570000 Expended Appropriations: – 570000 – Expended Appropriations – Accrued – 570010 – Expended Appropriations – Disbursed Reciprocal USSGLs (GF USSGLs) broken out as well. Impact on Reciprocal Categories? Page 5 RC 38 RC 39 Entity 570000 Entity 310700 Entity 570010 Entity 310710 GF 570005 GF 320700 GF 570006 GF 320710 LEAD TRANSFORM DELIVER

General Fund of the U.S. Government General Fund Mailbox [email protected] Page 6 LEAD TRANSFORM DELIVER